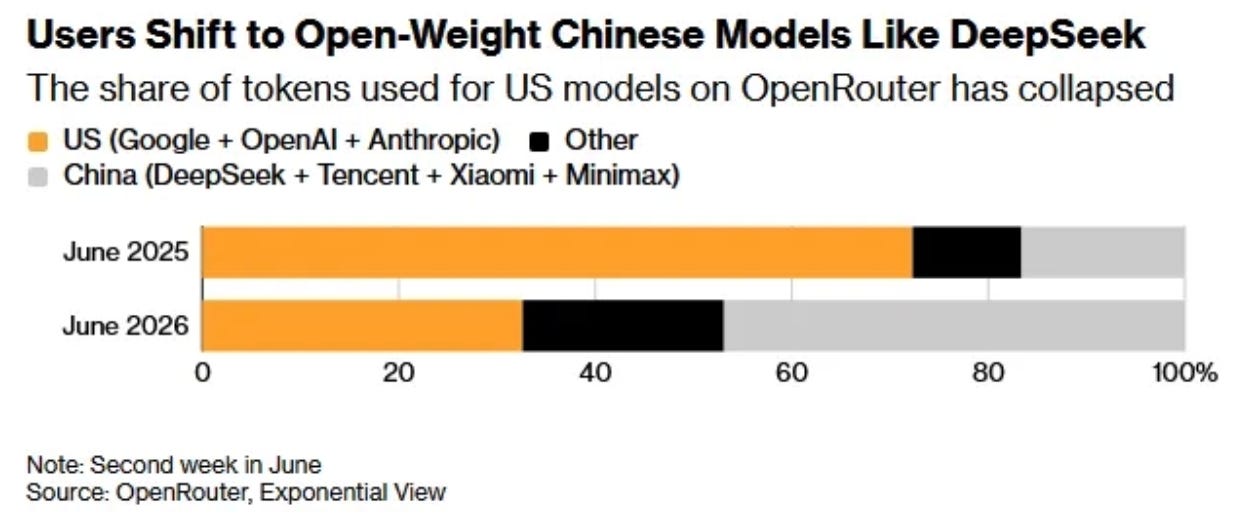

Start with one number that does not feel possible: In late 2024, Chinese open-weight models were under 1.2% of the tokens flowing through OpenRouter, the largest neutral marketplace where developers route API calls across hundreds of models. By June 2026, Chinese models had become the majority, and US models had fallen from roughly 70% of the platform to about 30% in twelve months [*]. That’s what developers around the world actually chose to pay for when nobody was watching the brand.

Amid the backdrop of Chinese companies going abroad, a new phrase has been coined in China to describe this phenomenon: “token 出海” (tokens going abroad). In today’s newsletter, I want to share some of my recent reflections: how real this trend is, why it’s happening now, who’s selling, and the investment implications behind it.

The “token export” trend is growing faster than anyone expected

The reason to trust the OpenRouter numbers is that OpenRouter doesn’t run any models itself. It’s a switchboard — it takes your request and sends it to whichever provider fits your price and latency, so its data captures genuine demand rather than marketing. And that data is stark. Chinese models surpassed US models on the platform for the first time in the week of February 9, 2026, and accounted for 61% of consumption among the top ten models, holding the top three spots.

Although the 61% figure represents the top ten models rather than all 400-plus models hosted on the platform, the overall direction is undeniable.

The market itself has also exploded. OpenRouter has scaled nearly 5× in the past six months, from roughly 5 trillion tokens per week to over 25 trillion in May 2026. This means China didn’t just gain market share; it took a bigger slice of a much bigger pie. Furthermore, a16z’s Martin Casado also estimated that roughly 80% of startups utilizing open-source AI stacks are running Chinese models.

Inside China, the curve is even steeper. Average daily token calls went from 100 billion in early 2024 to 140 trillion by March 2026 — more than a thousandfold in two years, per the National Data Administration (NDA). And Beijing has started treating tokens less like a technical artifact and more like a commodity you can meter, price, and export.

In March 2026, the NDA formally standardized the Chinese word for “token” (词元, cí yuán) and its director described tokens as measurable, priceable, and tradable. And in April, the port city of Shantou completed what officials called China’s first city-level “closed loop” for token exports: servers in China generate the tokens, an API call comes in from Southeast Asia, the answer goes back out, all under a compliant cross-border data arrangement. Nothing physical crosses the border — just the inference result.

Regulatory compliance still needs to be fleshed out, but the trajectory is clear—China views tokens as its next goldmine amid the global race for compute dominance.

Why it’s happening now: the frontier gap closed, and tokens got expensive

Two things happened in the last year that made this trend possible.

First, the performance gap between frontier models and other open-weight models is narrowing.

Stanford’s 2026 AI Index — the most-cited scorecard in the field — put the top US model just 2.7% (39 points) ahead of the top Chinese model as of March, down from a 17.5~31.6 point difference in mid-2023. Stanford’s own word for it was “nearly closed.“

In academia, the returns on all model training spending are also visibly shrinking: annual gains on the MMLU benchmark fell from 16 points in 2021 to under 4 in 2025 even as R&D budgets ballooned, and roughly half of the major benchmarks are now saturated — everyone clusters near the top, so the scores stop meaning much.

