Tencent games losing its edge? Let's settle the debate here.

Assessing Tencent's position in the evolving Chinese mobile gaming industry

*This post is part of our premium content. Thank you for being a valued subscriber.

Tencent released its mixed Q2 financial report on Aug 17th. The advertising revenue beat market expectations thanks to the monetization efforts from Video Account. Nonetheless, the game sector disappointed investors with a 8% Q/Q decline, sparking negative discussions about the performance of Tencent Games. As a result, the stock price has been on a continuous decline, nearly reaching its lowest point of the year.

At the beginning of this year, Tencent's stock rebounded to over HKD 400, and has since remained around HKD 320. Although the current market sentiment remains somewhat lackluster, we believe that 'it's better to mend the nets when it's calm.' As market conditions settle, investors' attention will eventually shift back to fundamentals. In this context, we intend to conduct an in-depth analysis of Tencent gaming business, discussing the challenges the company confronts and evaluating potential instances of market overreaction to its stock price.

1. Why do investors attach such importance to Tencent's mobile gaming business?

Value-added Services (VAS) segment has consistently represented 50% of Tencent's revenue over the long term. Given the lack of growth stimulus in the non-gaming sectors, comprising literature, music, game streaming, and long-form video membership services, the online gaming segment, accounting for 60% of VAS, has become as one of the most closely watched sectors by investors.

From an industry perspective, the boom in China's mobile gaming industry began in 2015, and Tencent's flagship game product, Honor of Kings, unquestionably stands as a milestone in the mobile gaming landscape. The launch of HoK also enabled investors to recognize Tencent's potential in mobile game production and distribution.

Figure 1: Mobile gaming users grew rapidly from 2015

Figure 2: The mobile gaming market reached RMB 200 billion, tripling from 2015

Source: CNG, curated by BigOne Lab

As mobile gaming segment contributes significantly to both topline (revenue) and bottom line (net profit), its business performance becomes the primary driver of Tencent's stock price. Looking at historical experience, every major upswing or downturn in Tencent's stock price has been closely tied to the performance of its mobile gaming business and related policies.

Figure 3: The great success of Honor of Kings and Peacekeeper Elite propelled the stock price to rise

Source: BigOne Lab

2. Tencent game business is now facing dual challenges of fundamentals and future incremental revenue contributions

For gaming companies, most investors primarily focus on two key aspects when analyzing financial performance:

1)The fundamentals: This includes the revenue performance of existing games and assessments of their lifetime-vaule (LTV). Typically, gaming companies that have successfully released long-lasting products tend to be favored by investors. This indicates that the company has a strong understanding of game operations and users' preferences. Examples include Netease (listed on both HK and Nasdaq, ticker:9999.HK or NTES, known for titles like Fantasy Westward Journey and Journey to the West) and G-bits (an A-share listing game company, ticker: SH603444, known for Asktao Mobile and Overmortal).

Source: BigOne

2)The visibility of new games: Chinese gaming companies often rely on in-game purchases to generate grossings. Therefore, game developers often invest significant marketing resources in the initial stage to achieve instant success. From countless experiences, the performance of high-profile new games in the first two months can significantly impact the company's stock price.

In summary, the current performance of the existing game portfolio often determines the core valuation of the gaming business (the median of P/E band), while expectations for new game releases determine how much premium investors assign to the gaming business.

Tencent's gaming business is currently facing dual scrutiny from investors.

Despite the fact that Honor of Kings and Peacekeeper Elite are maintaining Top3 positions on the best-seller charts, in a climate of negative sentiment, investors still have the following three concerns about the performance of these two games going forward.

