Important announcement: We are hosting the second “Ask Me Anything” live session this Wednesday, July 31 @ 9 PM Hong Kong (9 AM New York). This is going to be a 1-hour live webinar for you to ask the team about how we, as entrepreneurs, look at the 3rd Plenum, as well as any other questions you have, without limitations.

The event is reserved for paid subscribers, but for a limited time, we are offering 5 free spots. Reply to this newsletter today if you are interested in joining, and we will email the Zoom link to the event to the first five free subscribers who reply!Last week, we shared with you our practical take on the recently concluded 3rd Plenum. In summary, contrary to many other voices, we believe the 3rd Plenum has hit all the right buttons, and if implemented properly, would have far-reaching positive effects on the Chinese economy.

But despite our optimism, we will not deny that the market reactions to the Plenum have been at best muted, and have been quite bad in some corners. For instance, the onshore Shanghai Composite Index has broken below key psychological threshold of 2900 again after the Plenum. Although, we think judging the effect of a highly consequential political event by stock market price is as self-referential as judging a stock's intrinsic value based on its stock price, we still believe analyzing this negative market reaction is important.

Today we will share with you an insightful article by our old friend, Bob Chen. Bob is a UChicago-educated economist-turned-VC investor. He previously appeared on our podcast talking about investing in China's "Go-Global" opportunities. We also previously translated a very popular article from him about how the rest of the world might benefit from the US-China decoupling.

In today's article, originally posted by Bob on his personal WeChat blog, directly addresses why the public reaction is so bad, and despite the negativity, what he believes the bright spots are.

The original title is "市场尚未买账-当既要和又要打架时 The market hasn't bought in yet - when multiple goals fight with each other"

Summary

Why did the market decline after the 3rd plenum?

There are many bright spots about the Decision, but there is yet lack of prioritization and clear communication

Increasing difficulty in balancing multiple goals

The public believes the implementation will occur where there is the least resistance, hence the retirement age rumors

The market is trading as if there is no tomorrow

Several positive strategic opportunities for China

The market seemed unimpressed after the 3rd Plenum, with fund flows continuing to withdraw from the market orderly. Is it simply because expectations weren't met? Even if there were no surprising results from the Plenum, why did the market react so strongly?

Why did the rumor about delaying retirement for the post-90s generation first become viral after the Plenum? The Wechat account that first published this interpretation quietly went offline, and the official sources did not make significant efforts to refute it. Surprisingly, Tencent News even posted an interpretation of delayed retirement, beginning with "finally implemented" (though it wasn't). Today, most people still firmly believe that a delayed retirement plan has been implemented.

The core issue seems to lie in the way the Plenum results were communicated. The Plenum contained numerous highlights, but due to their scattered nature, it was hard to see the bigger picture. The public found it difficult to understand and eventually lost interest.

Behind these numerous objectives, there is still a lack of detailed plans and strategies for implementation. While the highest-level decisions may not need to address every detail, people are bound to ask how these decisions will be implemented because:

Externally, there is increasing pressure, while internally, issues like the decline in real estate, accumulation of local debts, weak domestic demand, and overcapacity in various sectors reduce incremental opportunities. The era where a high-level policy could easily mobilize public enthusiasm and create new opportunities is over. People are eagerly eyeing on the only entity with resources and influence to provide actionable plans and strategies.

Even if achieving these goals isn't immediately feasible, people want to see a clear set of priorities. In an era of limited resources and a focus on major projects, seeing priorities and breakthroughs helps find the main thread amidst the detailed plans. When there is no prioritization or emphasis, it becomes a long-winded maze of words.

The only clear priority seems to be on safety, autonomy, and overall coordination, a continuation of a control-focused approach. This makes it hard for the market to remain enthusiastic. The market appears overly compliant, with funds flowing heavily into state-owned enterprises and government bonds to support construction, behaving defensively rather than proactively.

If the numerous and scattered highlights are at odds with the current trend of short videos and concise posts on Weibo, we hope that brokerage firms, think tanks, and independent media will provide insightful analyses.

However, interpretations tend to either cover all aspects extensively, continuing the scattershot approach, or focus on individual highlights they find appealing. This scattershot approach still doesn't address the core question of which of the many points of light is the "sun".

