Has China's “Old” to “New” Economic Transformation Happened?

A survey of China’s job recruitment data

“Charts of the Week” is Baiguan’s series that features key data points to help you quickly grasp the general state of affairs in China in just a few minutes. We handpick the highlights of the data charts from a variety of sources, analyzing and delivering insights trusted by 100+ top institutional and corporate clients worldwide at BigOne Lab.

Understanding China’s true job market is complex. On the one hand, official data suggests the overall unemployment rate remains steady and healthy. On the other hand, if you live in China, you hear constant conversations about how difficult the job market has become and how salary growth has stalled.

This is a crucial question: gauging the health of Chinese households is essential to determining whether China can successfully transition into a consumption-driven economy, which depends on healthy, organic income growth.

So, what is really going on?

China’s economic structure has been undergoing a quiet transition from “old” to “new” over the past few years. Much of this shift was muted by pandemic news. While headlines consistently mention “industrial upgrading” (产业升级) or “New Quality Productive Forces” (新质生产力), it can be difficult to decipher whether this is actually happening on the ground. Today, we dive into online job postings data to find the answer.

Methodology Note: To map this transition, I classified millions of job postings from major recruitment platforms into six categories: New Productivity & Industrial Upgrade, Real Estate & Related, “Old Tech” & Traditional Manufacturing, Finance, Education, and Others.

The “New Productivity” category tracks the strategic pivot toward sectors like EVs, semiconductors, AI, green energy, biotechnology, etc. “Old Tech” includes industries that grew rapidly over the past decade—such as e-commerce, software, and internet platforms—which have increasingly matured into traditional industries rather than representing the current “cutting edge.” Other categories are self-explanatory.

While some cross-functional roles defy perfect classification, the massive scale of data since 2020 provides a definitive view of the structural transformation occurring over the last five years. (See the footnote for full definitions.)

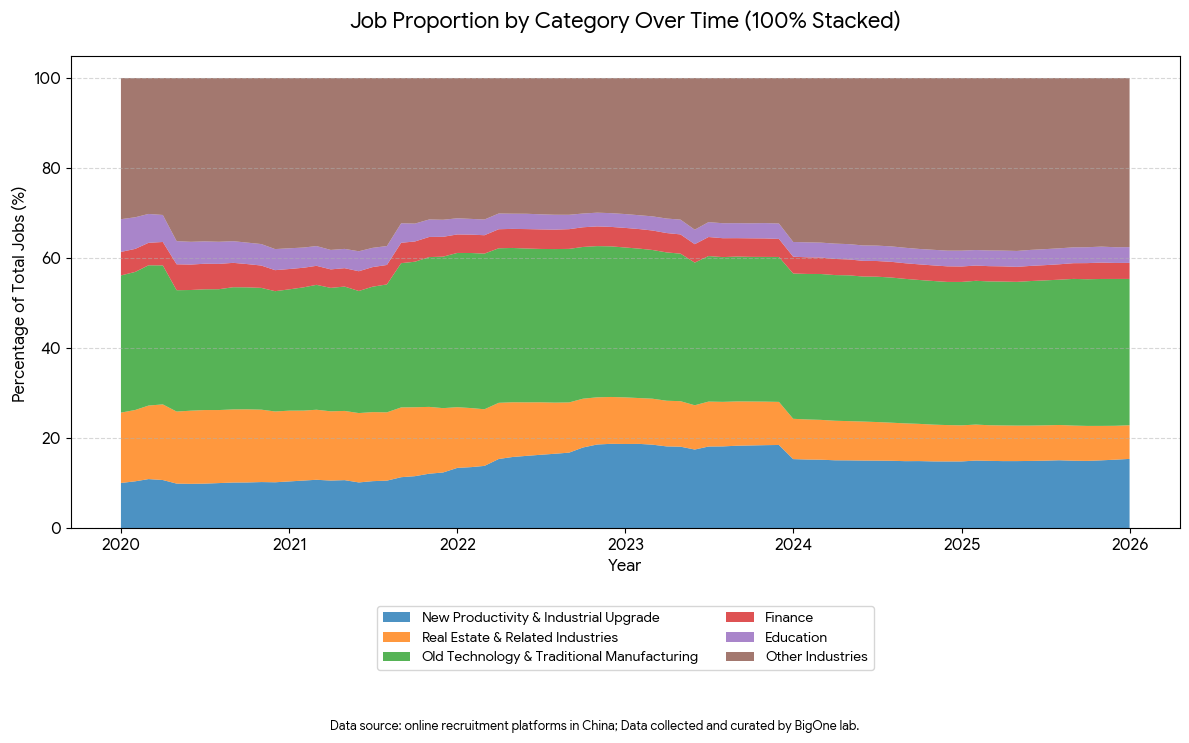

Q1: From “old” real estate to “new” productivity: has the transformation happened?