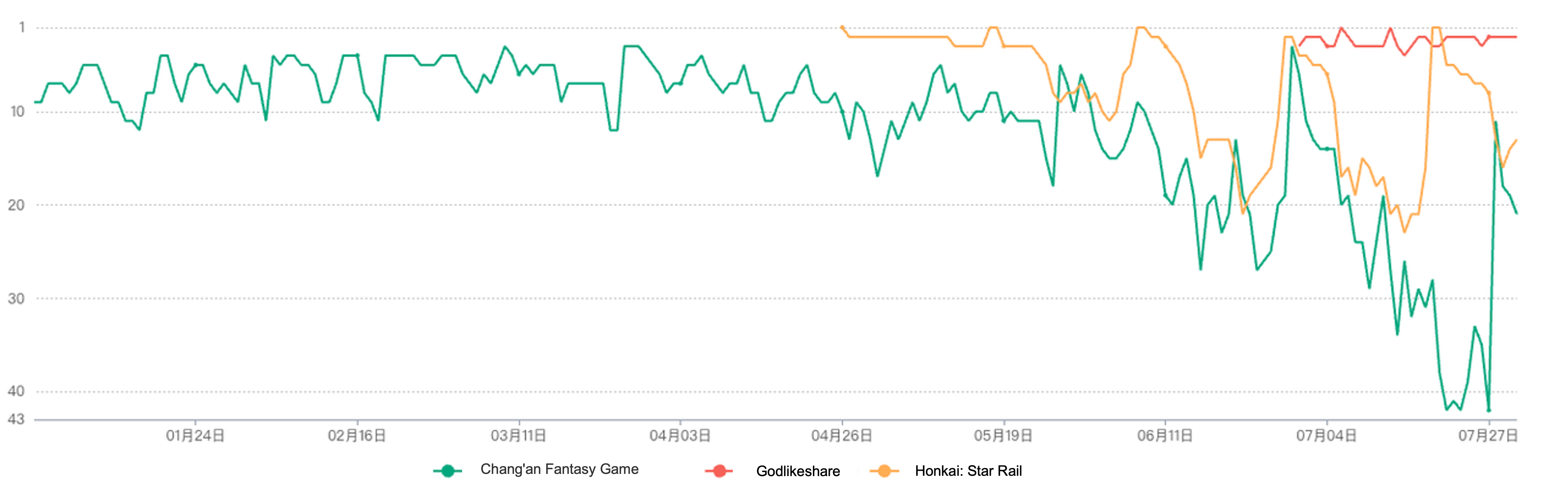

1) These two games have a significant impact on the gaming business, and if their revenues were to decline substantially, it could lead to a collapse in the overall gaming business valuation. At their peak, these two games contributed to over 50% of Tencent's mobile gaming revenue, and while their influence has gradually declined, it still accounts for nearly 30%. Moreover, the release of blockbuster games by competitors in 1H23, such as Honkai Impact 3 (miHoYo), Chang'an Fantasy (DreamQuest Games), Justice Mobile (NetEase), etc., raises concerns among investors about whether these two games, which have been in operation for over five years, can continue to attract users' attention.

2) Over time, WeChat and QQ have consistently harnessed the power of their social platforms to amplify the reach and impact of Tencent Games. However, with short video platforms gaining more user traffic and emerging as new distribution channels, investors are concerned that Tencent's previous distribution channel advantage may no longer exist.

3) Tencent's mobile gaming revenue in China reached approximately 110 billion RMB in 2022, with a market share exceeding 55%. This has set a more stringent criterion for upcoming game releases in the eyes of investors. After all, a mobile game ranked No.10 on the grossing chart only contributes 5% to Tencent's gaming business. However, the current pipeline visibility for such titles is relatively low.

Figure 4: The major releases by peers in 1H23 have made the competition even more intense

Source: Qimai grossing chart

Amidst prevailing pessimistic sentiments, our perspective takes a more optimistic stance. We will elucidate our views on Tencent's fundamentals from the perspective of the Chinese mobile gaming industry, user dynamics, and Tencent's channel value. Additionally, we will analyze the visibility of gaming content and overseas business expansions. The forthcoming content will primarily address the following questions:

Has the Chinese mobile gaming industry reached its saturation point, and where will future growth drivers emerge?

Follow-up Topic: how to assess the impact of licensing restrictions and pandemic-related lockdowns on the gaming market.

Have the values of WeChat and QQ channels been diminished?

Follow-up Topic: How to assess the lifecycles of Honor of Kings and Peacekeeper Elite.

How should we view the argument that 'Tencent Games cannot create high-quality content'?

2.1 What Factors Are Shaping the Future of the China Mobile Gaming Industry? --Understanding the Industry's Growth Potential

As demonstrated by industry data presented earlier (Figures 1 and 2), the gaming market experienced a decline in 2022 after years of continuous growth. Coupled with the leveling off of mobile gaming user growth, investors have become increasingly concerned about the future of mobile gaming. Investors are worried that the short video platforms continue to pose threats to the gaming industry and are also anxious about that users' affection for games may be temporary. Meanwhile, they perceive regulatory impacts as a long-term hammer overhang to the gaming industry.

