Dear Baiguan readers,

We have something new to share.

We’re launching Baiguan Pro this April.

Here’s why, and what’s inside the first issue.

Why we built this

Have you ever read a Baiguan piece introducing a phenomenal company — be it Pop Mart, Laopu Gold, others, and thought — Okay, I hope I can know how this company performs from now on. Or, have you ever read a piece about China’s service sector, experiential spending, or robotaxi industry, and wondered, but what is the Baiguan team actually doing with this?

We get these questions a lot.

Over three years of writing the newsletter, we’ve noticed our readers split into two groups. One group loves the broader China observations — the cultural context, the business stories, the macro backdrop. But there’s another group that keeps asking a more specific question: I’m bullish on China after reading you. Now what do I actually do? (There are overlaps, of course.)

Baiguan Pro is for the second group.

Here’s what we’ve realized: we’ve flagged a lot of companies, sectors, and themes in the newsletter, and readers have told us they want the follow-through. Not just the observation, but the investment thinking behind it.

We also sit on a lot of data. Baiguan has some of the best ground-level macro, consumer, and sentiment data on China out there. But data alone doesn’t tell you what to do. In Baiguan Pro, we’ll pair our data with a more structured, directional view — what we’re watching, and why.

One more thing that shapes how we think: everyone on the Baiguan team manages their own global, multi-asset portfolios. We’re not single-country analysts. That means when we look at China, we’re always looking at it in context — what else is on the table, what the opportunity cost is, how an international allocator actually thinks about an allocation decision. That global frame is built into how we write Baiguan Pro.

What to expect

Baiguan Pro has a consistent content structure, so you always know what’s coming:

Monthly View on Chinese Assets — Each month, we pull together macro data, BigOne Lab (Baiguan’s parent company)’s proprietary data and indices, and the relevant policy backdrop to give you a structured read on where Chinese assets stand. The goal is to cut through noise and give you a directional view, backed by data.

Quarterly Theme Focus List — Every quarter, we identify the sectors, themes, and idiosyncratic opportunities we think are worth paying attention to for the next three months. This isn’t a buy list — we flag both opportunities and risks, both longs and shorts. We flag what’s interesting and why, and we’re equally willing to tell you when something looks stretched or when the consensus narrative seems wrong.

Follow-Up & Deep Dives — For themes on our quarterly list, we follow through: deep dives into industries or companies, BigOne Lab’s own data on specific trends, and the occasional company or story that’s just too “meme” to ignore.

Baiguan Data Highlights — Data insights feeds from BigOne Lab’s industry analyst team, shared with our institutional clients.

Occasional Commentary — When something happens in the market that actually matters, we’ll write about it. Brief, direct, no fluff.

Baiguan Pro is available as an upgrade via Baiguan Professional Tier (Founding Member).

For existing Baiguan free subscribers: nothing changes with your current subscription. We’ll continue covering China broadly in the newsletter — context, culture, business, macro — and we plan to expand that coverage further over time.

For existing Baiguan paid subscribers: We are offering an upgrade to the Professional tier, giving you full access to all Baiguan Pro content. To upgrade, please REPLY to this email with the email address associated with your paid subscription. We are processing these upgrades manually through the end of the second quarter (June 30). (Please note that if you opt-in to the Baiguan Pro tier, your subscription will renew at the new rate if auto-renewal is enabled.)

This Month: Our View on Chinese Assets

First, we believe China is meaningfully underweight in ACWI relative to its economic footprint, and we think that gap has overshot. The discount is understandable historically, but the risk/reward of adding from here is better than consensus implies.

We prefer A-shares over HK, currently — Three specific reasons: (1) the national team floor mechanism is a genuinely unusual feature with no real global analog; (2) in an elevated geopolitical risk environment (Iran conflict backdrop), A-shares’ domestic-anchored dynamics make them more uncorrelated with global risk-off moves; (3) the composition of A-shares — AI/tech supply chain, heavy industrials, domestic manufacturers etc. — is a better fit for the China themes we find most interesting right now versus the HK.

