The secret: sell Chinese VICs expensive but useless stuff

China's slumping luxury sales is not just a consumption downgrade

As I was taking a walk to my office the other day, I couldn't help but notice that my favorite imported goods supermarket downstairs, which went bankrupt earlier this year and has been vacant since, was finally replaced with a vintage luxury store. Similarly, another store, which used to be a real estate agency, has now become a second-hand luxury handbag store. Taking into account two other vintage stores that have been around for more than two years, my apartment complex, with just over 1,800 apartments, already has 4 second-hand luxury stores nearby.

My apartment complex, which is located close to Beijing's CBD Guomao, is just a microcosm of the booming second-hand luxury market in China.

Sales of major luxury brands in China are practically bleeding in 2024. LVMH Group reported a 3% global decline in Q3, with sales in Asia (excluding Japan, where the Chinese market holds a dominant share) sliding by 15%—a sharper drop compared to the 14% decline in the previous quarter. The bleeding performance of the industry giant LVMH has significantly shaken confidence in the luxury sector in China, raising concerns for other players in the market, some of whom are in an even worse position. (We shared our data to capture this trend earlier this year.)

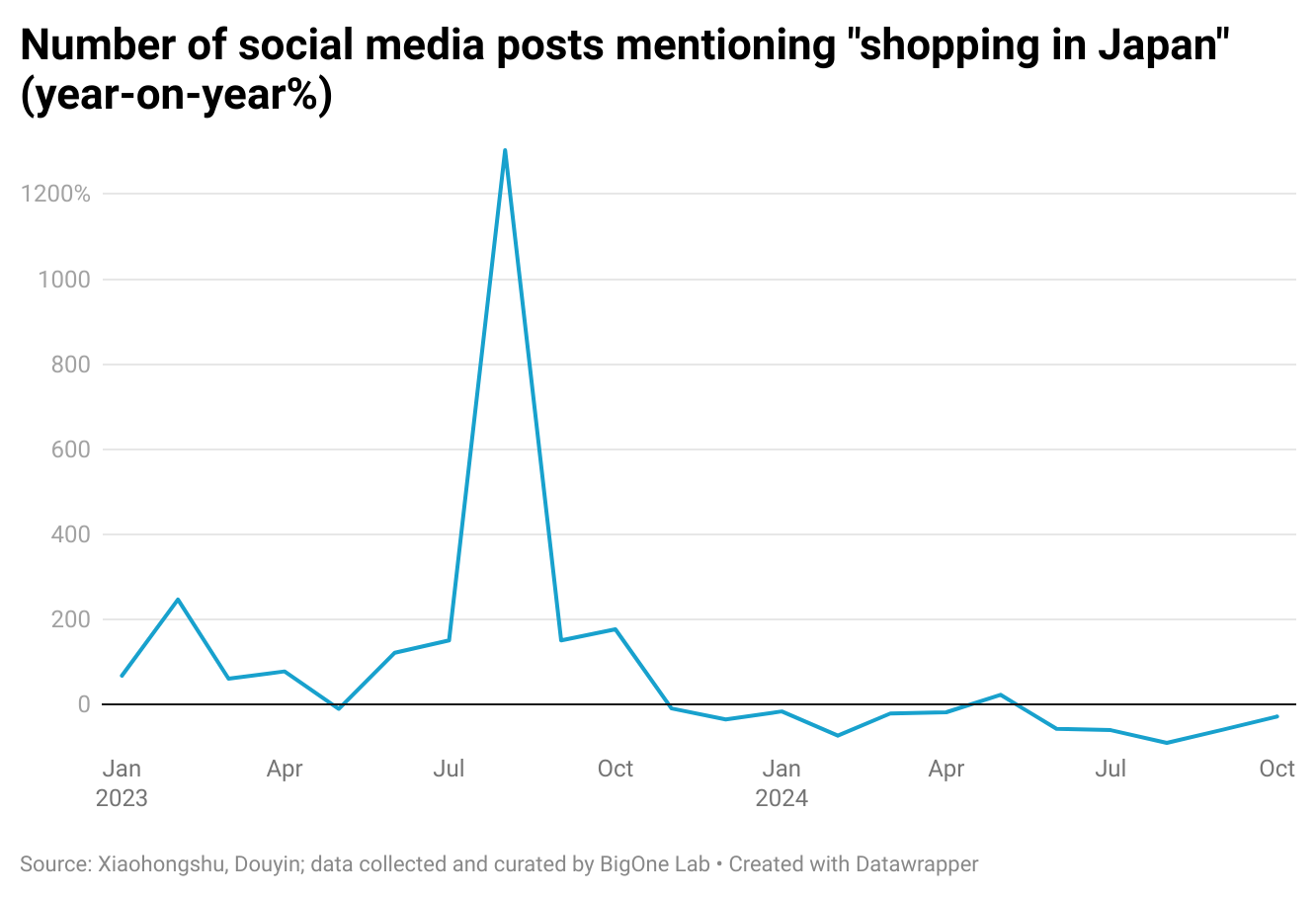

One possible explanation for why Chinese consumers' interest in luxury purchases did not decline is that they were simply driven to Japan because of the price disparities caused by the depreciating JPY. While this was indeed the case for 2023 and the first half of 2024, I noticed that discussions around topics like 'flying to Japan to shop' noticeably decreased since the second half of 2024. This suggests that consumer appetite for luxury brands could only worsen in the year to come. Securing VIC clients, those who are still capable of spending, has become the top 1 priority for the brands.

