How to understand Chinese real estate optimization policies on May 17th?

Interpretation of the policy, potential future policy focal points, public sentiment and market performance

This year, China's real estate market has witnessed a flurry of policy adjustments aimed at stabilizing the real estate market and fostering healthy development.

On May 17th, the market responded enthusiastically to the so-called "epic favorable" policies, leading to a robust surge in the real estate sector, which in turn propelled the Shanghai Composite Index to rebound from its lows, breaking through the 3,150-point mark and effectively improving market sentiment. Leading real estate enterprises such as Vanke A (000002.SH), Poly Developments (600048.SH), Tande Source (600665.SH), Binjiang Group (002244.SZ), and Rongsheng Development (002146.SZ) saw their stock prices soar collectively, with related sectors of the real estate industry chain, including real estate development, real estate services, characteristic towns, property management, building materials, and architectural decoration, all showing strong performance.

The article translated today, authored by economists Duandong Gao and Jiawen Wang of Everbright Securities, provides an in-depth analysis of the real estate policies unveiled on May 17th. It examines the projected outcomes and offers insights into forthcoming policies and their anticipated direction. Furthermore, by synthesizing real estate market data on views and transactions with social media sentiment analysis from BigOne, we aim to evaluate the efficacy of the newly implemented policies comprehensively.

Multifaceted real estate policy suite activates: beyond simple adjustments

The major highlight of the new comprehensive inventory reduction policies is its formation of a multifaceted policy package. The statements made at the Politburo meeting signify a shift from localized policies to a nationwide campaign to reduce housing inventory. During the recent real estate policy briefing on 17 May, coordinated efforts among various government ministries resulted in a set of specific measures, collectively forming a robust policy package.

(1) Relaxation of demand-side restrictions: Nationwide adjustments have been made to the minimum down payment ratios for first and second homes, reducing them to 15% and 25%, respectively. Additionally, the interest rate on housing provident fund loans has been lowered by 0.25%, with the new minimum rates set at 2.775% for loans of five years or less (including five years) and 3.325% for loans exceeding five years. The floor on commercial loan interest rates for first and second homes has been removed at the national level.

[Baiguan Note: Here's a timeline of significant adjustments to the minimum down payment ratios for first and second homes in China:

1998: Housing reforms initiated, with a 30% down payment for personal housing loans.

2003: "Notice No. 121" set 20% for first homes and higher for subsequent homes.

2006-2008: Tightened policies with 30% for first homes and 40% for second homes.

2008 October-2009: Relaxed policies post-global financial crisis, with a 20% minimum.

2010-2014: Further tightening to 30% for first homes over 90 sqm and 50% for second homes.

Since 2014: Policies adjusted to support the market, with improved terms for settled previous loans.

August 2023: Unified minimum down payments to 20% for first and 30% for second homes.

May 17, 2024: Latest adjustment to 15% for first and 25% for second homes.]

(2) Local government-led land reserves on the supply side: The policy also proposes that in cities with high inventories of commercial housing, local governments can purchase unsold homes at reasonable prices for use as affordable public housing. This is part of a continued effort to address the risks associated with unfinished residential projects and to prioritize the reduction of existing commercial housing stock. To further support these initiatives, a 300 billion CNY(≈42.25 billion USD) re-lending facility for affordable housing has been established. This aims to encourage financial institutions to support local state-owned enterprises in purchasing completed but unsold commercial properties at reasonable prices for affordable housing purposes. This measure is expected to stimulate an additional 500 billion CNY (≈70.42 billion USD) in bank loans.

(3) Mitigation of risks for industry-related entities: Based on extensive research, the government is also preparing to introduce policies for the proper management of idle land and the revitalization of existing land resources. Local governments will be supported in taking appropriate actions, such as reclaiming or acquiring idle residential land that has already been sold, to alleviate the financial difficulties faced by enterprises.

Looking ahead: what other policies can we expect?

Looking at the specifics, there is room for further policy enhancements in the future.

Firstly, the current inventory reduction pressure is relatively higher. As of April 2024, the area of residential commercial housing for sale was nearly 391 million m², slightly below the previous peak of 466 million m². However, due to a sharp decline in sales volume, the inventory clearance cycle has been prolonged. The previous inventory peak occurred in February 2016, with an inventory clearance cycle of approximately 21.6 months. As of March 2024, the current inventory clearance cycle has risen to 22.4 months. Additionally, household debt leverage is higher. In 2016, the average quarterly household leverage ratio was 42.7%. By the end of Q1 2024, it had climbed to 64%, an increase of 21.3%. This indicates that there is less room for households to increase leverage compared to the 2016 cycle, necessitating stronger policy support.