Our team’s directional view on China equity allocation is currently overweight relative to the MSCI All Country World Index (ACWI) index.

A few specifics driving that view:

Chinese equities (and broader markets) have had a choppy start to 2026. After a meaningful recovery in late 2024 and into 2025, driven by policy support and a wave of improving sentiment, the market is now in a more discerning phase — one where fundamentals are doing more of the work. Last year’s recovery captured much of the easy re-rating.

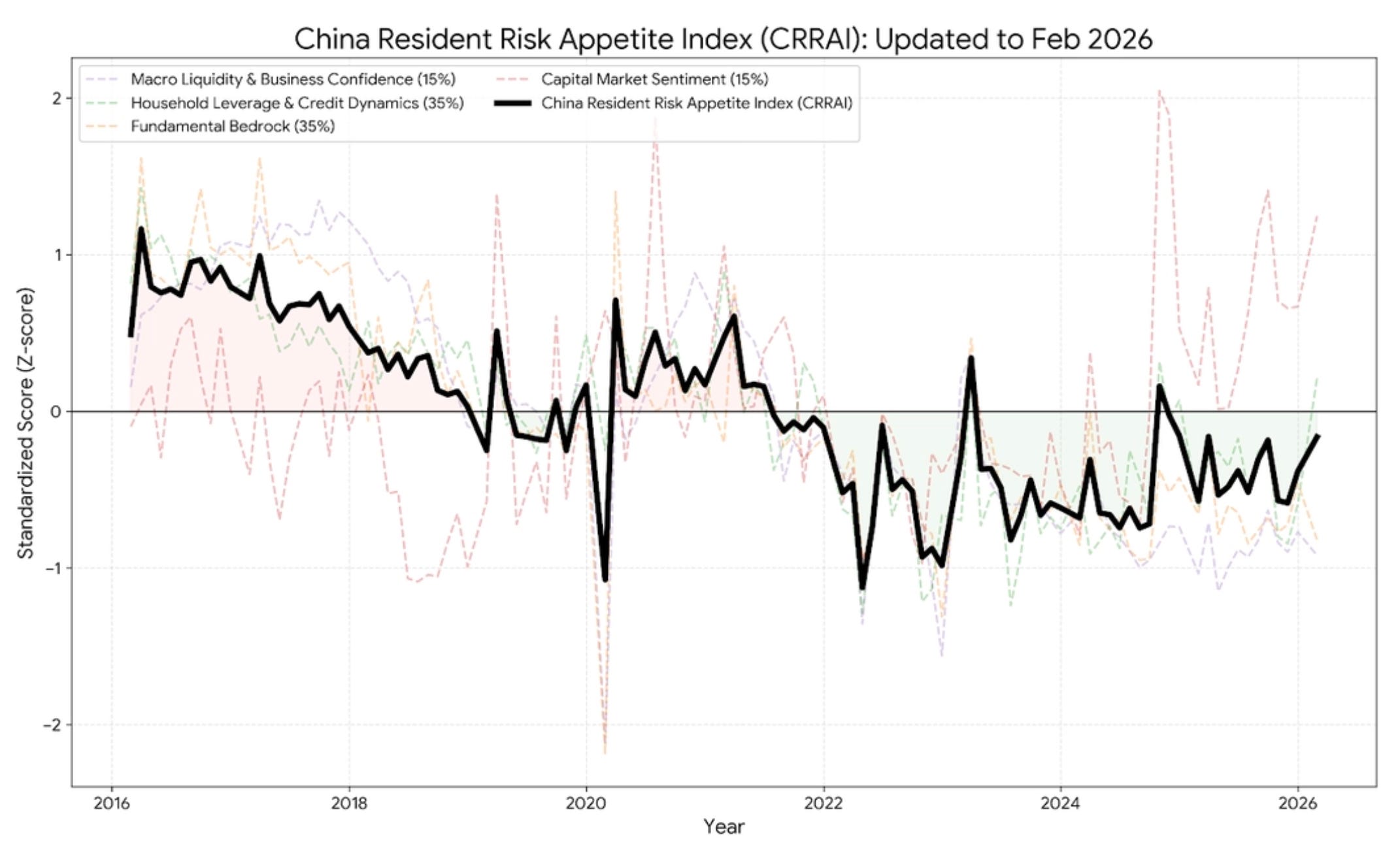

Fundamentals — we are seeing an improving trajectory. Our proprietary China Resident Risk Appetite Index (CRRAI) showed improvement in January and February.