News headlines are swamped with news of China’s struggling real estate market (rightfully so, as listing prices for existing homes have yet to find a bottom). However, a quiet transformation has taken place within the job market. Since 2020:

The real estate and related industries (the orange area) have seen their share of total recruitment cut in half, dropping from 15% in 2020 to less than 8% by the end of 2025.

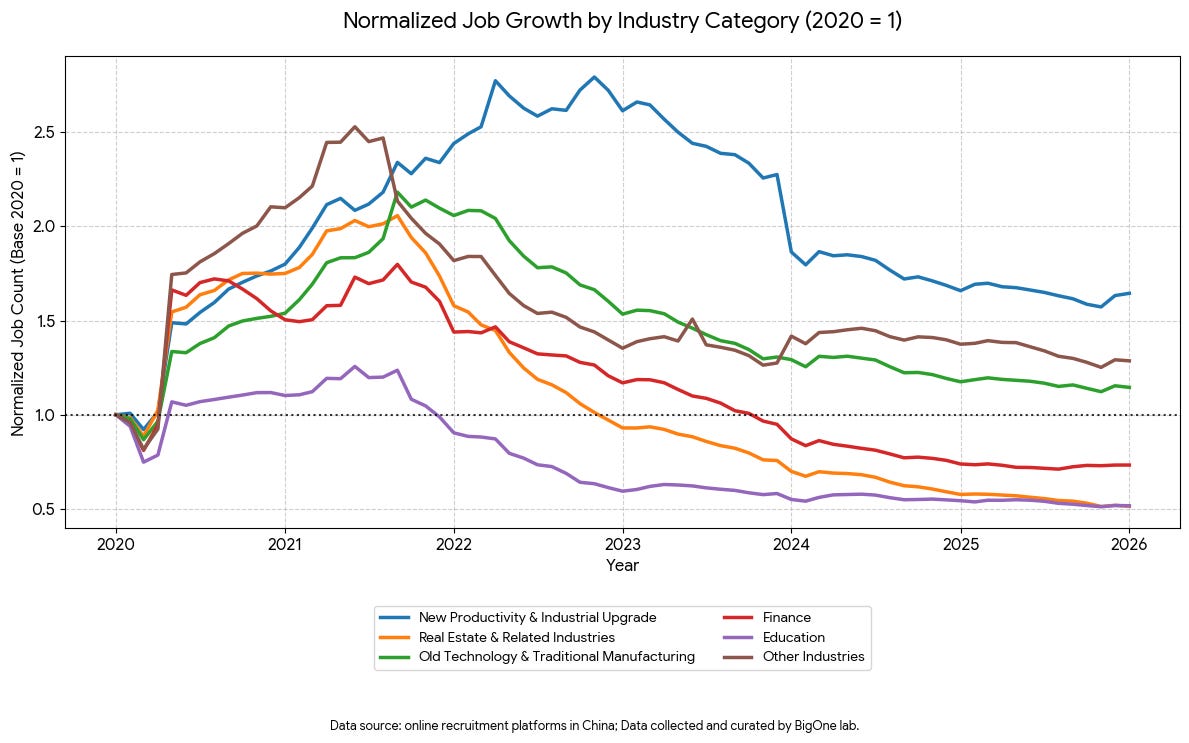

Simultaneously, the “New Productivity” sectors (the blue area) have shown powerful counter-cyclical growth, with their share of job postings climbing from 10% in 2020 to over 15.4% in 2025.

It is no coincidence that the added value of China’s real estate industry fell to only ~6.3% of GDP in 2024 [*]. (In my opinion, this partly explains why Beijing feels less urgency to launch a massive stimulus; real estate no longer influences overall employment as heavily as it did just five years ago.)

Despite the “structural pain” society is currently enduring, this shift proves the underlying logic of the Chinese economy has fundamentally changed. The absolute number of jobs created by the ‘New Productivity’ sectors (an increase of about 300,000 positions) has effectively offset the bulk of the losses in the real estate sector (a loss of about 350,000 positions).

The transformation of the “New” replacing the “Old” real estate is now firmly established in the trend data.

Q2: Why do on-the-ground sentiments feel so cold?

If the overall number of jobs has remained relatively stable and “Hard Tech” is booming, why is public sentiment so gloomy?