Secondly, many local governments have already implemented relevant policies in practice. The nationwide removal of the minimum down payment ratio and loan interest rate floor is inherently flexible. On September 29, 2022, the People's Bank of China and the China Banking and Insurance Regulatory Commission issued a notice to temporarily adjust differentiated housing credit policies. Eligible city governments were allowed to independently decide whether to maintain, lower, or remove the floor on new first-home loan interest rates before the end of 2022. Many cities have already reduced mortgage rates to a certain number of points below the Loan Prime Rate (LPR).

Therefore, the market's ongoing and robust performance hinges on the anticipated scope for further policy enhancements and the effectiveness of policy implementation. Specifically, there are three focal points:

Focus point one: how to utilize re-lending for affordable housing?

The re-lending facility for affordable housing, introduced by the People's Bank of China, operates through a mechanism where the central bank provides funds to commercial banks, which in turn provide sufficient eligible collateral. Subsequently, commercial banks extend a certain amount of funds to local state-owned enterprises (SOEs). These SOEs then purchase unsold, completed commercial properties from the market, converting them into affordable public housing, which can be either for sale or for rent, with the latter generating revenue from subsequent operations.

Estimate capital requirements: Drawing from the previous inventory reduction experience, during the last cycle, the peak inventory of commercial residential properties was 739.31 million m² in February 2016, which was reduced to a low of 492.21 million m² by November 2019, representing a clearance rate of approximately 33%. Applying this rate to the current inventory, as of the end of April 2024, there were 390.88 million m² of residential properties for sale, necessitating a reduction of 128.99 million m². Given the current average price of residential properties in 100 sample cities is around 16,000 CNY (≈2,253.52 USD) per square meter, approximately 2 trillion CNY (≈281.69 billion USD) would be required. Assuming a 30% discount on the purchase price, the required funding would be around 1.4 trillion CNY(≈197.18 billion USD).

Now the funding arrangement consists of 300 billion CNY (≈42.25 billion USD) from re-lending and an additional 500 billion CNY (≈70.42 billion USD) in leveraged credit funds, totaling 800 billion CNY(≈112.68 billion USD). Under a conservative scenario, if substantial purchase discounts, such as the 30% assumed above, are applied and funds are used strictly to mitigate inventory pressures in a limited sense, the announced funding appears adequate but not sufficient. Typically, policies are implemented from the top down and require feedback from initial data to adjust and enhance measures. Therefore, it is likely that the first batch of funds will be evaluated before further enhancements are made, indicating that increased efforts can be anticipated.

Focus point two: effectiveness of policy implementation by local goverment

The primary executors of these policies are local governments, with the core issue being the difference between potential returns and the cost of funds. Drawing from the 2008 experience in the United States, where the Treasury took over Fannie Mae (FNMA)and Freddie Mac (FHLMC) nationwide, the current policy places responsibility on local governments, which introduces variability in execution and effectiveness across regions.