* CRRAI quantifies Chinese household financial confidence and risk-taking appetite, and consists of the following components.

Macro & Business Confidence (15%): Tracks liquidity and growth using M1-M2 spreads, government bond yields, and PMI data.

Household Leverage & Credit (35%): Measures willingness to borrow, mortgage/consumer loan growth, and deposit trends.

Real Economy Foundations (35%): Monitors asset values and income security through second-hand housing prices, transaction volume, and employment.

Capital Market Sentiment (15%): Captures “animal spirits” via financing ratios, valuations (P/E), trading intensity, and new account openings.

All indicators Z-score standardized against the 2014–2026 history.

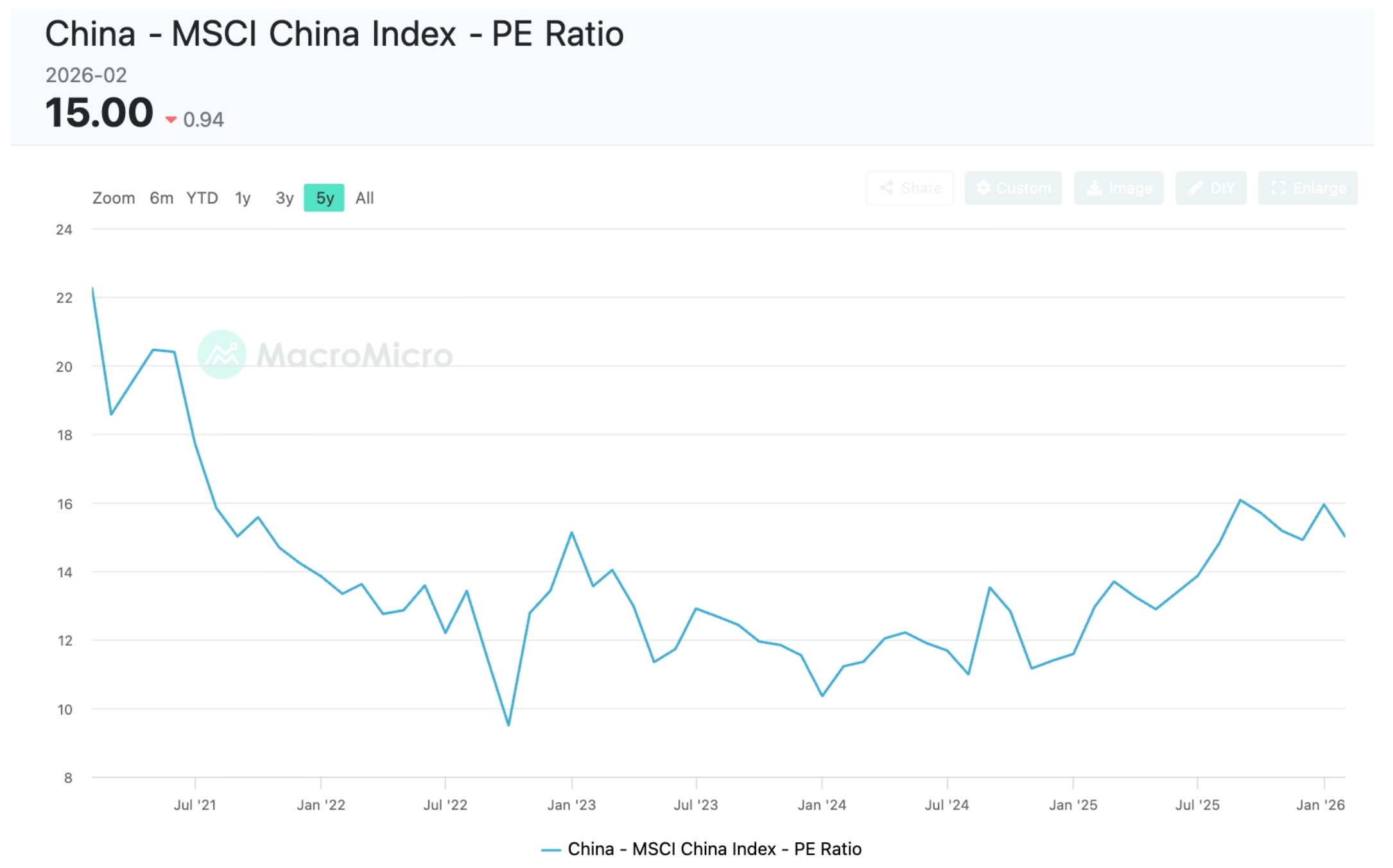

Valuation — not expensive, not a screaming buy. China is not uniformly cheap anymore after the recovery since 2025, but it still offers reasonable value.

Sentiment

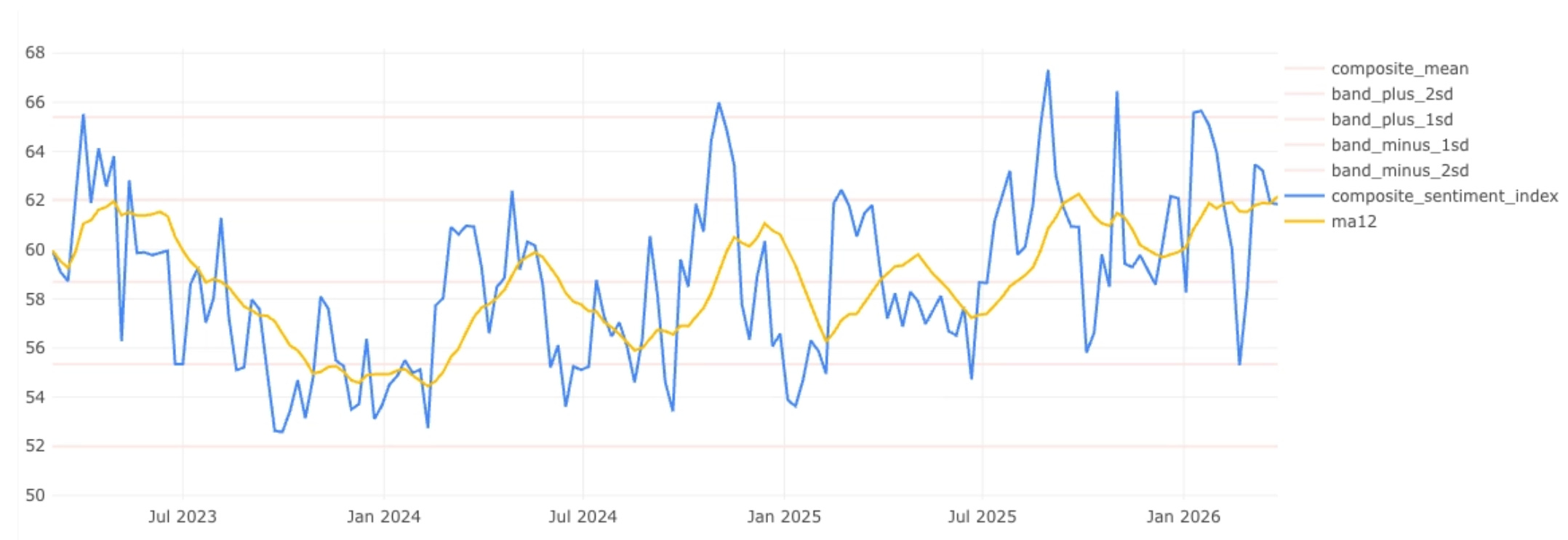

Retail Sentiment Index

Data is sourced from China’s major retail stock communities, with high-frequency, full-spectrum tracking of individual investors’ sentiment toward specific Chinese assets and the broader market. The sentiment index is constructed by fitting post-level semantic analysis, discussion volume, posting frequency, and directional (bullish/bearish) tone.

