Post-pandemic consumer spending in China: key trends from the WeChat and Alipay consumer transaction panel

Strategic opportunities and emerging trends

In the post-pandemic landscape, understanding shifts in Chinese consumer behavior is both critical and complex. This report provides a detailed overview, exploring key questions about consumer purchases, changes in distribution channels, emerging trends in physical and service sectors, and significant macro trends and behavioral shifts across various income and age groups. By leveraging consumer panels derived from WeChat and Alipay transactions, this study taps into vital data sources at the core of China's digital payment sector, a rarity in the market. We offer a deep dive into fundamental macro trends and consumer behavior changes, presenting crucial insights for brands and investors seeking to understand the factors influencing China's consumer market post-pandemic.

For a limited time, we are offering a New Year's special: 20% off your annual subscription. Make sure to redeem yours before January 15, 2024!

Contents

Executives summary

Macro Trends

Transition to cautious and rational consumer spending

Shifting financial priorities

On consumer confidence and deflation concerns

Consumer behaviors

Channel update: physical goods

Young adults splurge on travel expenditure

Investing in education

Service & offline activities

Key takeaways: setting the stage for 2024

Introduction to the panel

The panel consists of the transaction records of thousands of individuals via WeChat and Alipay, which are the two primary e-payment channels in mainland China. The dataset spans from 2020 to 2023Q3 and is curated by our data scientists and statisticians to embody a balanced representation across gender, age, income classes, regions, and occupational sectors. Employing a rigorous scientific methodology in designing the panel's composition, we ensure that it serves as a representative microcosm of China's vast and diverse consumer landscape.

Accurate and representative: Alignment with China's National Bureau of Statistics

Retail growth (excluding automotive), as reported by China's National Bureau of Statistics, closely aligns with the year-on-year increase in average spending per person within our panel (refer to the chart on the left). Notably, 2023 witnessed a significant resurgence in the dining sector, with its recovery pace surpassing that of other sectors. This trend is mirrored in our data, where the retail growth specific to dining, as published by China's NBS, aligns closely with the spending patterns observed in our panel (refer to the chart on the right).

Panel demographics

Gender representation: Our panel consists of 60% female and 40% male participants.

Age diversity: The age range of our panel is concentrated between 25-50 years, capturing the core of China’s economic workforce (32% aged 25-30 and 50% aged 31-50). The presence of younger (13% aged 18-24) and older demographics (5% aged 50+) ensures a broad perspective on market preferences across generations.

Income spectrum: Income levels among our panelists primarily span the middle class, with 54% earning between 5,000 to 10,000 RMB per month, reflective of the average working citizen [1]. Those earning under 5,000 RMB represent 34%, providing insights into the spending behaviors of low-income citizens. The panel also includes individuals from higher income brackets (12% earning over 10,000RMB).

Notes on data collection and privacy standards: we adhere to strict legal and ethical standards in data collection. Participants provide informed consent and receive fair compensation. We collect data exclusively through a secure system, ensuring all sensitive personal information is anonymized. Our robust database and anonymous processing protocols further guarantee the privacy and security of the data collected.Executives summary

Our analysis reveals a significant uptick in individual spending levels since the 2020 pandemic, marking a period of economic recovery in 2023. However, per-person spending has not yet returned to its 2021 level, reflecting ongoing consumer caution.

Rebound with prudence: Our analysis reveals a significant uptick in individual spending levels since the 2020 pandemic, marking a period of economic recovery in 2023. However, per-person spending has not yet returned to its 2021 level, reflecting ongoing consumer caution. Notably, investment spending has continued to lag behind since 2021, signaling a cautious stance in financial confidence. Additionally, a decrease in consumer debt repayment suggests an improved debt landscape, but also a reorientation of financial priorities towards more modest consumption.

Revitalization of offline consumer engagement: The travel sector in 2023 has witnessed considerable growth, with increases in both average spending per person and transaction. The merge of online and offline experiences, particularly in online-to-offline (O2O) shopping, has seen a surge in expenditure. There's also an uptick in offline consumption through specialist stores, convenience stores, and interest-based experiences like entertainment venues.

Selective spending in key categories: While staples and dining have seen an increase in per-person spending in the first three quarters of 2023, transaction values haven't rebounded proportionately, indicating a volume-driven recovery in these sectors. Conversely, categories like education, health, travel, mother & baby products and services, and offline entertainment (movies, shows, spas, fitness, etc.) have experienced significant uplifts in both per-transaction and per-person spending. This trend suggests that consumers are being selective, prioritizing personal development, professional services, and interest-based activities.

Notes on category classification:

Debt: Short-term consumer loans like Meituan and Douyin monthly payments, commercial, credit card, and car loans are included, but car loans and mortgage payments are likely underrepresented due to lower usage of WeChat and Alipay for these transactions.

Dining: Expenditures at restaurants, fast-food chains, and cafes.

Discretionary: Non-essential purchases such as lotteries, home improvements, electronics, clothing, jewelry, and entertainment like beauty salons, spas, cinemas, and streaming services.

E-commerce: Transactions on platforms like Tmall, JD.com, Taobao, Douyin, and Pinduoduo, excluding grocery-focused O2O channels such as Hema (盒马) and Xingsheng Selected (兴盛优选).

Education: Costs for tuition, after-school tutoring, professional development courses, and exam fees.

Health: Medical and healthcare expenses, not including health supplements.

Investment: Spending on life insurance and fund management products such as ETFs, excluding flexible savings like Yu'e Bao (余额宝).

Staples: Daily essentials including groceries, utilities, rent, courier services, transport, and phone bills, plus purchases from grocery-focused O2O channels such as Hema (盒马) and Xingsheng Selected (兴盛优选).

Travel: Outlays for hotels, travel tickets, and tourist site admissions.

Macro Trends

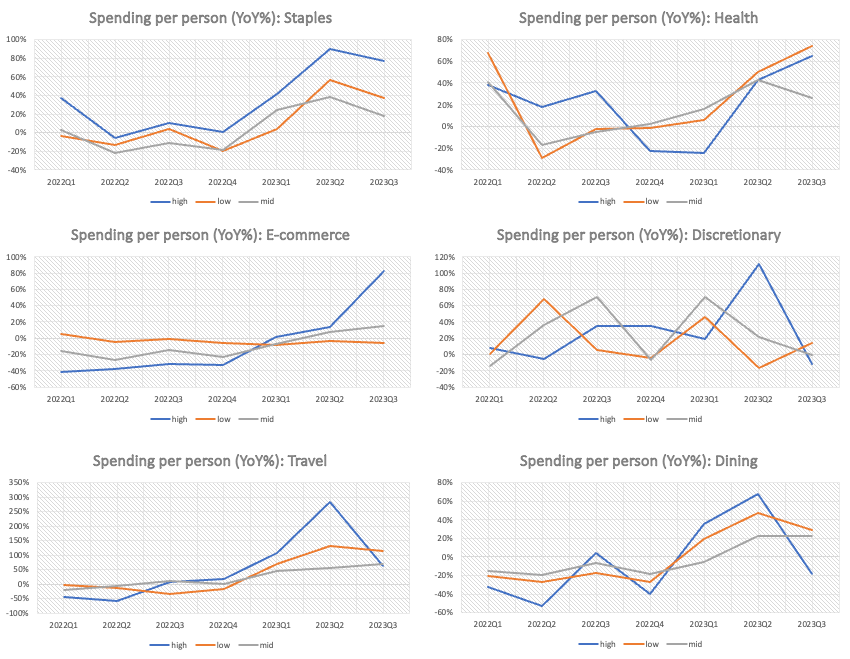

Consumption trends by income group: The low-income demographic, predominantly composed of young adults aged 18-24 — many of whom are students or in entry-level positions — has witnessed a rapid increase in average spending per person starting in 2023. The middle-income bracket demonstrated a steady recovery, while the high-income sector saw a peak in spending recovery in Q2 of 2023, followed by a cooldown in Q3.

Transition to cautious and rational consumer spending

By Q3, however, there was a noticeable slowdown in these categories as high-income earners pulled back, signaling a return to more cautious spending.

The short-lived spending splurge: In 2023, the high-income bracket drove a sharp uptick in spending across most categories, with a pronounced peak in Q2 for discretionary items, travel, and dining. This peak likely reflects a release of pent-up demand during the first holiday season post-pandemic and the Spring Festival (Labor Day in May, and the Dragon Boat Festival in June.) By Q3, however, there was a noticeable slowdown in these categories as high-income earners pulled back, signaling a return to more cautious spending.

The mid-income group exhibited a cautious approach to spending, lagging behind the high and low-income brackets in the speed of recovery within booming categories such as staples, travel, and dining in 2023. Their expenditure on discretionary items also showed greater fluctuation, suggesting a spending pattern closely tied to shifts in consumer confidence.

Note on income group classification: Low-income: Monthly income below 5,000 CNY; Medium-income: Monthly income between 5,000 and 10,000 CNY; High-income: Monthly income exceeding 10,000 CNY.

Shifting financial priorities

Expenditure on debt repayment has declined while investment sentiment stays subdued.

Expenditure on debt repayment has declined while investment sentiment stays subdued. Since 2021, there's been a consistent drop in the average per-person spending on debt repayment, which includes short-term consumer loans such as Meituan and Douyin monthly payments, along with commercial, credit card, and car loans. (Note: car loans and mortgage payments might be underrepresented due to less frequent usage of WeChat and Alipay for these transactions)

Meanwhile, investment expenditures, primarily on life insurance and fund management products such as ETFs (excluding more flexible savings options like Yu'e Bao 余额宝), have remained muted, showing minimal recovery from the low point in 2022 Q3.