"Charts of the Week" is Baiguan's series that features key data points to help you quickly grasp the general state of affairs in China in just a few minutes. We handpick the highlights of the data charts from a variety of sources, analyzing and delivering insights trusted by 100+ top institutional and corporate clients worldwide at BigOne Lab. Don't forget to subscribe before you continue reading!

Since the unprecedented policy shift in September 2024, which sent Chinese equities surging, the market has remained relatively neutral. Despite some subsequent policy announcements, most have failed to meet the high expectations set by the initial rally. The Hang Seng has gained 10.40% over the past six months, but most of that gain came during the late September surge.

A natural question now is whether Chinese equities are poised for another rally in 2025, especially since the "value correction"—the "easy" argument for a potential bull market—has largely been priced in following the 2024 rally.

For those interested, I’ve covered the policy developments of 2024 in this YouTube video, explaining why these measures were considered "unprecedented," as well as offering my thoughts on what to expect in 2025. Robert Wu has also highlighted a few key equity themes to watch for in the new year in this substack post.

With Chinese New Year approaching (Jan 29), we may see a slowdown in market activity as investors wait for further clarity, especially regarding Trump’s tariff policies. In today’s newsletter, I’ll highlight a few important time stamps and themes to keep an eye on in Q1 2025.

Trump's (exact) tariff policies & US fed rate cuts

China’s long-term government bond yields have been plummeting to new lows at an alarming pace toward the end of 2024, prompting the People's Bank of China (PBOC) to suspend its government bond purchases.

At the same time, expectations for US rate cuts have recently dimmed in expectation of persistent inflation. The widening yield gap between China and the US still remains a major concern for global asset allocators.

Since the onset of the US-China trade war, China has increasingly built factories overseas. I would specifically keep an eye on whether Trump will raise tariffs specifically for China (which would leave China better prepared than during the 2018-2019 tariffs with factories overseas) or impose tariffs universally on global countries, which would present a larger headwind for the Chinese economy. (So far, at the time of writing, Tuesday, January 21, it looks like universal tariffs are the most likely scenario, as Trump has just announced plans to impose tariffs on both Canada and Mexico starting in February.)

RMB may face further depreciation and capital outflow momentum still looms with the widening yield gap. Although the PBOC's intervention with RMB rates now may be the way to save some bullets until there’s more clarity on Trump’s trade policies.

It would be too early to draw premature conclusions, as the negotiations will undoubtedly involve uncertainty and unexpected turns of events. In the short term, however, I believe these two factors still remain the biggest macro headwinds to watch for Chinese equities overall.

The "Two Sessions" in March: more specific policy announcements

March will be a critical month as the National People’s Congress and the Chinese People’s Political Consultative Conference meet to release more details on policy.

As a general practice, the Politburo meeting in December 2024 sets the general direction for development, the Central Economic Work Conference, also held in December 2024, outlines specific economic policies, and the National People's Congress in March this year will focus on concrete targets and plans.

Real Estate: Since the stimulus package was announced back in September 2024, the real estate market in China has largely rebounded and stabilized. According to the panel we track at BigOne Lab, the parent company of Baiguan.news, existing home transaction values have shown double-digit year-on-year growth across 140+ cities in China.

As the real estate market stabilized, back in December 2024 during the Central Economic Work Conference, there weren’t many new concrete plans introduced for the real estate sector. However, the sector still faces challenges, with both transaction values and prices experiencing downward pressure as we approach the Chinese New Year in January this year.

Real estate remains a key concern for the economy, with second-home values heavily influencing consumer confidence as a core asset for many Chinese households. Any updates from the Two Sessions could be a game-changer.

Consumer Spending & Stimulus: During the December Work Conference last year, boosting domestic consumption was elevated to the top priority—an unprecedented move that highlights the Chinese government’s determination to stimulate spending.

However, the specifics of how this goal will be achieved remain unclear. Key questions, such as the exact scale of the stimulus package, whether changes to social security or pension systems will be introduced, and the specific stimulus programs, are yet to be answered. We expect more clarity during the "Two Sessions" in March.

Policy implementation in China often takes a gradual, incremental approach rather than bold, sweeping reforms. It’s likely the government will focus on smaller-scale measures, such as issuing consumer vouchers for specific goods or targeting selected cities, rather than deploying massive cash injections upfront.

