The first quarter of 2025 has been nothing but good news for Chinese tech equities. After years of depressed valuations since 2021, the "DeepSeek moment" has made many realize that Chinese tech companies are, after all, capable of competing in the global AI race.

However, amid the excitement, some recent news may serve as a reality check for the rally that hasn't come easily. Today, I want to walk you through three key developments that matter to Chinese stock investors. While no single headline can dictate the market's direction, each of these stories highlights a crucial takeaway that’s worth paying attention to right now.

The buzzkill: "We are exiting humanoid robot companies in bulk"

Last week, Zhu Xiaohu, managing partner at GSR Ventures, made waves in China’s VC and tech circles with his blunt statement: “We are exiting humanoid robot companies in bulk.” This is a provocative stance, especially given the broader enthusiasm in China’s tech scene—humanoid robots are one of the hottest investment themes right now. (Interested readers can check out my previous post on Where does China stand on the global humanoid value chain?)

Zhu's investment philosophy is simple: he prefers companies with clear commercialization paths. Despite the hype, he doesn’t see one for many humanoid robots projects out there. In an interview with ChinaVenture.com.cn, he explained:

What we fear most is when market consensus becomes overly concentrated and commercialization is unclear. We have never made money on such cases.

While Zhu and GSR Ventures follow a specific investment strategy that isn’t the only formula for success, his comments highlight a key shift in the current narrative of China’s tech investment landscape.

For years, investors have been chasing high-growth, unicorn tech startups with the dream of backing the next big thing. But reality has changed. Even after the recent rally and signs of warming in primary markets, such as a pickup in Hong Kong IPOs, overall VC activity still remains cooler than in the pre-pandemic era. With fewer obvious opportunities, sectors like humanoid robots and AI have drawn massive attention—regardless of whether their commercialization prospects are clear or not.

Now, as the market moves past the initial "DeepSeek moment," it's time to shift focus. The key question is no longer just about AI breakthroughs, but about how applications and downstream products can translate into profitable, AI-powered businesses—or at least show the potential to do so.

After all, too much hope concentrated on a few good projects can create a "bubble."

Xiaomi SU7 car crash

On March 29, 2025, a Xiaomi SU7 electric vehicle was involved in a fatal accident on the Dezhou–Shangrao Expressway in Anhui Province, China, resulting in the deaths of three female university students. The vehicle was operating in Navigate on Autopilot (NOA) mode at approximately 116 km/h when it detected an obstacle and began decelerating. The driver intervened but was unable to prevent the collision with a cement barrier, with the vehicle's speed reducing to 97 km/h at impact.

Following the incident, Xiaomi's stock declined by 5.5%, reaching a six-week low.

But the key takeaway isn’t the crash itself. Xiaomi isn't the only EV maker with crashes—global leaders like Tesla and local players like BYD have not been absent from such tragedies. The real story here is that this crash serves as a "bubble burst" moment for consumers.

Over the past year, Chinese consumers have placed incredible trust in Xiaomi products, believing that anything Xiaomi makes must offer excellent quality and value. For instance, after the sanitary pad scandal angered many, some even joked, "Please let Xiaomi make sanitary pads"—that's how much faith they had in the brand.

However, this car crash might serve as a wake-up call for those who thought Xiaomi’s EVs would easily become its next big growth driver. Making EVs is no easy feat, and even Xiaomi must compete in an already saturated Chinese market (with over 100 EV brands!).

This isn’t to say Xiaomi is doomed, but it’s a reminder that China’s consumer market is fiercely competitive. Even with renewed enthusiasm in stocks, deflationary pressures in the consumer market still exist. No company should be idolized or take the high-growth story for granted too quickly.

In our Discord channel for paying members, I also shared that I closed my Xiaomi position on Monday, which we had been recommending since last year. At 36x+ forward PE, I think the valuation is fair for now, if the EV story doesn't get priced in. That said, Xiaomi is still a solid company to keep on my radar. If there’s a correction, I may consider adding it back to my portfolio.

"China's AI narrative contains cognitive biases"

"China's AI narrative contains cognitive biases", said the Dean of the Beijing General Artificial Intelligence Institute.

A viral article covering the latest opinions of Zhu Chunsong, Dean of the Beijing General Artificial Intelligence Institute, sent shockwaves through the tech investment community with his claim that "China's AI narrative contains cognitive biases."

He argued that many AI innovations in China focus more on algorithms and deployment rather than fundamental cognitive breakthroughs. He also hinted at "superficial hype" surrounding AI, which inflates expectations and fuels speculative bubbles.

For instance, he bluntly stated (and we translated from this article):

"A few years ago, we saw an overuse of the 'nano' concept—nano insoles, nano pressure cookers—now we’re seeing a wave of ‘pseudo-AI’ hype. Some large-model companies even call themselves the ‘Six Little Dragons,’ yet many of them are unprofitable, overvalued, and highly risky."

"Six Little Dragons" refers to six Chinese unicorns in AI/humanoid robots based in Hangzhou. I've written an article about how Hangzhou is becoming China's Silicon Valley because of its "small government" - style management and excellent business environment. If you're interested, read it here.

On the so-called "cognitive biases" in China's AI development, he commented (and we translated):

"Many so-called innovations today are stuck at the fourth level (algorithms) or the fifth level (deployment) and don’t even have a solid theoretical framework, yet they claim to be 'revolutionary.' What we truly lack is original breakthroughs in understanding intelligence itself and cognitive modeling.

We must be clear—DeepSeek has made engineering progress in API commercialization, computing power optimization, and deployment. But these remain engineering achievements; they don’t solve AI’s core challenges—such as cognitive modeling, intelligence theory, and learning mechanisms.

