China's 2023 Luxury Consumption in 5 Keywords

A K-shaped path towards recovery

In 2022, overall luxury spending in China decreased by 10%, interrupting the strong growth seen in the previous five years (Bain&Company). However, with the lifting of COVID restrictions in China, the luxury industry has every reason to believe in a strong rebound of luxury consumption.

Although the paths to recovery for different consumption categories vary, luxury giants have confirmed their confidence in China's growth potential in 2023.

LVMH, the industry giant, had an excellent start to the year in 2023. Sales in Asia, excluding Japan, grew by 14% in 2023Q1, compared with an 8% decline in the fourth quarter of last year. The group expects China to drive growth in 2023 [Reuters]. Bernard Arnault, the Chairman and CEO of LVMH, recently met with China's Minister of Commerce, Wang Wentao, reaffirming the luxury giant's confidence and ambition to expand in China.

To gain insight into how luxury consumption will unfold in China in 2023, we scanned millions of discussions on Chinese social media, as well as commentaries and articles published by industry experts. Here are the important nuances and trends we have identified.

Keyword 1: VIC (Very Important Customer)

Luxury giants are once again raising their prices to prioritize VIC customers, who are high net worth individuals with significant purchasing power and drive a significant portion of a luxury brand's revenue.

In March, the price of Chanel's iconic handbag products in the Chinese market increased by approximately 11%-16%, while the US market saw an increase of 7%-18%. After the price increase, the price of CF series products was 74% higher than in November 2019.

Other brands, such as Celine, Fendi, Bottega Veneta, Gucci, and Saint Laurent, have all adjusted their prices to varying degrees since 2019, with the highest price increases being applied to their classic items. [source]