What is even harder to balance is the internal divisions and even opposition—there are growing conflicts between trying to "have it both ways".

In an era of growth led by existing resources, the slowing growth of the "overall cake" (wealth) inevitably leads to more conflicts. Since the pandemic, there has been a clear division in interests among different groups. This includes the split between the elderly, the middle-aged, and the young (pensions vs wages, mobility vs lockdowns), between first-tier and third- and fourth-tier cities (financial services vs manufacturing), between technology and employment (technological progress vs job preservation), and between public finance and private savings (whether debt should be borne by the government or households). There are also conflicts between boosting domestic demand and fully supporting production, between stimulus measures and discouraging idleness, and even in debates over international issues like Russia-Ukraine and Israel-Palestine. The difficulty of trying to balance all these demands is increasing.

Perhaps the notion of serving the public good requires decisions to be comprehensive and inclusive, making it difficult to clarify a specific stance. As a result, we will have to wait and see how these decisions are implemented.

This internal division also explains why the rumor about delayed retirement quickly gained traction. Most people believed it at first glance, but those familiar with the policy-making process knew that such a significant matter affecting millions couldn't be decided so hastily. However, it’s clear that when it comes to implementation, people believe that the path of least resistance is most likely to be taken.

If reforms in state-owned enterprises, respect for the market, and the promotion of technological development require talent, overcoming resistance, and changing entrenched interests and mindsets, the process will inevitably be lengthy. Meanwhile, asking the dispersed, controllable, and less influential public to contribute more [Baiguan: implying policies such as delayed retirement] seems a natural choice.

Strikingly, many people have resorted to humor rather than serious thought. A considerable number of young people seem to disregard the future, almost resigned to the idea that any pension they receive will be insufficient. Indeed, in terms of the demographic structure, by the time those born in the 1990s retire, without the support of inherited wealth, securing a pension sufficient to sustain a comfortable life would necessitate raising the retirement age well beyond 65, potentially to over 70.

With the future appearing bleak, many choose not to think about it. The age of 65 seems distant and irrelevant.

This mindset mirrors current market behavior. Investors are heavily buying 30-year government bonds, despite yields indicating minimal economic growth prospects. It’s as if the future doesn’t matter (coincidentally, many people will retire in 30 years, losing touch with the concept of a future beyond that timeframe). Similarly, investors are chasing dividend stocks, driving their yields to near fixed deposit rates, as if growth stocks have suddenly lost their potential.

This is typical market behavior when people see no vision for the future.

Paradoxically, while emphasizing patient capital and long-term strategies, most market participants are trading as if only today matters.

This also brings up another issue with the decision.

Implementation of policies requires people. Currently, morale across many industries is at a low point. The service sector has been hard-hit, and many in the venture capital community have been leaving, with many involved in lawsuits and buybacks, affecting numerous entrepreneurs and companies, which are vital for innovation.

Secondary market financial professionals are also "lying flat", merely aiming to do the minimum, directly impacting market sentiment. Even many employees in state-owned enterprises and local administrations, under strict audits and accountability, are attempting to maintain a low profile, emphasizing stability. This societal atmosphere starkly contrasts with the high-profile, ambitious policies being promoted.

Lastly but crucially, the impact of policies on the market is no longer immediate. Marking the anniversary of the active capital market policy, it has become evident that policy alone is not a panacea. It requires the cooperation of the market and the public, necessitating unity. Even if the authorities have identified existing issues, merely pointing them out and setting goals is insufficient. Clear prioritization, measures, resource allocation, and even entering deep waters of redistributing interests and discussing allocation are required. This is the true test ahead, one that necessitates the central government's wisdom.

Finally, several favorable trends are emerging. This is not about mere survival for my WeChat account or blind optimism, but rather a thoughtful recognition that there are certain strategic opportunities for China as the world's second-largest economy:

Industrial involution has somewhat improved because local government-led industrial policies have become unsustainable due to a lack of funds. The capital market no longer highly values the high capital expenditures on new energy initiatives, and instead begins to punish reckless spending. The raw and blind drive for expansion has diminished. The central government has recognized the issue of tax competition among regions and has started to intervene. Most importantly, many companies can no longer sustain the intense competition and can no longer afford the losses. In the next 2 to 3 years, we will see the consolidation of leading companies, an increase in their market share, and price stabilization, with no more chaotic price cuts.