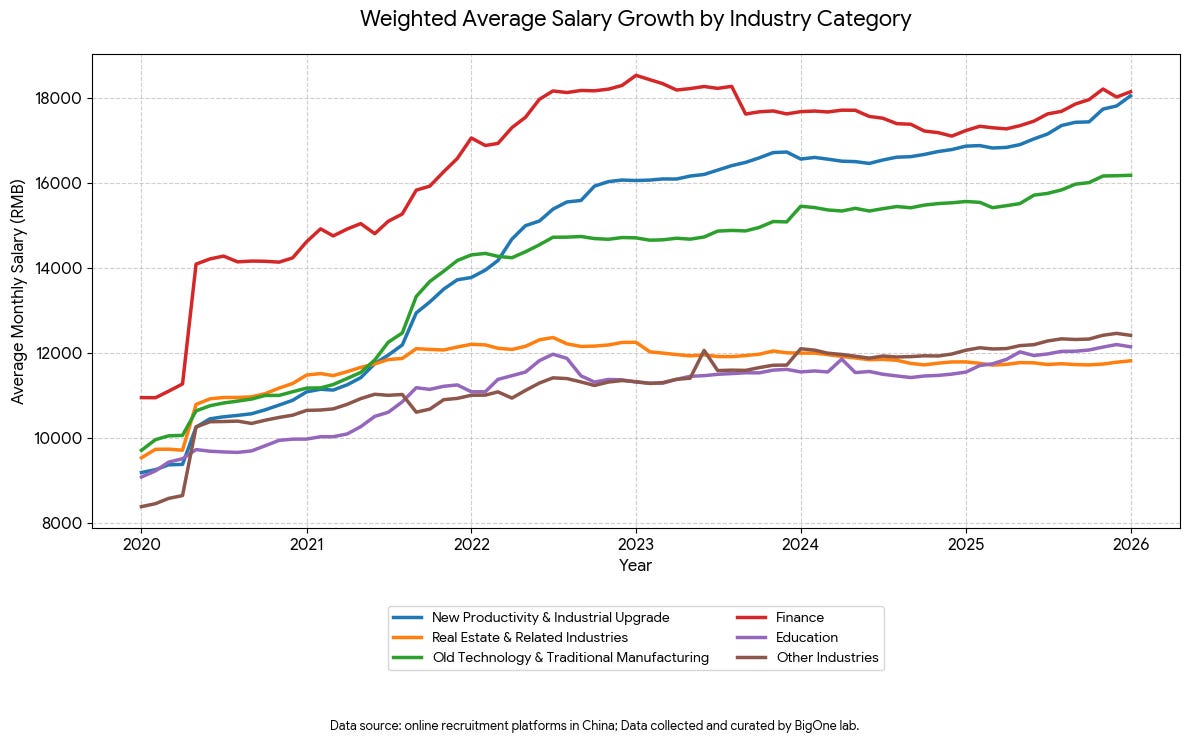

The answer lies in structural friction and a perceived “quality downgrade” for the middle class. Real Estate, Finance, and Education—industries that traditionally recruited a significant and highly educated portion of the population—have seen a consistent shrinkage in job postings since 2022, never recovering to pre-pandemic levels. These happen to be the three high-paying industries most favored by the university-educated, urban middle class (the demographic with the strongest voice on social media). These traditional sectors also still serve as a massive reservoir for the labor force, maintaining a share of roughly 32%.

For those who managed to keep their jobs in these industries, salary growth has been optimistic for them.

The new jobs replacing the old ones offer no easy transition. You cannot simply retrain a real estate marketing manager to design semiconductors or engineer hydrogen fuel cells. The booming “New Quality Productive Forces” require highly specific STEM backgrounds (often Master’s or PhDs). Meanwhile, the other side of the job growth spectrum—such as wholesale, retail, and local services—often represents a downgrade in social prestige and stability for university graduates.

This “talent incompatibility” is what creates the profound sense of a “job crisis” on the ground.

Q3: Are there other interesting insights and key takeaways for investors?

If you want to find the next structural growth opportunities in China, follow the hiring.

Trend 1: Consumer internet could soon become a “utility”

The era of hyper-growth for tech platforms and e-commerce—sectors that once defined the ‘cutting edge,’ provided the most sought-after roles for China’s top-tier talent, and made investors filthy rich—is over. When we examine the absolute job gains and losses across sub-industries from early 2020 to early 2026, the data paints a vivid picture of an economy executing a ruthless, structural pivot.