Dear Baiguan Pro readers,

Each month, we pair macro data and BigOne Lab’s proprietary indices with a structured, directional read on where Chinese assets stand and what we’re doing about it.

If you haven’t upgraded yet, we’re offering a free upgrade to the Baiguan Pro tier for all existing paid subscribers through the end of Q2. Just reply with the email address associated with your subscription.

Macro & Sentiment Check

Our macro indices suggest that the market has entered a consolidation phase after the strong breakout testing seen earlier in the spring.

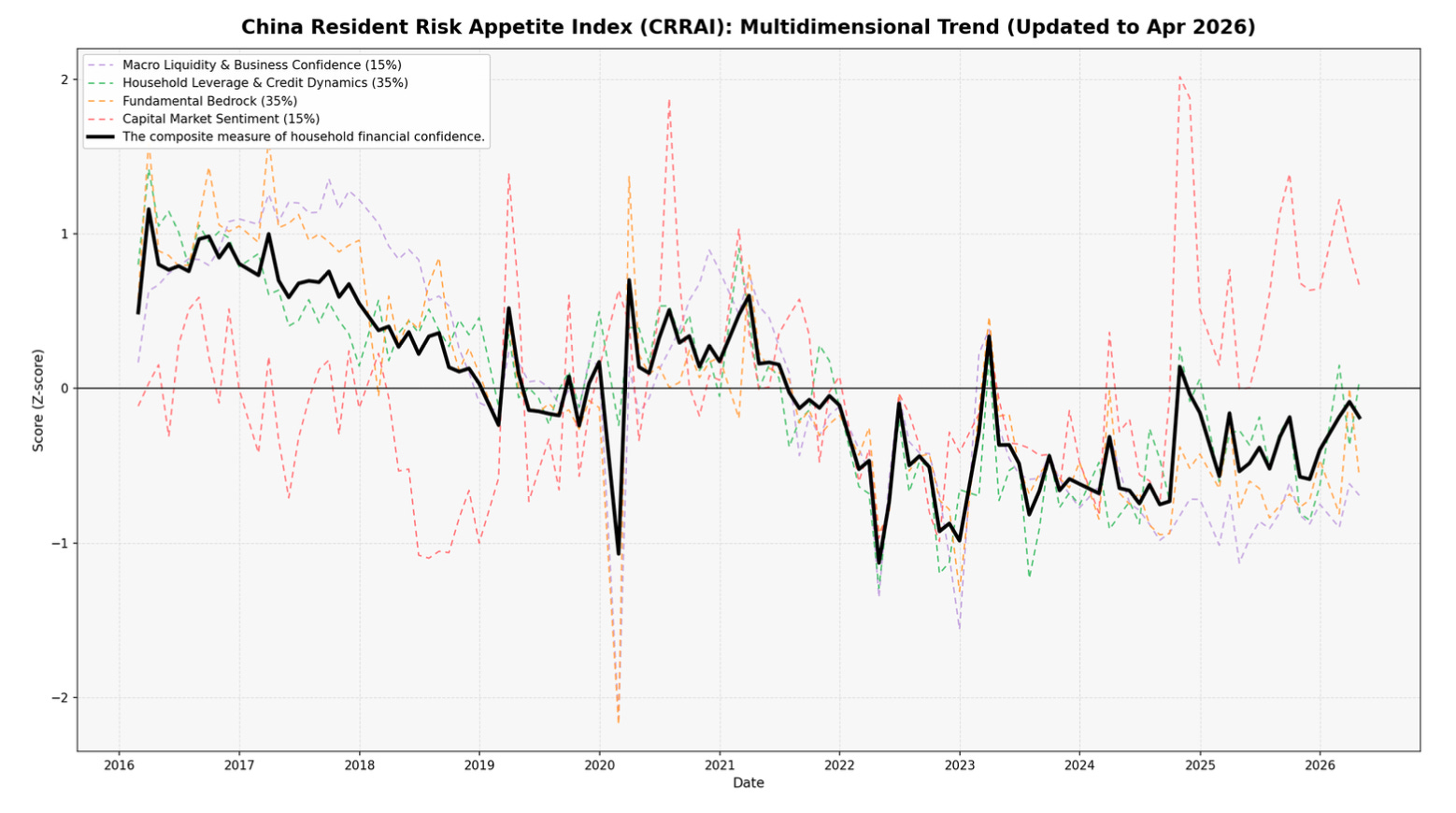

1. China Resident Risk Appetite Index (CRRAI)

Following March’s push toward neutral territory (-0.08), the April 2026 CRRAI composite reading recorded a tactical pullback to -0.19. The index remains materially above the late-2025 floor, but April did not confirm a clean break into neutral territory.