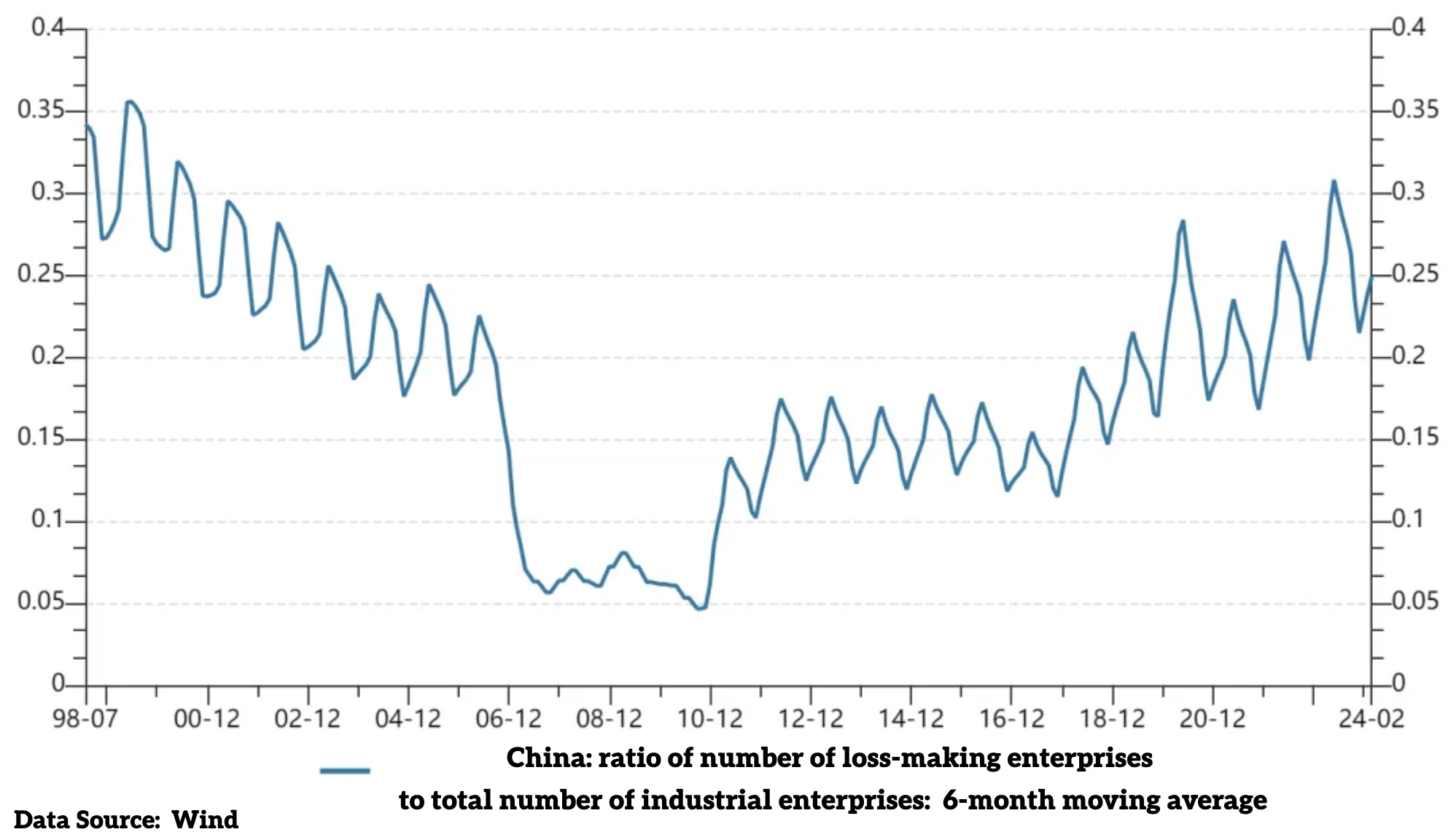

The proportion of loss-making industrial enterprises is steadily increasing:

The government will heavily invest in cutting-edge technologies, especially those requiring extensive social coordination and infrastructure, benefiting local talent and generating returns. Given the need for broad coordination and significant investment, state-owned enterprises are likely to benefit the most. ("Guiding state capital towards forward-looking strategic emerging industries")