I chatted with a sales rep at one of the second-hand luxury stores downstairs in my apartment complex. She told me that her base salary is around 9,000 RMB, but with the handsome sales commission, she now earns a steady monthly income in the range of 20,000 to 30,000 RMB, and in good months, it can even exceed that. She did not see signs of decline, even amid the broadly stagnated salary growth in China in 2024. (As a reference, 20,000 to 30,000 RMB is what a young Chinese professional with 3-5 years of experience would earn in industries like IT or finance, and you have to be among the best to reach that level.)

This just gives you an idea of how the second-hand luxury market is booming in China, albeit unintuitively, given the broader decline in the luxury sector.

In today's newsletter, I want to share some perspectives on this trend, beyond the 'consumption downgrade' narrative, which I think oversimplifies some important shifts in Chinese consumer psychology.

Second-hand luxury: Is the 'grey market' really the reason behind the declining sales?

While it is easy to blame the second-hand market amid "consumption downgrade", and I certainly believe it is a factor, I do not think it alone attribute to the decline of sales. A healthy and robust price in the secondary market can actually enhance the brand reputation.

On Chinese social media platforms like Douyin and Xiaohongshu, the percentage of posts discussing 'second-hand purchases' for major luxury brands has noticeably declined since Q3 of 2024. However, Hermes has experienced a slower decline compared to its peers. And it comes as no surprise that Hermes was among the only luxury brands that still managed to grow in sales in mainland China in 2024, as our team observed previously. As the 'consumption downgrade' mindset takes hold, the second-hand market has also been affected, with consumers increasingly drawn to brands that truly retain value. Amid uncertain times, buying luxury items for many now carries an additional purpose – as an investment that retains value, rather than simply for personal pleasure or a fashion statement.

However, this is a widely discussed narrative, and the entire picture extends beyond that.

Apart from the value-retention consideration, shopping vintage or second-hand has actually become a trendy activity for a small but capable consumer community. For these consumers, shopping vintage doesn’t mean they want to get bargain deals, but rather make a fashion statement and hunt for rare vintage pieces, even if it means paying a premium for them.