We do not believe that the downturn in 2022 signifies the end of the road for the mobile gaming industry. Let's dissect these concerns one by one.

To begin with, short video platforms were not the root cause behind the market's decline in 2022, and their negative influence on the gaming industry has been gradually diminishing since 2021. While short video formats are indeed more effective in grabbing users' attention, their ability to siphon off the gaming market has weakened. Both user engagement and content strategy from platforms like Douyin and Kuaishou have shown signs of slowing down, indicating a diminishing impact on other content formats. A research study specifically examined the proportion of time spent by mobile gamers on various apps and found that the rapid acquisition of gaming users by short video platforms peaked in 2019-2020. However, entered into 2021, these gaming users' time spent on gaming apps had stabilized. Combined with the slower growth in both user base and user engagement for Douyin and Kuaishou, it suggests that short video platforms are gradually exerting less pressure on the gaming industry.

Figure 5: The time distribution of gaming users on the internet

Source: HMM Data, curated by BigOne Lab

Figure 6: User operating metrics of both two giants are about to enter the plateau

Source:1)Metrics of Kwai, incl. Kuaishou Flagship, Kuaishou Express and other Kuaishou Concept apps, were disclosed by the company. 2) Metrics of Douyin flagship app were provided by HMM Data.

The stability in the proportion of user engagement time already reflects the irreplaceability of games for users. Furthermore, when we observe user behavior from the perspective of their affection for games and their stickiness, the answer is affirmative. Both the monthly downloads or the 30-day retention rates of existing users indicate that the stickiness of games to users has not undergone significant changes.

Figure 7: The download data reflects the consistent appeal of mobile games to users.

Source: Qimai, curated by BigOne Lab

Figure 8: 30-Day retention ratios of popular mobile games are stable

Source: HMM Data, curated by BigOne Lab

We believe that the decline in the gaming market in 2022 can be attributed to two main factors: supply-side impacts due to regulatory and macroeconomic issues.

1) The regulatory impact: The implementation of various licensing policies in the past has consistently led to significant fluctuations in the gaming market. In 2018, the freeze on game licensing led to a sharp decline in the gaming market's growth rate, dropping from 42% in 2017 to 15%. When licensing resumed in 2019, the lack of blockbuster new games resulted in a modest recovery, with the year-on-year growth rate reaching only 18%. It wasn't until 2020 that major companies started releasing hit games, bolstering revenue base and driving the gaming market's year-on-year growth rate up to 33%. In 2021, there was another suspension of game licensing, compounded by the enforcement of regulations for the protection of minors. The negative impact on the gaming market this time around was even greater than in 2018.

2) The economic impact: In 2022, the economic environment, coupled with China's stringent COVID-19 lockdown policies, had a certain negative impact on game monetization efficiency, particularly among the middle to high-income individuals. As a result, mobile games, especially hard-core ones, were negatively affected. We observed that high ARPU (Average Revenue Per User) games, primarily MMOs, collectively experienced a significant decline in 2022.

Figure 9: Mobile game market resumed growth trajectory after four consecutive quarters following the normalizaion of license approval (4Q18)

Source: CNG, BigOne Lab

Figure 10: High ARPU Games become more volatile after the pandemic lockdown in 2022

Source: Qimai

2.1.1 Follow-up Topic: how to assess the impact of licensing restrictions and pandemic-related lockdowns on the gaming market.

We believe that both licensing suspension and the pandemic were major factors contributing to the fluctuations of mobile gaming market , albeit with differing impacts. The pandemic lockdown, which provided users with more leisure time, combined with more frequent operational activities by game companies, leading users to overdraw their wallets. This impact is relatively short-term and can be mitigated by adjusting the pace of game operations. The licensing suspension primarily impacts the supply side, making its effects more far-reaching. Based on the experience from the 2018 License Freeze, industry revenues gradually recover after the resumption of licensing, but normalized growth often takes six months to a year after the licenses are reinstated.

