Is China's capital market on the brink of a major shift? State Council's 9 new guidelines for capital markets

[REMINDER] Exclusive "Ask Me Anything" live webinar on China on April 29, hosted by Sign up [here] before April 26 to secure your spot.Is there anything important about China's stock market? Perhaps people haven't realized yet that, with the decline of real estate as a major source of asset appreciation for Chinese households, the stock market may now be the only viable option for the middle class to hope for appreciating assets. Just like the US household benefited from the stock market during the past decades.

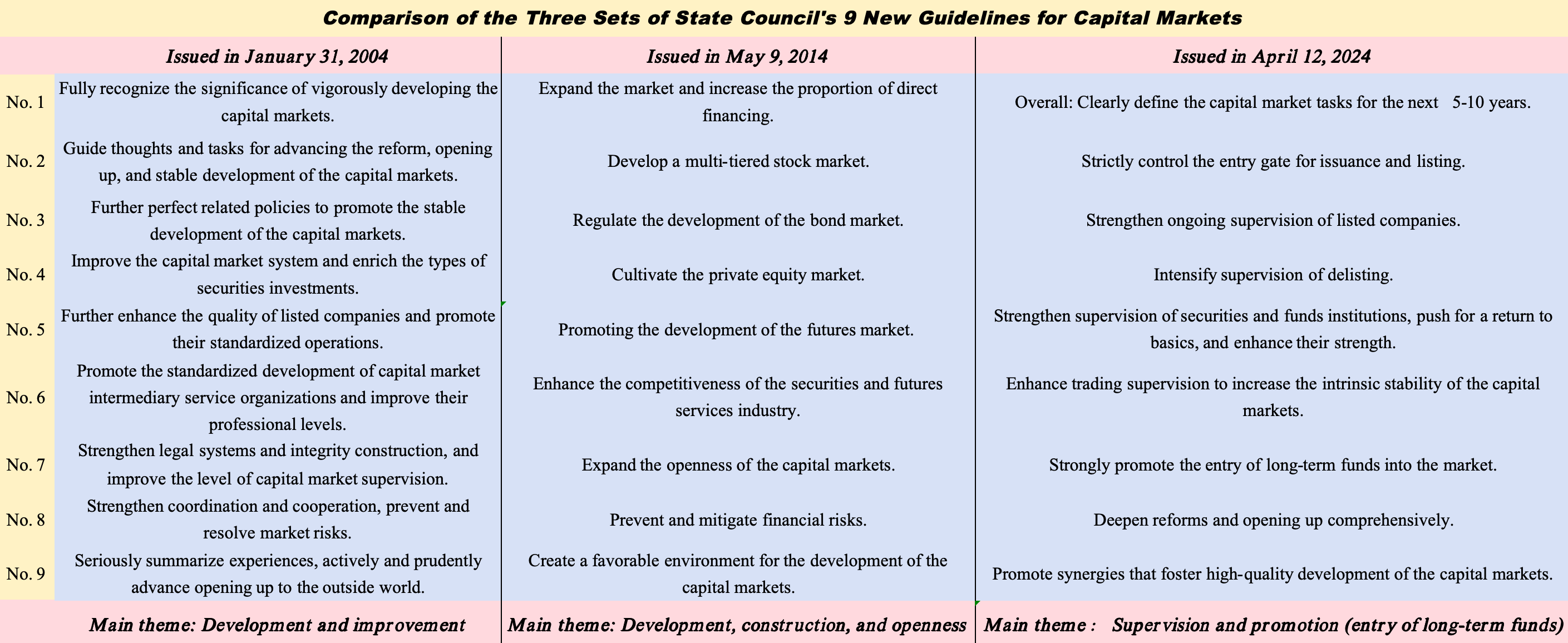

On April 12, Chinese domestic media outlets were abuzz with reports of a once-in-a-decade blockbuster boon for the A-shares market. Why such excitement? The reason lies in the State Council's unveiling of the "State Council's 9 New Guidelines for Capital Markets," dubbed "国九条." This designation stems from two factors: 1) The issuing body is the State Council, representing the highest echelon of governmental administration; 2) The document traditionally comprises nine distinct sections.

Interestingly, the "State Council's 9 New Guidelines" is not a standalone document. (I will abbreviate it to "Nine Guidelines" in the following post.) Historically, it has been issued every ten years, with previous versions launched in 2004 and 2014. These earlier policies were instrumental in setting the stage for major bull markets—most notably in 2007, when the Shanghai Composite Index reached an all-time high of 6,124 points, and again in 2015, soaring to 5,178 points. Similarly, the latest release of the new policy round came at a ten-year interval. After a prolonged period of the stock market downturn, everyone hopes that the A-shares will usher in a bull market.

While the "Nine Guidelines" have been widely discussed, penetrating analyses that fully grasp their implications are scant. We have aggregated and distilled in-depth analyses to offer our readers a comprehensive understanding of these pivotal guidelines and their potential impact.