The extreme reduction in costs for some individual products has begun to show positive social spillover effects. For example, the widespread adoption of electric vehicles has significantly lowered the per-kilometer cost of travel, which corresponds to increased mobility for people. Why is this important? A major wave of development in the United States was based on the extensive national highway system and the significant reduction in car prices, which led to a substantial increase in population mobility. Resources gathered in more efficient areas, and people had more choices. Of course, this requires the removal of restrictive factors such as household registration. At the simplest level, we have already seen short-distance travel become a beneficiary. Increased mobility also helps prevent the exacerbation of wealth inequality. Many poor residents in the United States are unable to integrate into overall economic development because they rely on deteriorating public transportation systems and do not have cars.

Industrial rotation: China's strong foundation in consumer electronics could benefit from a new wave if AI hardware becomes prominent, given that the consumer electronics sector has been quiet for some time.

Finally, on the topic of expanding overseas and developing emerging markets: If China can seize this opportunity to convert its excess domestic savings into assets in emerging markets, it can recreate another China abroad.

The transition period before Trump takes office presents opportunities. Trump represents a significant uncertainty and often acts against allies, causing countries like Ukraine to be on edge. This is an excellent chance for us to expand our diplomatic space. For instance, many Southeast Asian countries now view China more favorably than the U.S. Recently, China has played a significant role in mediating conflicts in Israel-Palestine and Russia-Ukraine. By timely disengagement from deep ties with Russia, China can potentially expand its international influence.

Important announcement: We are hosting the second “Ask Me Anything” live session this Wednesday, July 31 @ 9 PM Hong Kong (9 AM New York). This is going to be a 1-hour live webinar for you to ask the team about how we, as entrepreneurs, look at the 3rd Plenum, as well as any other questions you have, without limitations. The event is reserved for paid subscribers, but for a limited time, we are offering 5 free spots. Reply to this newsletter today if you are interested in joining, and we will email the Zoom link to the event to the first five free subscribers who reply!

My take on this, why?

1. Uncertainty in China's economy: Insufficient funds (currently) and extended amount of time to support de-stocking real estate. Slowing or even declining salary growth in some industries -> both don't help with the domestic consumption. Exports also face uncertainty due to slowing global demand and potential tariff effects.

2. Fear of persistent deflation. No one knows whether China will enter a Japan-like extended deflation period at this moment. We can have faith, but there's clearly uncertainty and fear of that possibility.

3. The policy did all right things, but the market wanted to see "surprising" proactive measures to address such uncertainty. They needed to see that for them to overweight China, but they didn't. It's not the market's job to be "long-term visioned." Even if they're bullish on China in the very long term, it doesn't mean they won't diversify risks given short-term volatility.

4. As the US Fed enters a rate-cutting cycle, other markets will be favored. Investors may weight markets like Japan and India more heavily than China, given less uncertainty (e.g., Japan just showing signs of inflation).

5. Implementation concerns, as you mentioned, including the timeline and the effectiveness of the measures.

6. The real problem behind delayed retirement: People don't just talk about it because it is the most obvious one, but because it impacts their spending power the most in a really tangible way. Delayed retirement doesn't guarantee a good job when you are 65, but it does guarantee delayed pensions. There still hasn't been a fundamental change proposed to the current social security system (which is extremely difficult and affects many interests, thus facing significant resistance. No one knows when is that coming). The urban-rural / state-private gap remains evident, and there's uncertainty from the outside about whether China is going to achieve common prosperity by lowering the salaries/social security of high earners or by elevating the lower classes to the middle class. Delayed retirement favors those within the system and urban areas under the current system. You can't ask people to have a longer-term vision if the system that affects their daily lives isn't fair in terms of salary and social security. Ultimately salary and income, that's what impacts consumer confidence and domestic demand the most.

After all, the market wasn't impressed but also wasn't selling off China. It's just a neutral response. Will need time to tell.

We really shouldn’t let the market judge economic policy. The market is so fickle and short sighted. Whereas economic policy has to maintain a steady course for the long term.

Anyway, be careful of falling into the trap of prioritising the market over reasoned discussion. Even Warren Buffet warns us that the market is a servant, not the master.