China market's epic rally: how sustainable will it be?

Top 5 areas of concern that we are closely monitoring while we enjoy the ride

Something huge happened in China last week.

A raft of positive policies and policy messaging have finally signaled a real pivot in China’s economic policy. In response, the market sentiment that has been held back for so long has erupted like a volcano. In Shanghai, the stock index returned ~13% in a week, which is the best trading week in 16 years. Hong Kong's market was even more extreme and just notched its best weekly gain of this century. The strong sentiment has continued at the time of writing this newsletter.

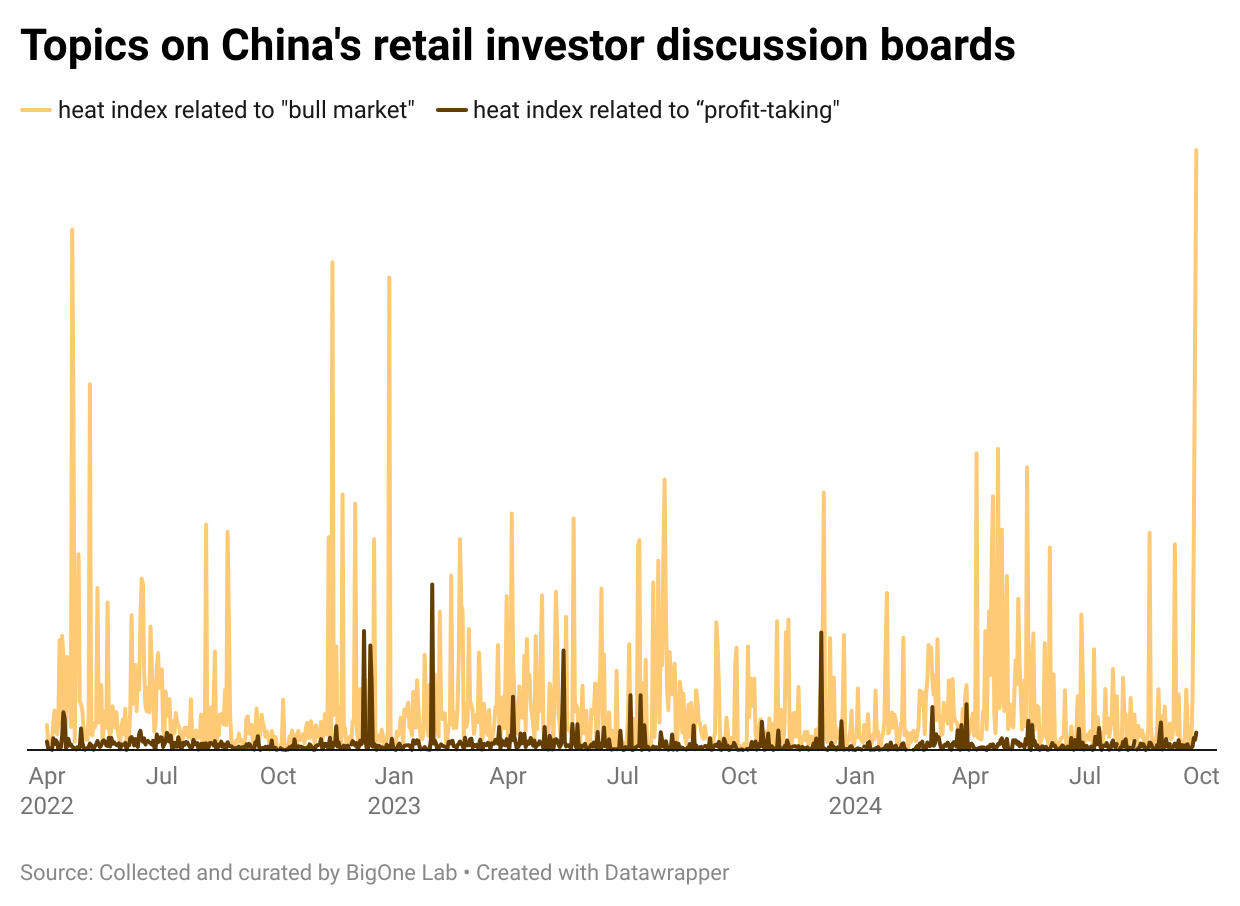

Retail investors, many of whom were hurt so much to have left the market, are rushing back in. The stampede was so huge that even Shanghai’s stock exchange’s trading system had a glitch. According to BigOne Lab’s retail investor sentiment data, discussions related to the “bull market” have reached a multi-year height as early as on Sep 27, while discussion related to “profit-taking” has remained subdued, showing positive retail sentiment is still at an early stage.

China’s stock markets have seen many false starts in the last few years. The natural question, after days of euphoria, is whether the current rally will be sustainable.

In this article, we will examine the top 5 factors that have contributed to last week’s historic rally, and we will also list out the top 5 areas of concern that will determine whether this rally will stay alive.

The top 5 factors include:

Unorthodox approach to the stock market

Blunt recognition of key economic pain points in real estate and unemployment

Strong willingness to resort to fiscal measures

A real sense of urgency from top leadership

A new mode of external communication that leaves open space for imagination and interpretation

The top 5 concerns that will determine whether the rally will be sustainable are:

The exact details of the fiscal stimulus package

Looming shareholder selldown

The potentially negative effect of the new M&A policy on the stock market

Re-adjustment of central-local relationships and fiscal reform

The “pendulum effect” swinging to the other extreme

The top 5 contributing factors

#1 Unorthodox approach to the stock market: fast-forwarding to the BOJ way

Of the press conference attended by the top 3 financial regulators last Tuesday morning, one policy move that has surprised many is the 500 billion yuan “swap facility” Governor Pan Gongsheng of PBoC announced. This unique policy device allowed financial institutions to pledge their assets to PBoC in order to get liquidity exclusively for buying up stock assets. Also, the central bank will also set up a 300 billion yuan special re-lending program that allows listed companies and major shareholders to borrow from commercial banks for share repurchases and increasing stakes. What’s even more, according to Governor Pan:

“I have discussed with [China Securities Regulatory Commission] chairman Wu Qing that we could consider unleashing a second round of 500 billion yuan, or the third batch of 500 billion yuan if the plan were enforced well enough,” he said. “We are taking an open attitude towards the new policy.”

It is still quite unconventional for a central bank to directly get into the stock market, and it is even more so for China. For veterans in the China market, so far we have only heard about policies that “prevent” hot money from getting into stock markets but have never seen money that can only be used for buying shares.

For context, it took the Bank of Japan almost 3 decades before wading into the stock market. So last week was almost like China’s central bank hit a fast-forward button and the whole “3 lost decades of Japan” seemed lost in the dustbin in an instant.

Up until today, the Chinese state only intervenes in the market with the so-called “National Team国家队”, a shadowy, “men-in-black”-style group of state-controlled entities surreptitiously purchasing up stocks, announcing no plans, revealing no identities, and making no statements to manage expectations. We don’t know who they are, how many shares they are going to buy, and when they will stop buying. We just know they exist.

This time is different. The PBoC, the mother of all money in China, effectively announces there will be unlimited support for the market.

Such a break from the past is also proof of the increasingly more central importance of the capital market in the minds of Chinese authorities now, seen as the potential next main financial engine to overtake land finance and bank financing. (I have talked about this historic transition here).

#2 Blunt recognition of key economic pain points in real estate and unemployment

The market has fretted for a long time about the bad situation in real estate and unemployment, and a perceived lack of concrete measures to combat those problems. On the one hand, housing prices across the country keep on falling with no end in sight, putting mounting strains on households, businesses, and local government’s finances. On the other hand, unemployment problems are rising, even though there are some bright spots in mid-tier cities and the manufacturing sector. What’s more worrying is the youth unemployment situation, which is only worsening.

Without solving our problems in real estate and unemployment, our domestic demand will not be healthy.