Located in a weathly neighborhood in Beijing's Shunyi district, a vintage clothing studio called 'Utopia the Shelter' is one such example. With a classy, old-fashioned interior design reminiscent of the 80s, the store occupies a two-floor deserted warehouse and features many vintage clothing items, bags, and accessories from the 80s and 90s. The store carries discontinued styles from brands such as Ralph Lauren, Chanel, and Comme des Garçons, as well as many lesser-known brands among Chinese consumers from all over the world. Each piece can easily cost between 8,000 RMB (~1111USD) and beyond, but the store has always had a bustling atmosphere, with consumers eager for one-of-a-kind rare vintage pieces. Almost none of the items in this shop display obvious big brand logos, and you rarely see the typical "value-retaining" bags or clothing lines.

Consumers also discuss traveling to Japan to 'shop vintage' on social media, with many key opinion leaders sharing their favorite vintage studios in Japan. Unlike China, where most so-called vintage stores mainly specialize in bargain deals on widely circulated handbags and jewelry styles in the second-hand market, Japan has many vintage studios that focus on rare pieces with a special story behind them, which adds to their value as collectibles.

This group of consumers largely overlaps with the VIC (Very Important Customer) group that top luxury brands wish to target. While almost all top-tier brands realize that their 2024 strategy is to secure these VIC customers, many fail to identify them. Brands still pursue the go-to strategy of increasing prices as a way to create exclusivity, believing this is what VIC consumers want. However, many neglect the shift in consumer psychology: among true VIC consumers in China, price isn't the ultimate factor for exclusivity. In this environment, consumers still shop for personalized styles, a story behind the item, or a clear statement of their values through their purchases, and they don’t care much about the brand logo, because it says nothing more than 'I have a lot of money.'

Where are all the VIC clients? Miu miu's epic success in 2024

Miu miu emerged as the dark horse amid bleak luxury sales in China. The success of the Prada group's Miu Miu is an excellent example to illustrate the shift in consumer psychology behind China's VIC clients.

Although Prada's sales grew only 2% in Q3, Miu Miu exploded by 105% in the same quarter, continuing the growth of 93% in Q2. In China, Miu Miu has become the only luxury brand to achieve such remarkable growth in 2024.

The true VICs in China have shifted away from using the price as a criteria for exclusivity. Instead, the main factor influencing their purchase decisions is "who else." "Who else wears this brand? Who else wears this bag?" This question largely determines the impression and personality they associate with a particular brand.

A quick check of social media in China reveals very different scenarios for this question. For instance, when searching "who wears Louis Vuitton" (picture on the left), most topics are about "why people wear LV bags yet still take the subway". In contrast, when searching for Miu Miu (picture on the right), you'll see topics such as "True princesses wear Miu Miu," "Miu Miu is the Uniqlo for rich daughters," and Quan Hongchan, the 17-year-old Olympic champion and diving prodigy, wearing a Miu Miu bag.

Gen Z and millennial consumers are among the driving forces behind China’s luxury sector spending. According to Jing Daily, they now account for approximately 60% of luxury spending in China in 2024, making China the youngest of the major luxury markets, with an average luxury consumer age of 29.

In China, Miu Miu’s choice of brand ambassadors is key. It could be the 22-year-old actress Zhao Jinmai, popular among young Chinese born in the 2000s, or the 70-year-old "doctor auntie" Tan, who walked for Miu Miu at Paris Fashion Week. It could even be worn by trending male celebrities, despite Miu Miu not having a men's fashion line.

Miu Miu's online presence has cultivated an image that resonates deeply with young consumers: audacious, rejuvenating energy, and the daring to be one's true self—regardless of age or identity.

So, if I were a young urban Chinese VIC, would I choose a Louis Vuitton bag or a Miu Miu one? The answer is obvious.

Expensive, bold, but useless: The secret to winning VICs

It has become easy to blame the "consumption downgrade," and therefore, it is intuitive to create a good "price-for-value" proposition when brands try to attract consumers.

While "price-for-value" is indeed a true need for many, I don’t believe it’s a priority for the true VIC clients in China. In fact, emphasizing it in the product image can actually have the opposite effect.