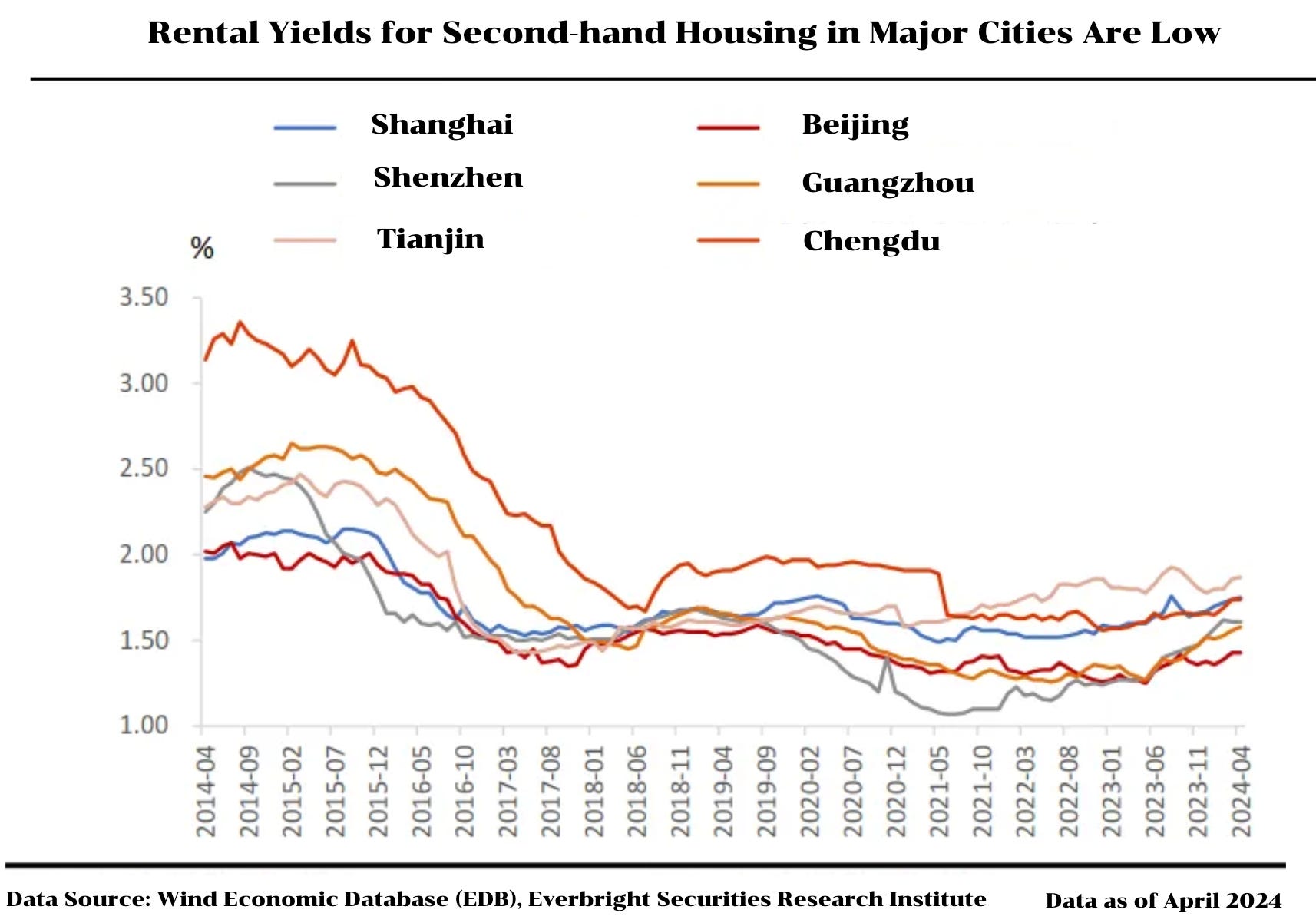

Local governments’ willingness to implement these policies hinges on two factors: whether the funds can revitalize existing assets and alleviate debt pressures, and whether the potential returns from managing these projects exceed borrowing costs. The key equation is: potential returns from acquisition > borrowing costs, i.e., (rental yield + appreciation potential - operating costs) > borrowing costs. Given that operating costs are relatively stable and appreciation potential is not a primary focus early on, the main variables are rental yields and borrowing costs.

Currently, rental yields in major and popular cities are relatively low. As of April 2024, the rental yields for second-hand housing in Shanghai, Beijing, Shenzhen, Guangzhou, Tianjin, and Chengdu range between 1.43% and 1.75%, with an average of 1.66%. However, this does not account for the potential "discount" from bulk purchasing. Assuming a 30% discount, the rental yield could increase to approximately 2.37%. After deducting operating costs and considering the typically low interest rates of policy-driven re-lending tools, which often include fiscal subsidies, there is still potential for profit. This can incentivize local governments to act.

Focus point three: another meaning in "supply-side" inventory reduction

On April 29, 2024, the Ministry of Natural Resources issued a notice on residential land supply, requiring cities with an inventory clearance cycle exceeding 36 months to suspend new residential land supply. For cities with a clearance cycle between 18 and 36 months, the new land supply will be dynamically determined based on the area of existing residential land activated within the year.

Data indicates that in cities with significant residential inventory pressure, real estate companies' participation in local land auctions has already decreased. In cities with inventory clearance cycles over 36 months, there were about 29 land transactions in 2023, while cities with cycles under 36 months saw about 56 transactions, nearly double.

Although local governments' "land banking" efforts appear to target demand, they are essentially a supply-side policy aimed at reducing housing supply in the market to ease supply-demand imbalances. Strengthening supply-side reforms in land policies could enhance the effectiveness of these measures. An optimal policy mix would involve further reducing local land supply while supplementing local fiscal revenue through special bonds, additional national debt, transfer payments, and fiscal and tax reforms. This approach aims to resolve existing debt while supporting local economic development.

Insights from Baiguan's exclusive data: how did the market react in the first week following the policy announcement?

In the following analysis, we will leverage transaction data (incl. GTV, transaction volume and area, average selling price; covering 140+ cities in China) from a Chinese leading real estate transaction platform, tracked by BigOne Lab, as well as forward-looking property viewing data (covering 80+ cities) to assess the impact of the newly implemented housing policies in the first week. Additionally, we will monitor the national real estate-related discussions on major social media platforms to gauge the intensity and structural changes in the discourse.