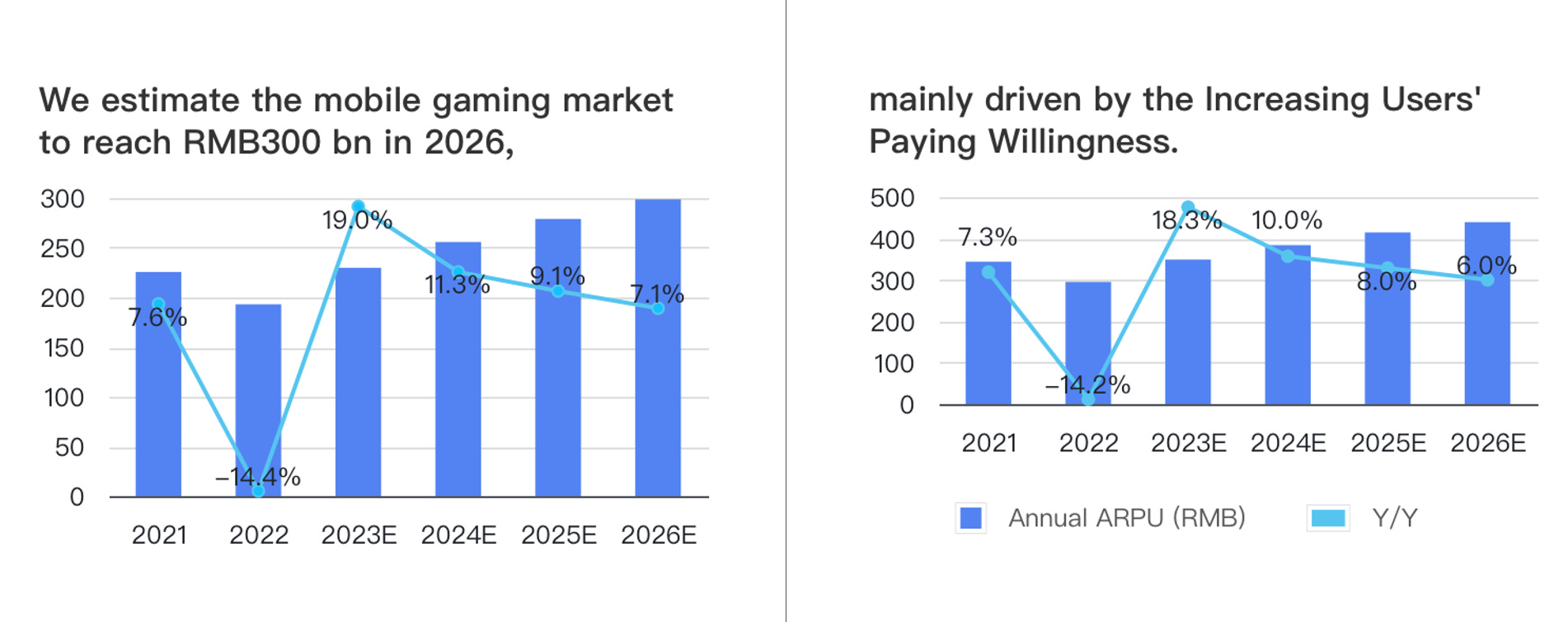

With the supply-side gradually recovering thanks to the resumption of license approvals, we expect the gaming industry to achieve Y/Y growth within one year. Meanwhile, both the improving ARPPU for existing games and the performance of new releases indicate the increasing user paying willingness. This undoubtedly shines a brighter light on the mid-term development of the mobile gaming industry. We believe that the era of the mobile gaming industry relying solely on user growth has passed, and future driving factors will primarily revolve around the enhancement of user willingness to pay. We expect the mobile gaming industry to achieve a 12% CAGR from 2022 to 2026, with ARPU contributing 11% and game users contributing 1% to this growth.

Figure 10: ARPU for Tencent games continued to grow and reached record-high in 2Q23

Source: Tencent Official Website, curated by BigOne Lab

Figure 11 and 12: Mobile game market forcasts

Source: CNG, BigOne Lab estimated

Now that we have examined the potential of China's mobile gaming industry, our focus will shift to Tencent's position within this context. Are investors' primary concerns about Tencent valid? For the following sections for paid subscribers, we'll explore if Tencent has truly lost its edge in distribution channels, notably WeChat and QQ, and its ties with the gamers community. Expect in-depth analysis featuring key data on user engagement: game downloads, game activations via WeChat & QQ, and engagement metrics for Tencent's flagship games.

Additionally, we will delve into Tencent’s recent strategies aimed at broadening its user base on WeChat channels and its initiatives in the global market. To round it up, a valuation and forecast of Tencent, incorporating all these factors, will be presented.