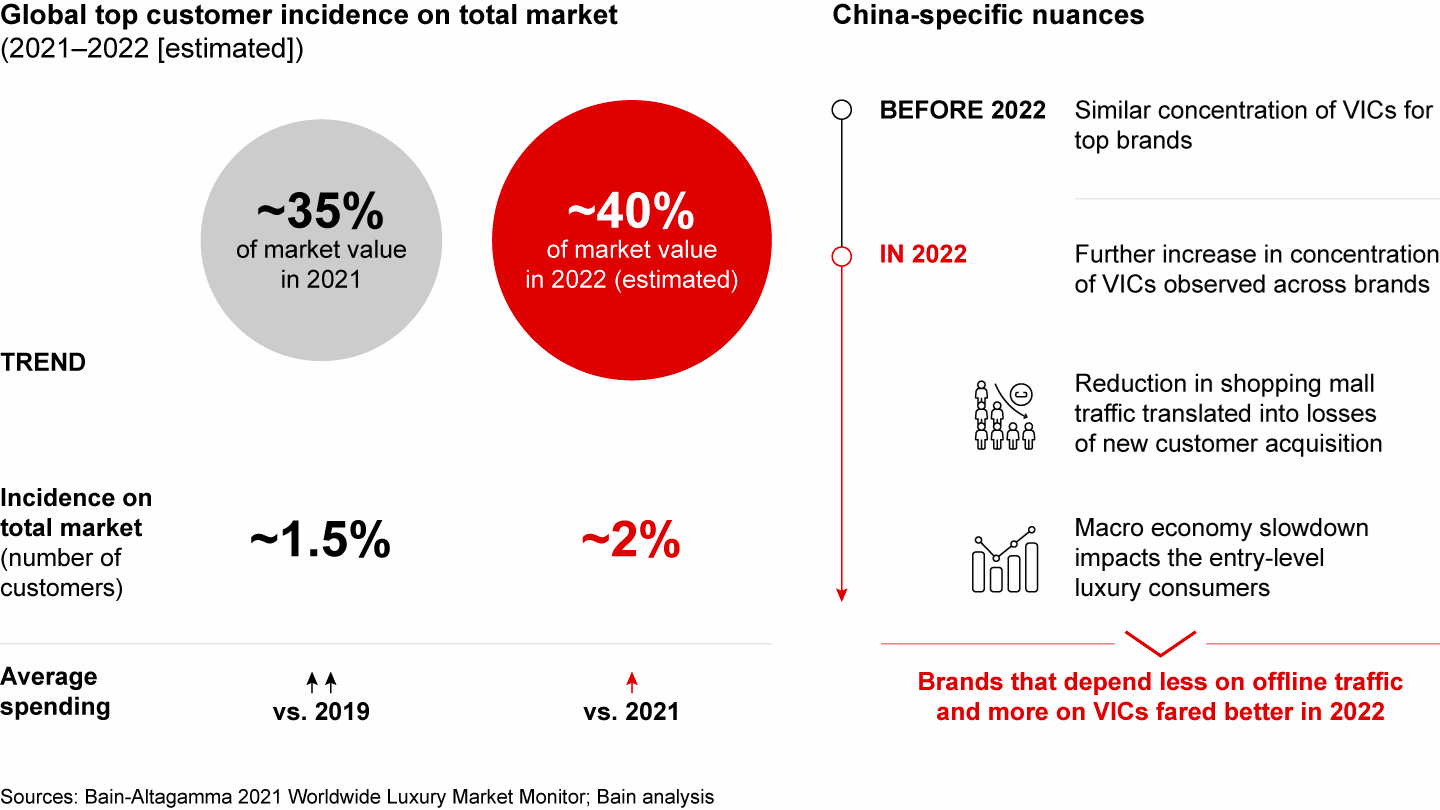

The VIC customers are highly concentrated in China's luxury market and this concentration increased further in 2022. According to Bain & Company’s research:

Compared to high net worth individuals, entry-level luxury consumers are more affected by the economic slowdown. In 2022, epidemic prevention and control measures resulted in a decrease in mall traffic, which led to sales being more concentrated among VIC customers. The average concentration of VIC customer sales in the global market reached 40%, and the concentration of VIC customer sales for some luxury brands in the Chinese market exceeded this level.

VIC customers are also the main force for purchasing luxury goods online. Take Tmall's leading luxury brand as an example, customers who consume more than three times a year contribute to more than 50% of sales and are the fastest-growing consumer group

An article by an independent think tank in China sheds further light on the luxury giants' strategies to prioritize VIC customers:

In 2019, the group of individuals in China with a personal net worth of over 10 million [~1.4 million USD] yuan accounted for only 0.3% of the country's population but contributed to 73% of luxury consumption. After three years of the pandemic, this number has grown to 82%.

Luxury giants are raising prices in order to cater only to the true high-net-worth group, at the expense of middle-class consumers.

LVMH group is targeting the top 0.3% wealthiest population in China:

In the past, smart luxury groups did business with two types of people: one was the urban middle class who saved money to buy LV; the other was the top wealthy who bought bags like groceries.

In a widely circulated meeting summary from April of last year, LVMH group set a stringent threshold for its core high-net-worth individuals: personal annual income of over 3 million yuan or household annual income of over 10 million yuan

The strategy of prioritizing VIC customers has proven to be effective in the past and is recession-proof. We think that premium pricing, targeting the true high-net-worth group in China, will be a core strategy for luxury giants to expand and boost overall sales in 2023.

Keyword 2: Revival of Offline Shopping

Duty-free shopping is popular for buying "entry-level" luxury items and has been targeting middle-class consumers in China. The so-called "entry-level" luxury items, which include brand-name products of high quality but are relatively more affordable and accessible to middle-class consumers, are widely sold through duty-free shopping channels. However, the duty-free shopping industry was heavily impacted by the COVID-19 pandemic.

With the reopening of in-person shopping, we expect duty-free shopping to boost luxury sales, particularly among middle-class consumers who are in the market for "entry-level" luxury items.

According to statistics from Haikou Customs, the tax-free shopping amount on Hainan Island during this year's Labor Day holiday (from April 29 to May 3) reached CNY 883 million. This represents a 120% year-on-year increase from 2022.

Hainan is now a major hub for duty-free shopping among China's middle class. It has become more attractive than Hong Kong because it offers the same duty-free benefits without requiring a visa.

According to Liu Xiaoming, the Acting Governor of Hainan Province, total sales in Hainan duty-free shops reached 20.3 billion CNY in Q1 of 2023, marking a 29% year-on-year increase. Shen Danyang, Executive Vice Governor of Hainan, said that the annual sales of tax-free shopping exceeded 60 billion CNY in 2021 and is expected to exceed 80 billion CNY this year. [source]

Hainan may not be a desirable shopping destination for ultra-high-net-worth groups, as the shopping experience can involve lots of waiting in line. However, the resurgence of offline shopping scenes will certainly boost the spending of middle-class families on luxury items.

Keyword 3: Cosmetics still under pressure

Cosmetics are still under pressure, while leather goods, jewelry and skin-care are rebounding.