Historical analysis shows that every time the index reaches a standard-deviation extreme, the market has subsequently experienced a mean-reverting correction—either cooling from excessive optimism or warming from excessive pessimism.

Since the onset of the US-Iran conflict through early March, A-shares have demonstrated notable resilience relative to other emerging markets. Retail sentiment indicators are now flashing clear signs of a rebound. Drilling into the sub-components, investor enthusiasm for hard technology, upstream resources, and cyclical sectors has risen sharply during the period. At the same time, previously underperforming segments have shown no further deterioration; the positive and negative forces have largely offset each other, resulting in an overall improvement in market sentiment.

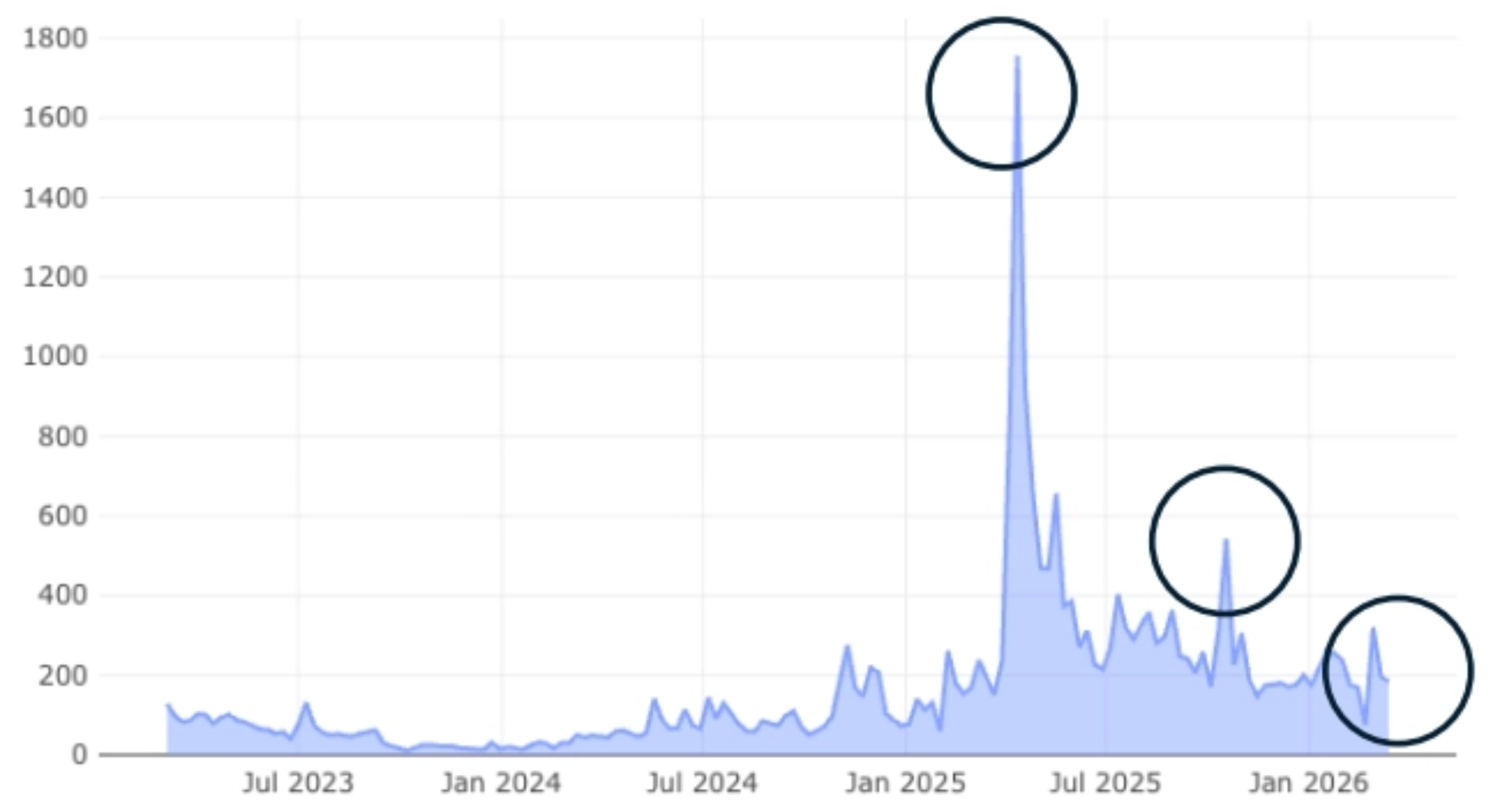

Retail Sensitivity to Sino-US Relations

Since the second U.S.-China tariff conflict of 2025, A-shares have traded steadily with limited volatility. On the sentiment side, retail investors’ sensitivity has been markedly lower than during the April tariff clash. Despite extensive media coverage, individual investors’ attention in the stock market has not escalated into extremes. More recently, the expected Xi-Trump summit has triggered a modest sentiment rebound, though the magnitude remains notably restrained.

Institutional Sentiment Index

Data is sourced from research reports from a selection of top global investment banks. The tracking monitors their analyses of capital flows into Chinese assets, macro policy outlooks, sector-level developments, and individual stock perspectives, while identifying shifts in cross-border asset allocation toward China, directional sentiment (bullish/bearish), and overall market confidence levels.

Recent data shows that foreign institutional investors’ confidence in allocating capital to Chinese assets has risen sharply. Sector and stock-specific outlooks are gradually improving, and views on China’s macroeconomic stability remain solidly positive.