The recovery is still visible, but uneven: Capital Market Sentiment (+0.67) and Household Leverage & Credit Dynamics (+0.05) both remained in positive territory. This indicates that retail market psychology and balance-sheet momentum have not collapsed.

The primary weakness stems from the Fundamental Bedrock dimension, which slipped to -0.57. This is the most important constraint because it represents the household sector’s perceived safety margin through property prices, transaction activity, employment, and unemployment conditions. When this dimension is negative, speculative equity-market strength transmits less effectively into durable household risk-taking.

Macro Liquidity & Business Confidence also remained below neutral at -0.69. The practical implication is that the recovery needs broader confirmation.

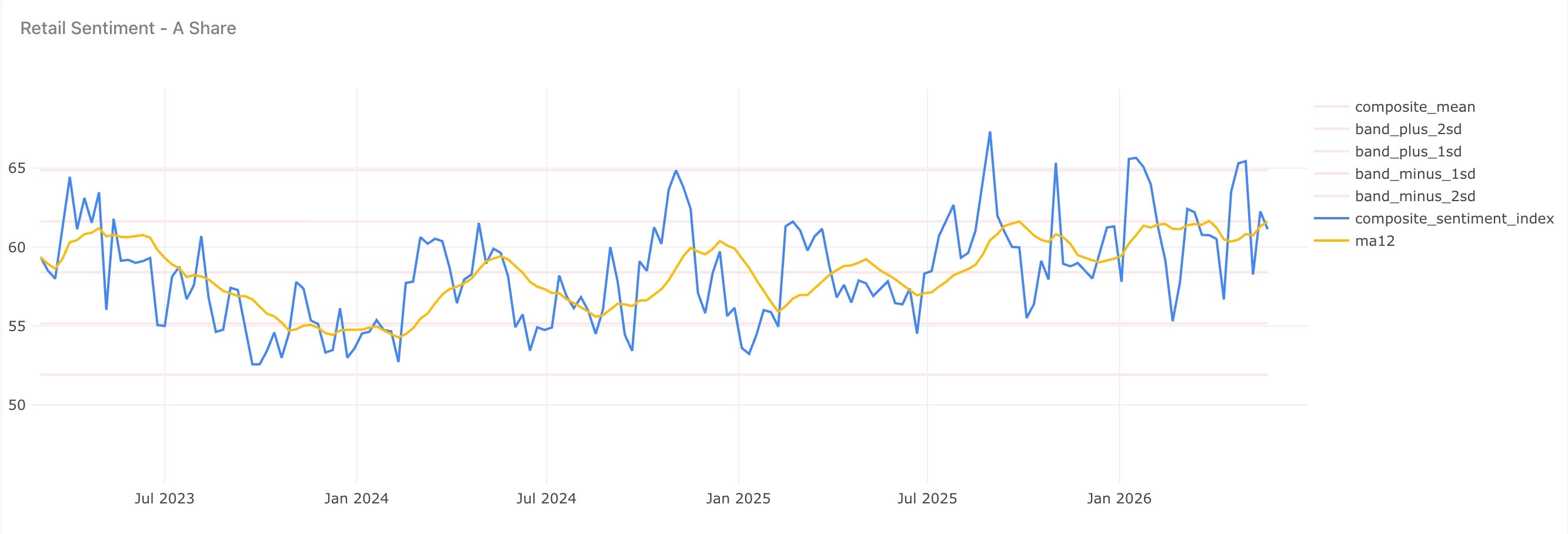

2. Institutional vs. Retail Sentiment

Individual retail investors in China remain steady but calm. While retail investors are actively participating, the market is not currently overheating into irrational optimism.

Big banks and international funds have become noticeably more optimistic about Chinese equities. After dipping slightly in April, institutional sentiment jumped sharply in late May, climbing to 0.59.