Take U.S. innovation as an example: many breakthroughs happen at the deepest levels—hardware (chips, architectures), foundational models, and algorithm optimization. If we want to compete with the U.S. in AI, the key lies beyond the fourth layer—it requires deeper philosophical and theoretical innovation. If we simply follow the U.S. playbook of scaling compute, algorithms, and deployment, we’ll always be playing catch-up."

Of course, not leading in state-of-the-art foundational research doesn’t necessarily block commercial success. And while this isn’t a dot-com-style bubble, it’s yet another voice warning that parts of China’s tech sector may be overheating.

Now is the time to stay clear-headed and focus on AI’s real development—not just foundational research but also the monetization potential of AI companies. And on both fronts, behind all the hyped headlines, we have to admit that Chinese AI companies still have gaps to fill.

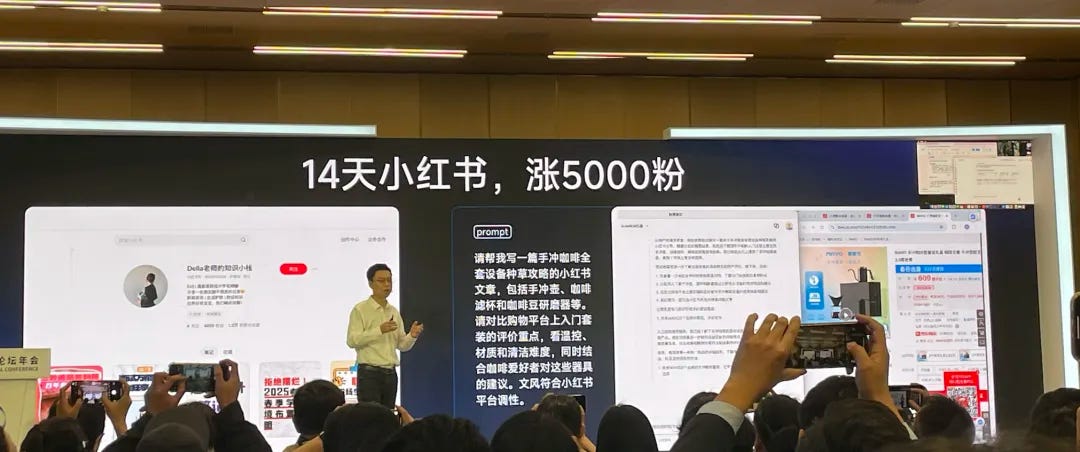

Recently, Zhipu AI—one of China’s three AI LLM unicorns valued at over 20 billion CNY—launched its AI agent, AutoGLM. A key highlight of the launch is that AutoGLM is free for everyone, with no invitation code required—directly addressing the frustration of securing an invite for Manus AI, the first-ever general-purpose AI agent that made headlines just a month ago, not to mention its newly introduced hefty monthly subscription fee.

One of Zhipu’s use cases claims that AutoGLM can browse the internet and complete tasks like a human intern. They even demonstrated running a Red Note account with AutoGLM, gaining 5,000 followers in just two weeks and securing an order—this is one of the most obvious commercialization paths for AI tools in China.

That said, many netizens who tested AutoGLM reported that the experience isn’t as smooth as advertised, and the product is still in its early stages. But this underscores how Chinese AI startups are racing to deliver real commercial value, and the competition is fierce. With multiple LLM players in the market, some could end up burning through billions and still losing the race. While it’s an exciting narrative for investors, it’s still too early to predict the timeline for China’s AI agents and applications to become viable businesses—or how the competitive landscape will unfold.

From an investment perspective, I think the current rally may have already priced in much of the value correction triggered by DeepSeek’s launch. As I mentioned in my latest YouTube video of the Chinese investment roundup, a lot of the current hype and bullish sentiment stem from FOMO over Chinese tech giants’ position in the global AI race or expectations around Alibaba and Tencent’s increasing AI-related capex. But looking ahead, with many Chinese tech giants now trading at or above their 10-year average PEs, the next leg up will likely come from downstream products and services that are actually profitable or have strong commercial potential to justify further upside—especially as the recent correction in U.S. stocks is expected to create headwinds for global markets. (The same applies to U.S. tech stocks too.)

In our Discord channel for paid members, I also shared on March 24 that I took profits from my Hang Seng Tech positions based on this rationale. Overall, I’m bullish on Chinese tech stocks in the long run, and I see a lot of potential—but I’m not chasing new highs at this moment.

Closing thoughts

At Baiguan, we strive to provide objective and actionable insights for investors and business owners with a stake in China. Over the past month, we’ve repeatedly pointed out the bumpy road ahead for Hong Kong and China ADRs, advising against chasing new highs in tech and suggesting alternative opportunities, such as consumer stocks. Our latest call remains the same: stay sober, watch out for short-term headwinds, and consider taking profits.

The rationale is simple—after a sentiment-driven rally, China needs to show real, sustained macro improvements, like a stabilized real estate sector and a stronger recovery in domestic consumption. So far, despite the stock market rebound, these fundamentals haven’t materially changed.

To stay updated on these macro shifts, I recommend following our "Charts of the Week" series, where we provide biweekly updates on key economic indicators such as real estate and consumption. I also break them down into 8-minute video roundups on our YouTube channel.

For more timely discussions, consider joining our private Discord channel for paid readers. There, I share trade ideas—both the ones I like and the ones I’m avoiding—through the lens of a global asset allocator. To enhance your decision-making, we also provide a daily digest of equity research from top sell-side institutions, covering macro trends and specific company analysis. Each day of digests includes a 3-minute audio summary to make it easy to absorb key insights quickly.

If you want in-depth and timely equity research papers, and to join our paid community to exchange ideas on China's investment and general affairs, consider getting a paid membership today!