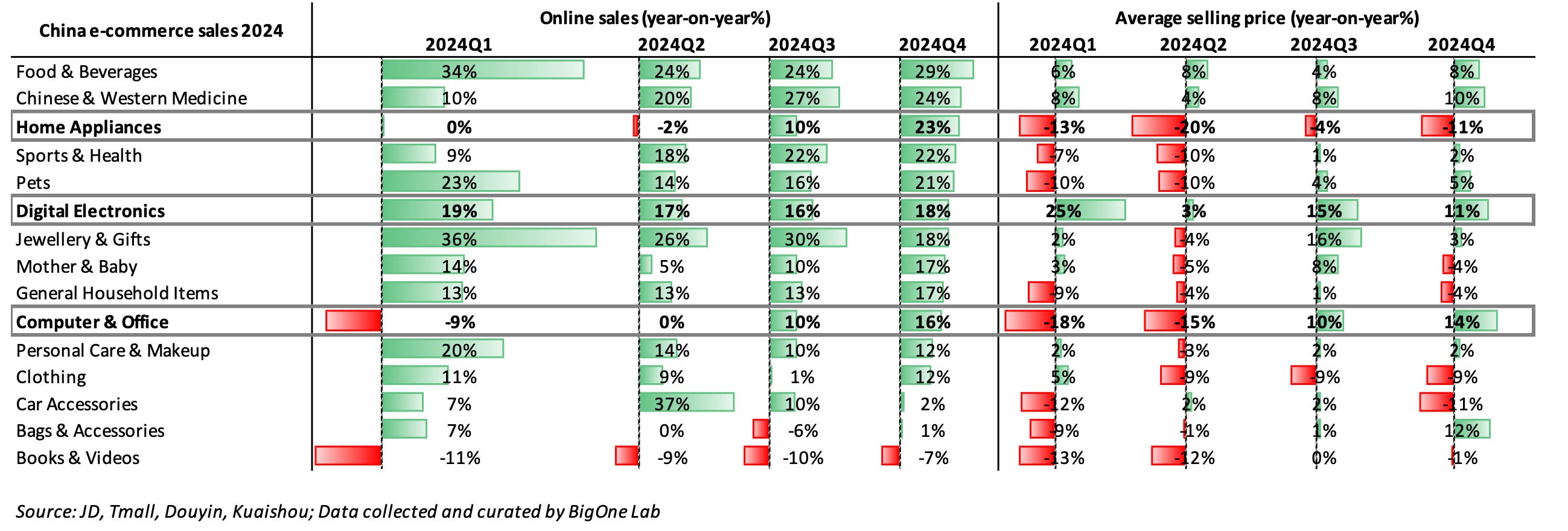

For instance, since September last year, vouchers have been given out for major appliances, computers, and digital electronics, including mobile phones. In Q3 and Q4 of 2024, these categories—especially home appliances and computers, which saw negative growth in the first half of 2024—saw a noticeable rebound in online sales. (We tracked this data across China’s major e-commerce platforms, including JD, Tmall, Douyin, and Kuaishou.)

This suggests that vouchers can drive growth. However, a broad rebound across all spending categories this year is not guaranteed, as items like major appliances and computers are generally not repeat purchases. So in 2025, it will be important to keep an eye on how these incentives evolve and which categories will be targeted in the coming months.

Behind the paywall, I'll continue with recommendations for key trends to watch and opportunities to consider in domestic consumption, including the latest Q4 2024 online sales comparisons for Tmall, JD, Douyin, and Kuaishou. I’ll also cover the third major theme to watch: the overseas expansion of China’s tech giants. To get a sense of what is offered, you are welcome to check out this older post in the same series: Charts of the Week. You can also get free access by sharing us.

This post is sponsored by BigOne Lab, our parent company. BigOne Lab proudly announces the introduction of the China Mobile Payment dataset, covering high-frequency offline sale performance of brands such as LULU, Hermes, LV, Starbucks, POP MART, Miniso sportswear, luxury, coffee and tea chains, and specialty retail sectors that were previously undercovered by data. If you are interested in subscribing, please contact more@bigonelab.com

In terms of investment, some opportunities do stand out: