Reconsidering Risk, Reward, and Allocation to China

If it’s zero, at least let's make it an informed zero

Beijing’s regulatory decision against online brokers last week, which we just wrote a note about, once again put the policy risk of investing in China in sharp focus.

On days like this, we think this is the perfect time to share with you a wonderful guest piece from Pandawatch that will give you a systematic review of risk, reward, and the right allocation strategy to China from the perspective of someone who has been working and investing in this part of the world for almost 2 decades.

Pandawatch‘s real name is Enrique Becerra, a Hong Kong–based investor who has managed his own capital full-time since 2017, focused on China A-shares and Hong Kong-listed equities. He is the author of the monthly letter “Investing in China”. He also tweets @pandawatch88. Based in Hong Kong since 2007, he spent 16 years as an M&A investment banker at Citi and Bank of America Merrill Lynch, most recently as Managing Director and Head of Asia Financial Sponsors, executing deals across Greater China, Korea, and Southeast Asia.

Enjoy!

Reconsidering Risk, Reward, and Allocation to China

By Enrique Becerra a.k.a Pandawatch

Why this article exists.

Back in January I published a deck called A Hitchhiker’s Guide to the China Stock Galaxy: 2026–2030. I made it because in conversations with fund managers I kept hearing the same story: it has become really hard to have a meaningful discussion with US and European allocators about China.

The moment someone in the room says “yeah, and what about Jack Ma”, “tutoring stocks”, or “Taiwan”, the conversation ends. Zero nuance. This piece puts these one-liners under scrutiny.

Because of the above, many have missed a 15% China rally in 2024, then a 30% rally in 2025, and then the doubling of the onshore tech index Chinext over the last 12 months.

Or at best, enjoyed a 3% allocation to it. Wait what, 3%?!

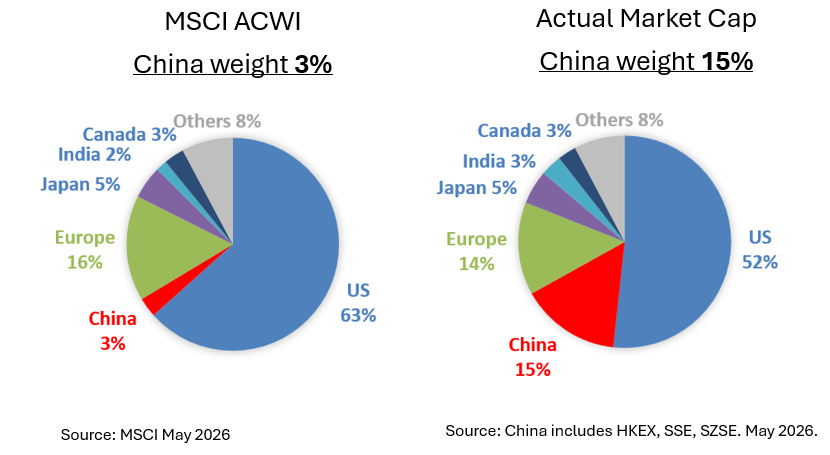

Intro: According to MSCI and FTSE, the China market is the size of Canada.

China is the second largest equity market on the planet, at about USD 22 trillion of market cap across Hong Kong, Shanghai and Shenzhen. It is also the second largest market in terms of overall liquidity and number of Fortune 500 companies.

However, China weight in the global index benchmarks MSCI ACWI and FTSE All-World is 3%. The same as Canada. Half of Japan.

If we were to re-do the MSCI ACWI by actual market cap, China weighting would be 15%. Similar to its share of global GDP, which makes more sense.

There are a few reasons why both MSCI and FTSE do the weights the way they do. It doesn’t mean you should too, as it may not give you a balanced global exposure.

I don’t expect this massive underweight to close anytime soon. Changing the methodology to more closely align to market cap would mean reducing US from 63% to 52% and corresponding outflows. Good luck to MSCI CEO in that endeavor. But the gap may eventually narrow, and this is something to keep in mind.

What is the right number? We come back to why this article exists: many institutions operate in an environment not conducive to having a nuanced discussion about China investment risks or rewards. And without an informed view on risk and reward, you can’t size a bet.

The article is divided in three parts. Part 1 talks about five risks. Part 2 talks about three rewards. Part 3 talks about strategies to allocate money.

The point of this piece is to help allocators re-examine their China assumptions. Do not treat it as a comprehensive review of risk or a scientific paper, but a source of ideas and ammunition to discuss with peers. The answer may still be a zero China allocation, but at least it’s an informed zero.

Part 1: A better understanding of Risk in China.

Some investors (not you of course, dear reader) approach China risk in the same way they approach the country weightings: “if MSCI says it is 3%, that is probably the right number.” Therefore “if well-regarded guru says that a conflict in Taiwan means China equities are a doughnut, that’s probably the right pastry.” Investors love narratives, heuristics, and outsourcing due diligence to others.

Below I examine five common China risk narratives:

China is ultracompetitive, nobody makes any money

Your upside is capped, the government doesn’t let companies become too big

The core mission of Chinese companies is different from US companies

Regulations move fast in China

Taiwan

The first two sound good in the echo chambers, but are light in substance. The last three are more serious.

Risk 1: “China is ultracompetitive, nobody makes any money.”

Saying this has become very trendy recently. People will reference a book author that makes this point in every podcast, or a post on X from someone that just did a factory tour in China. It sounds smart, fits many priors, and if you look at the actual numbers, it turns out to be inaccurate.

As with every good-sounding story, it must have a piece of truth. And for sure: certain industries, like solar, are incinerating money.

The missing truth however is that in a majority of very competitive industries, like EVs, consumer electronics, retail, industrial automation, etc, you have market leaders making good money: BYD was loss making in 2019 and made USD 4bn in profits in 2025, while its competitor Geely doubled profit this year to USD 2bn. Xiaomi was making USD 1bn in profit in 2019 and made USD 5bn in profits in 2025. Midea and Haier, competing white goods manufacturers, or Anta and Lining, the two largest Chinese sportswear brands, have all doubled profits in the 2019 – 2025 period, while navigating a very tough and deflationary consumer macro environment. Among industrial manufacturing names, heavyweights like Nari or Inovance have doubled and tripled their profits respectively in the same period.

Survivorship bias in the sample? Maybe. What about the generic widget manufacturer with 1% market share? Yes, that one is probably struggling. It should be noted here that 40% of the companies in the Russell 2000 have negative earnings. Losses are not a uniquely Chinese export. Takeaway for risk management? Do not predict, observe, invest in the ones growing profits. Another takeaway: question hot takes from podcasts, numbers please.

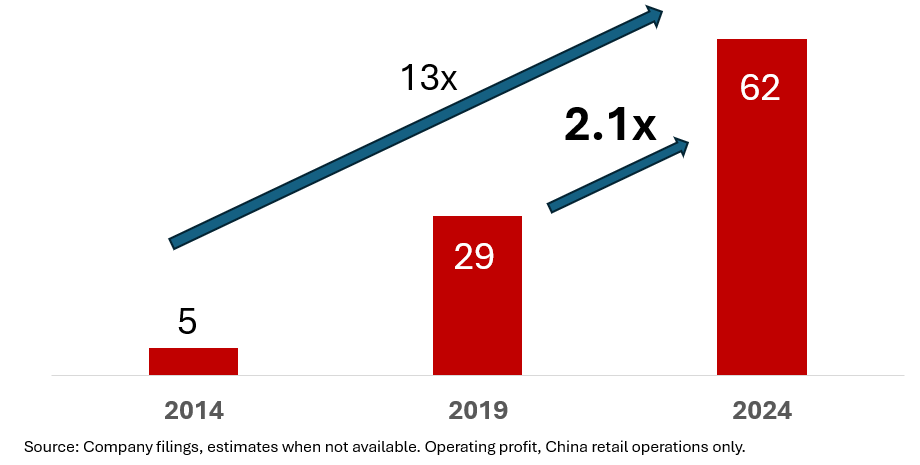

Profits do not always go in a straight line up and to the right. There are investment cycles and there are collecting cycles. The combined profit pool of the top 10 retailers in China doubled from USD 29bn in 2019 to USD 62bn in 2024 despite the industry experiencing intense ecommerce rivalry in 2021–22. In contrast, in the same period, the top 10 US retailers, despite a milder competitive environment and much better consumption macro with stimmy checks, just grew their profit pool by 50%.

Back to China, 2025 saw another investment cycle begin among ecommerce players aiming to expand the pie of quick commerce and fight for the largest piece. We’ll see how that shapes out in 2026-27, and if we come out the other side with usd100bn combined EBIT.

China Top 10 retailers EBIT (USD bn).

Competition? Big. Killing industry profits? Not necessarily.

Risk 2: “Your upside is capped, the government doesn’t let companies become too big.”

China currently has 23 listed companies with market cap above USD 100bn, and 8 of them are controlled by entrepreneurs. Ten years ago, it was basically just one. Entrepreneurs and their shareholders have made money.

At the start of 2026, Hurun counted 1,000 billionaires in China vs. 550 in 2016, doubled. The top 10 today are worth USD 490bn vs. USD 190bn in 2016, more than doubled.

If the system was set up to chop tall trees, one would expect the counts above to be stagnant. What is stagnant is the number of billionaires publicly criticizing SOE banks.

Let’s move on to what I consider more serious risks. The first is more philosophical, the next two more tangible.

Risk 3: The core mission of Chinese companies is different from US companies.

Borrowing some reasoning here from Midea’s chairman: the history of the Chinese equity market is too short. Private companies and the stock market have existed in the US for 200 years. In China, for less than 40 years.

In the US there is a well-established understanding: companies are not expected to shoulder excessive social responsibilities; their core mission is to maximize profit and shareholder value.

In China such consensus has yet to be formed. The experience is too brief. Right now, the stock market exists to serve “the real economy”, and companies exist to serve “national development” goals. An investor in China must be aware of what these goals are.

For example, from a recent article in Qiushi outlining economic priorities: “…to foster a group of new growth engines, including new-generation information technology, artificial intelligence, biotechnology, new energy, new materials, high-end equipment and green industry during China’s 15th Five-Year Plan period (2026-2030).”

If you don’t pay attention to the shift in goals, you risk missing the action. Or worse, you risk being offside, which takes me to our next risk.

Risk 4: Regulations can move fast in China.

For better and for worse. We are going to focus on the “for worse” here, with a few examples. There’s nothing too esoteric behind regulatory actions and the tea leaves come in capital letters. The issue is execution, which is faster than in other jurisdictions and can lead to wild price moves.

First, in many cases regulatory action is actually not that fast, but still somehow manages to surprise investors:

The afterschool tutoring ban came after 2 years of warnings (in NPC statements and state media) about the pressure this product was putting on families. Investors ignored and kept buying, chasing price. When the regulatory hammer came, EDU and TAL were trading at 80x LTM PE

Last week, after three years of warnings, FUTU and two other online brokers got fined by CSRC around 15-20% of annual profit for servicing mainland residents without a securities license (people were wondering if CSRC had forgotten about them, nope they had not). Investors learn though, and this time when the penalty arrived the valuation was not 80x PE but 12x PE, already carrying the regulatory uncertainty

Other times regulation does come very fast as a response to specific company actions like:

Didi rushing a US IPO in June 2021 ahead of a new data law coming into force in September 2021 (risk factor #6 in the prospectus). Two days after the IPO, CAC launched a cybersecurity probe, banning new user registrations and pulling the app from domestic stores

The well-documented drama around Ant Group, which needs no recap

And in other cases, regulatory action comes to companies where users complain about market dominance, but the trigger and timing can be random and abrupt. For example:

Antimonopoly investigation into Trip.com, where small hoteliers had been complaining to local regulators that the platform was forcing them into exclusivity and to give up control over room rates. Trip got a few small fines over the past couple of years, but eventually SAMR decided to jump in. Meituan went through a similar process in 2021 and came out with a USD 500m fine but higher revenue and margins (they have bigger problems now, I’m sure they miss SAMR)

The caps on pricing for online consumer lenders like QFIN and FINV, an industry where in the risk factors of smaller players you can read gems like “we indirectly charge our borrowers in the manner our borrowers are not aware of.” Turns out borrowers found out

Regulatory action aimed at companies extracting rents is not a uniquely Chinese export, see FICO and UnitedHealth investors for details

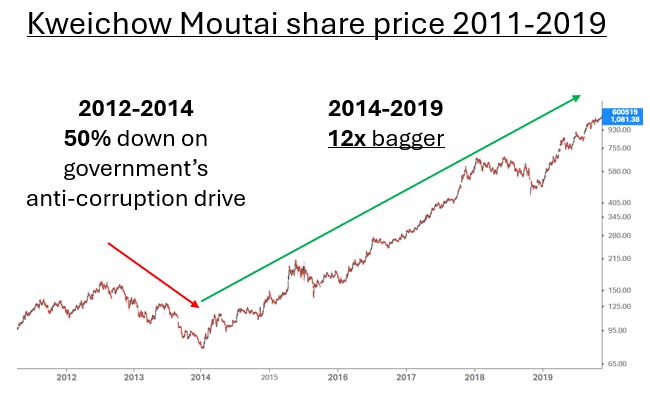

Finally, regulatory action can provide opportunity. Moutai was a 12x bagger in 5 years after regulations to curb government spending on banquets and gifts took the stock down 50%. It is important to distinguish between regulations targeting the company, the product, or the behavior.

Practical implications for risk management: there are 8,000 listed companies in China, minimize your exposure to those working against the direction of policy (see risk 3). If you want to be involved because the risk reward set-up makes sense, size appropriately.

Risk 5: Taiwan.

Everyone has their own very thoughtful take on CCP stated goals, DPP stated goals, the outlook for the new KMT president, and the latest DJT commentary. Fine.

As an investor looking to measure this risk, I just look at the issue in two ways. First, the incentives for something to happen, and second what then if something happens.

In the short and mid-term, the incentives for all three parties point against escalation. US does not want to lose access to TSMC fabs or the supply chain for DC infrastructure components. It would slow down AI progress. Intel is not going to make cool Rubins anytime soon. Further, without access to TSMC, Nvidia, Microsoft, Google, and Apple share prices could be cut in half. The other two parties would suffer tragic human losses. No one wins much.

But accidents can happen. And here investors do a quick “reasoning by analogy” and assume China stocks are a zero, because of what happened to Russia. The analogy doesn’t work because China is a different global economic actor than Russia. In a Taiwan conflict, with the global tech supply chain in disarray, are you so sure that US and Europe will go down the massive sanctions route, and further spread the pain to industries that rely on access to China supply chains or sell to Chinese buyers? Maybe yes. But maybe not.

Before assuming this scenario is a zero for China stocks, a bit more work should be conducted on incentives, dependencies, and resilience. Once the work is done, maybe we find out that one way to diversify this risk, which would hit global equities hard, is to actually own some China. Counterintuitive? Huawei chips are not using TSMC fabs, and China has its own domestic datacenter supply chain.

Hope we don’t have to test any of this. People on both sides just want to keep enjoying life, eating good food, and having fun with friends. Let’s keep it that way.

[Baiguan’s note: Robert recently wrote about why it is highly unlikely for China to take military action against Taiwan]

Wrapping up the risk section.

Other risks not discussed here, but that you should think about, include:

“The GDP has doubled, but the stock index has not, means massive dilution” which if you are versed in basic arithmetic you can quickly dismiss by looking at the expansion in the number of index components

Known-unknowns such as deflationary cycle and population contraction

Unknown-knowns such as what comes after the Xi era

And unknown-unknowns which, you see, I don’t know

Human systems live in a critical state. Never underestimate what can come next.

Part 2: The Reward side of the equation.

Like the risk side, the reward side in China often suffers from the same: too much story and little substance. Back in 2010 we IPOed restaurant companies in China with “80 locations but TAM of 1.2bn people”.

Let’s tackle the reward side in a more serious and tangible way. I’ll cover three:

At the portfolio level, China offers diversification of economic outcomes

At the company level, geopolitics is paradoxically expanding TAM and accelerating growth

At the market level, domestic capital markets are going through a step change that is bringing new ideas to investors

| A guest post by

|