Maybe then, we can answer the question: can the middle class in China really use the stock market to offset their declining salary?

A quick look: if there is any "novelty" in this policy

One of the main differences among the three "Nine Guidelines" policies lies in the different "missions" each undertakes.

The context of 2004 was to address the numerous issues caused by non-tradable shares prior to the split share structure reform, a problem unique to the Chinese market that foreign investors may not fully understand. We will not discuss this further for now.

The 2014 policy was implemented to expand the market, including measures to open it up further. In the ensuing years, we witnessed the opening of the northbound funding channels, with foreign investors increasingly buying into China. This period saw A-shares' inclusion in the MSCI Emerging Markets Index and a gradual increase in their weighting — a bull market fueled by foreign capital influx.

The most recent guidelines, issued in 2024, come against the backdrop of several years of declining performance in both A-shares and Hong Kong stocks. This policy round is primarily aimed at bolstering investor protection and enhancing the intrinsic stability of the market.

Key points

The newly announced "Nine Guidelines" directly confront the enduring challenges of China's A-share market, with each directive displaying a significant impact. Key points of focus include:

Strengthening IPO scrutiny and supervision of listed companies

A glance at the data from 2023 reveals that China's A-share market topped global charts in IPO financing amounts—a stark contrast to its lackluster performance (should I say, the worst performance worldwide? ). Despite underperforming, the frenzy of capital raising shows no signs of abating.

In recent years, the A-share IPO scene has been plagued with various issues, including the low quality of companies, instances of fraudulent listings, and lax intermediary oversight. The new guidelines raise the entry criteria for the main board and ChiNext (the "Nasdaq-style" second board), demanding higher standards for profit and revenue metrics. This is expected to reduce the number of IPOs significantly.

Moreover, regulators are now placing a strong emphasis on the dividend policies of listed companies. Remember that, Japanese firms have been similarly coerced by regulators into increasing their dividends. The State Council's latest requirements explicitly mandate the disclosure of dividend policies at the time of listing, and even specify the need to enhance the ability to provide stable returns. It is anticipated that companies with substantial cash reserves will gradually increase their shareholder returns.

Stock market system design should focus on protecting small and medium investors

Institutional and retail investors have unequal rights under the trading system, and issues such as quant high-frequency trading have created unequal trading positions and significant impacts. The policy now clearly intensifies the push for systemic reforms to address these loopholes, aiming to achieve a relatively fair trading environment as much as possible, which can greatly boost investors' confidence.

The resolutions at the State Council level profoundly impact the actions of various ministries. Following the issuance of the "Nine Guidelines," the Securities Regulatory Commission and the Shanghai and Shenzhen stock exchanges quickly unveiled several related implementation policies. This swift and decisive action underscores a firm commitment to reform.

For instance, one controversial policy involves adjusting the trading information disclosure mechanism for the Shanghai-Hong Kong Stock Connect. It has shifted from real-time disclosure of buy and sell amounts to disclosures after the market closes. Some international media outlets have portrayed this as a move towards less transparency in China's capital markets—a misleading interpretation. The data is still disclosed, just at a different time.

It is essential to understand that not all media outside China are familiar with the real story. As an investor in this country, I have noticed a significant number of retail investors who closely monitor the "intraday" movements of northbound funds to guide their trades. This strategy has become increasingly common. However, it's crucial to note that "northbound funds" do not exclusively represent foreign capital; a substantial portion also comprises domestic institutional funds operating abroad. The proportion of funds represented in transaction data has been growing, leading to frequent sharp rises and falls in the market. Retail investors, unable to discern the underlying causes, often mistakenly follow these funds, which they perceive as "smart money," thereby being led astray.

Therefore, I commend this policy change. After all, the northbound funds, typically amounting to several billion yuan and at most a few hundred billion yuan, constitute a minor fraction of the A-share market's nearly trillion yuan daily trading volume. It is indeed unnecessary to let such modest capital flow irrationally influence the entire market.

Guiding long-term capital to settle in

The Chinese capital market is notably starved of long-term funds. The predominance of retail investors and the scant proportion of pension fund investments contribute to substantial stock price volatility and frequent chasing highs and selling lows.

The policy directives aim to forge a supportive framework for sustained long-term investment. This includes substantially increasing the proportion of equity funds, promoting the development of index investing, and explicitly enhancing the investment policies of the National Social Security Fund and the basic pension insurance fund. Moreover, the directives encourage the active participation of bank wealth management and trust funds in the capital markets.

The stock market serves as a reservoir for funds; an increase in long-term capital strengthens market confidence. Domestic retail investors often monitor the actions of institutional investors. A lack of participation from major institutions could dampen the remaining market sentiment. Hence, our policies have shifted from addressing the "availability of capital" to ensuring the "presence of long-term funds", hitting directly at the crux of the issue.

Yet, is this enough to spark a new bull market?

Continue reading my analysis on the new 9 Guidelines' impact on the stock market.. You can also get free access by sharing us.