For the ordinary user tackling daily tasks, the difference between the number-one and number-five models is becoming nearly impossible to distinguish. After all, not every job is rocket science requiring a frontier model; for the majority of personal and business scenarios, a much cheaper model suffices.

My empirical observations are similar. In my own coding and software development projects, I don’t find a large enough difference between, say, GLM 5.2 and Claude Fable to justify the price premium. I’ve also tested these models on non-coding tasks—such as suggesting product improvements, brainstorming design solutions, or architecting system-level engineering robustness—and in most cases, they yield identical alternatives.

The second thing is that ”tokenmaxxing“ is ending. Enterprises are reevaluating ROI.

Management went from going all-in on agents to introducing monthly limits on tokens and model tiers in less than a year. As frontier model costs rise, enterprises are now exploring lower-cost, open-weight, or in-house options that ensure proprietary data ownership.

For instance, Palantir’s Karp has openly criticized “tokenmaxxing” as a viable business model, noting that several of its US clients supporting critical infrastructure are already running open models (NVIDIA’s open model) [*].

These exact shifts give China’s open-weight models a distinct competitive edge.

China’s token export playbook

There are two distinct export routes.

The first route is to move only the tokens. The power stays in China, the servers stay in China, the model runs in China, and what crosses the border is the answer, delivered by API. That’s the Shantou model, and it’s where most of the OpenRouter volume actually lives. It turns cheap Chinese electricity into a services export with no containers and no tariffs.

Among China’s frontier labs, DeepSeek is closest to a “pure technology export” and acts as the industry’s price anchor. Operating with no prioritized B2B or B2C application strategies and no overseas offices, its global influence spreads purely through its open-weight models adopted by tens of millions of developers worldwide.

Zhipu AI (2513 HK), deeply Tsinghua-rooted, bases its strategy on three distinct pillars: MIT-licensed open weights, agentic coding, and—most distinctively—sovereign compute. Its GLM architecture is trained and served heavily on Chinese domestic accelerators (including Huawei Ascend, Moore Threads, Cambricon, and Kunlunxin). Its revenue is heavy on B2B and B2G, with 85% of its H1 2025 revenue coming from on-premise deployments to Chinese SOEs and financial institutions. However, it is racing to catch up with Western frontier labs—recently reported to match Anthropic’s Claude Fable 5 on specialized cybersecurity tasks.

Moonshot AI’s Kimi-K2.6 is arguably the premier open-weight native multimodal model on agentic benchmarks, capable of orchestrating up to 300 parallel sub-agents for autonomous coding loops. Commercially, it is the fastest-inflecting lab in the cohort: its Annual Recurring Revenue (ARR) surged to $200 million by April 2026, and its models are reportedly feeding Cursor’s training — meaning it’s already inside the Western developer-tool supply chain.

The second route is to export tokens, applications, and ecosystems simultaneously. Among Chinese labs, consumer-facing applications mostly dominate.

MiniMax is the consumer exporter, drawing about 70% of its 2025 revenue from overseas, driven historically by consumer apps (Talkie companion app, Hailuo video) and now increasingly by the multimodal capabilities and M-series API, whose M2.5 briefly led all of OpenRouter. Although Moonshot also derives revenue from its B2C applications, its user base remains mostly domestic as of now. MiniMax is, by a wide margin, the company earning the most overseas C-end revenue among the Chinese AI players.

Alibaba (Qwen) is China’s leading player in exporting a full-stack B2B ecosystem. It consolidates its models, cloud infrastructure, and chips under the Alibaba Token Hub (ATH) business group, and is rapidly expanding its data center footprint globally across South Korea, Malaysia, the Philippines, Thailand, and Mexico.

A massive driver of this global B2B strategy is the high volume of international developers downloading Qwen’s open-weight models from Hugging Face to host them locally. Ultimately, Alibaba’s play is to commoditize these open-weight models so that global clients become structurally locked into renting Alibaba Cloud’s compute ecosystem to deploy them.

What holds it back

The most important constraints are trust and jurisdiction, not capability.

Under China’s 2017 National Intelligence Law, companies must cooperate with state intelligence work, so every API call landing on a China-hosted endpoint carries an exposure no price cut can fix. But because the weights are open, Western hosts like Fireworks and Together serve the exact same models without any data touching China, at roughly double the first-party price — still cheap.

Nevertheless, enterprise adoption of Chinese models remains overwhelmingly low compared with that of smaller startups and individual users. Regulated, high-stakes workloads in finance, healthcare, and government stay with Western proprietary models.

Large enterprises still overwhelmingly buy from Anthropic, OpenAI, Azure, and Google Cloud, and US labs still capture most of the industry’s actual revenue even while losing volume. For instance, Anthropic holds ~12% of token volume on OpenRouter but captures ~46% of revenue [*].

Apart from the obvious geopolitics and regulations, localized sales execution is a real challenge faced by Chinese AI labs that wish to go B2B abroad.

One interesting story I heard from a friend in the industry shows the level of localization needed: one of their clients ended up choosing MiniMax’s voice model because it was among the only models that could provide a voice solution with the specific regional accents the client was looking for in that market. Despite the hype about AGI, the reality is that the sheer amount of detail required for localization still demands significant on-site, attentive human effort.

B2B sales require a strong local sales and marketing team to build client relationships —this means considering the nuances of language, business practices, and even local culture. This is the area where many Chinese companies still lack, despite their strong technical capabilities and excellent price-to-value.