On these matters, China has been quite unequivocal this time. The language issued by the urgently called Politburo meeting of last Thursday (Sep. 26) on real estate was to “止跌回稳Stop falling and back to stable”. I think this is the first time ever that Politburo explicitly says the real estate market should “stop falling”.

On unemployment, last Wednesday (Sep 25), the Central Committee and the State Council jointly announced a top-level document on “就业优先employment first”, facing our unemployment problems front and center.

#3 Strong willingness to resort to fiscal measures

But how do you exactly stop real estate from falling further, how do you make sure employment comes first and how do you stimulate consumers to consume more, without some strong government spending, a.k.a. fiscal measures?

In fact, a perceived unwillingness to commit to tough fiscal measures has been a major hallmark of China’s policymaking in the last few years.

This time, although the exact details of the package have not been announced yet, the messaging has been unequivocal.

The Sep 27 Politburo meeting reads:

会议强调,要加大财政货币政策逆周期调节力度,保证必要的财政支出,切实做好基层“三保”工作。要发行使用好超长期特别国债和地方政府专项债,更好发挥政府投资带动作用。

The meeting emphasized the need to strengthen counter-cyclical adjustments in fiscal and monetary policy, ensuring necessary fiscal expenditures and effectively implementing the 'three guarantees' at the grassroots level. It is important to issue and utilize ultra-long-term special government bonds and special bonds for local governments to better leverage the role of government investment.

On Sep 26, the Ministry of Finance and the Ministry of Civil Affairs announced a special handout to the poor in order to celebrate the 75th anniversary of the PRC. It was not clear how large the handout was, who was qualified, and whether it was part of the budget approved back in April. But it does seem this was only intended a pre-holiday appetizer.

#4 A sense of real urgency from top leadership

What’s also remarkable is the sense of real urgency from the top leadership, which is evident in the time, the format, and the language of the Sep 27 Politburo meeting.

It is customary for the Politburo to meet 3 times each year in April, July, and November to discuss economic affairs, while this year, the April and July Politburo meetings have already taken place. Therefore, an “extraordinary” meeting held in September suggests the urgency of matters at hands. The economic situation has been precarious enough, while the international monetary conditions have softened enough following the Fed’s rate cut, that the top leadership in China must have decided to push for action now.

The language of the readout this time is also succinct, with little cliche, but mostly tough and precise language, all suggesting the no-bullshit nature of the intent.

Moreover, the fact that many groundbreaking policies were announced even before the Politburo meeting (such as the Tuesday press conference of financial regulators) also suggests speed is now taking precedence over preciseness.

#5 A new mode of external communication that leaves open space for imagination and interpretation

I am also genuinely delighted by Chinse authorities’ new way of external communication with the market.

In the Sep 24 press conference, our regulators went the extra mile to explain not just what’s being decided, but also what can be expected to happen. Beyond an RRR cut of 0.5 percentage points, Pan also said we can expect a further 0.25 - 0.5 percentage points cut. Beyond 500 billion yuan of facility to buy up shares, Pan is suggesting another 500 billion, and another 500 billion, ad infinitum.

By the end of the press conference, when a journalist asked Pan whether PBoC would also launch the so-called “stabilization fund”, a vehicle for the central bank do directly get into stock market operations, Pan did not deny and said it was “under study正在研究”, with an almost boyish laugh. The journalist was apparently caught off guard and had to laugh along with Pan.

This is “expectation management” done right. After all, the market is all about expectation. It’s about confidence for the future. When the expectation is set right, Pan may never even get to use his “another 500 billion”. But if expectation is not set right, no matter how many “500 billion” out there won’t be able to restore confidence.

The top 5 concerns that will determine whether the current rally will be sustainable

China’s stock markets have seen many false starts in the last few years. So, the natural question this time, after a whole week of euphoria is whether the current rally will be sustainable.

[The remaining content is exclusive for the paying members of Baiguan, who also enjoy 1) access to the member-exclusive Discord community, where we have had lively discussions about this topic in the last few days, and 2) free access to my personal newsletter, China Translated, where I give personal reviews of events in China that truly matter.]