Wildcards: The escalation of the Iran conflict has rattled Asian markets, but not all of Asia is equally exposed. China actually sits in a more defensive position, holding large strategic and commercial oil reserves that help cushion short-term disruptions. It has also spent years diversifying its supply toward Russia and Central Asia.

In contrast, Japan relies on the Middle East for roughly 90% of its crude oil imports. South Korea sources about 70% of its crude from the region and routes over 95% of that through the Strait of Hormuz.

We think A-shares carry a structural cushion that most markets lack: the “national team” actively intervenes when needed, reducing correlation to external shocks in ways that are hard to replicate elsewhere in the region.

Despite its cushions, a sustained surge in oil prices will inevitably weigh on China’s economic fundamentals and industrial margins. Global hyper-inflation will erode household spending power worldwide. Even if China remains stable domestically, its export engine will stall as demand from its primary global customers collapses.

Therefore, while China currently appears more resilient than its neighbors, a significant escalation—specifically the introduction of ground troops or the transition into a protracted war—would fundamentally sour our short-term outlook on the Chinese market.

Q2 Themes We’re Watching

These are the areas we plan to cover in depth over the course of Q2.

Shareholder return & dividends

Chinese companies — particularly SOEs and large-caps — have meaningfully accelerated buybacks and dividends over the past 18 months. This is a structural shift, not a one-off. In an environment where earnings growth can be uncertain, capital returns provide a floor. To be frank, Chinese equities are less about high-flying growth or “moonshot” stories like U.S. tech. Much of the investment value — and a large portion of the economy — is concentrated in dividend-paying large-cap companies. In the current rate environment, yield becomes even more relevant.

However, many popular dividend indices are heavily tilted toward banks and energy companies, which carry increasing risks after the rally.

We’re building a more balanced, focused list of names where the yield is real, the balance sheet supports continuation, and the stock isn’t already priced for it.

Robotaxi