What gets Chinese consumers to spend - Charts of the Week

"Charts of the Week" is Baiguan's series that features key data points to help you quickly grasp the general state of affairs in China in just a few minutes. We handpick the highlights of the data charts from a variety of sources, analyzing and delivering insights trusted by 100+ top institutional and corporate clients worldwide at BigOne Lab. Don't forget to subscribe before you continue reading!

Welcome to this week's edition of "Charts of the Week." In today's newsletter, I've selected 12 charts that highlight the latest trends in domestic demand, hiring, and salaries, as well as investment opportunities and risks in the consumer sector that are worth paying attention to.

China's retail sales growth slowed in June 2024, with the year-on-year growth rate at 2.0%, down 1.7% from May and falling below market expectations. Consumers were not extravagant during this year's "618 festival" (China's biggest mid-year e-commerce sales event), and the slowing consumer demand was compounded by the slowdown in large-ticket consumer goods such as passenger cars.

Large-ticket goods sales cool down

Following the 3rd Plenum, China has launched stimulus programs such as ultra-long treasury bonds to fund trade-in programs and subsidies for large-ticket consumer goods such as electric vehicles and home electronic appliances. While this may boost domestic demand in the near term, it remains uncertain to what degree overall domestic consumption will be stimulated. The trade-in programs for home appliances, which have been used multiple times in the past and worked well, may not bring as much of a boost today. This is due to the higher penetration of home appliances in Chinese households compared to a decade ago and consumers being more conservative with their financial approach.

Passenger car sales, which grew robustly during 2023 boosted by subsidies and discounts, continued to grow in the first half of 2024, but at a slower pace. During January-June, total passenger car sales grew by only 1.6% year-on-year, and in June, decreased by 7.4% year-on-year, despite domestic automakers aggressively slashing prices to win customers.

What gets consumers to spend: the income expectation

Ultimately, income expectations and the real estate outlook remain the pillars that affect consumer confidence and their willingness to spend.

Salary expectation: Across major online recruitment platforms, we observe that the year-on-year growth of the average salary slowed in Q2 2024. I expect consumers to remain cautious as salary growth continues to be slow, and fears of salary cuts spill over from industries such as finance and internet to other sectors.

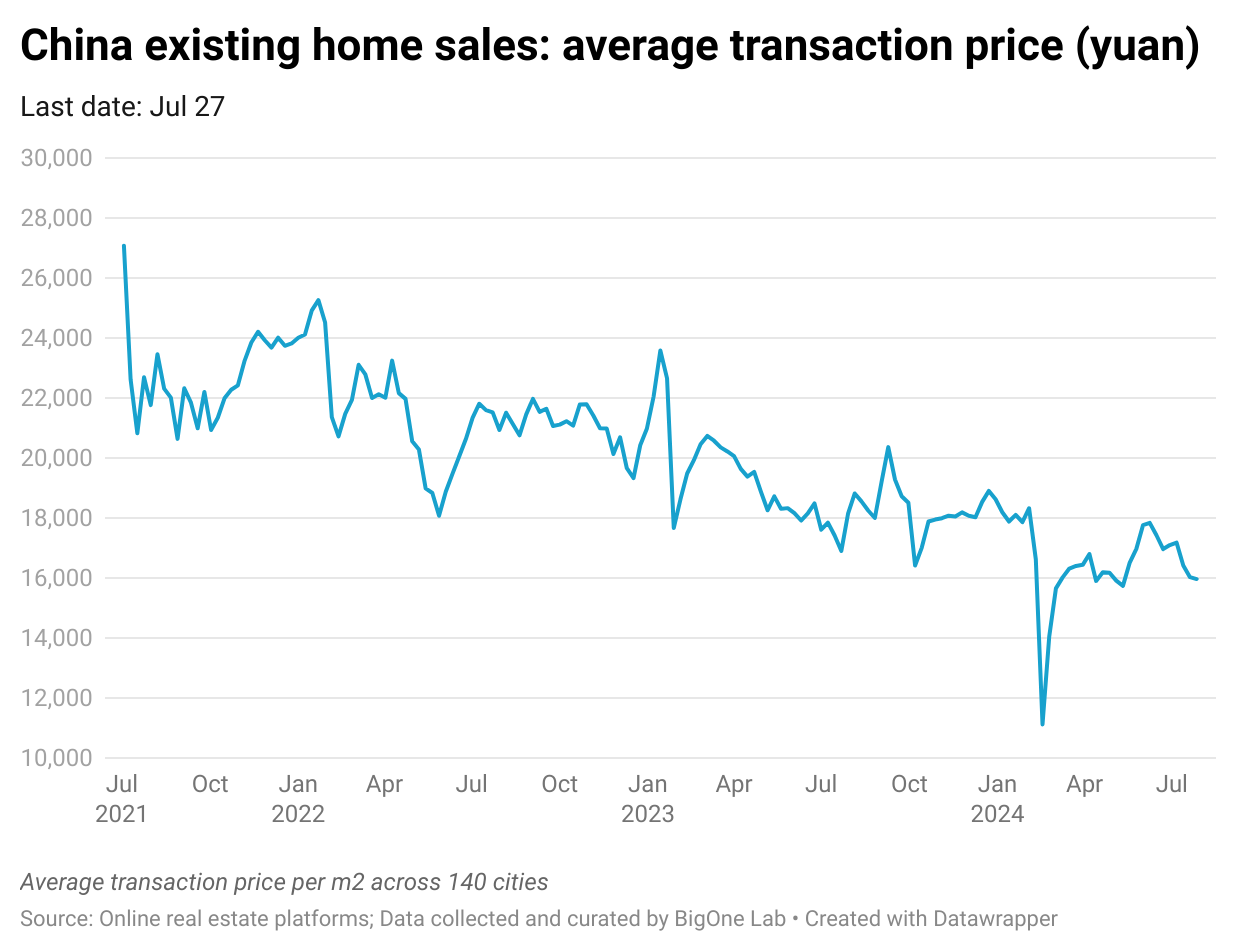

Real estate: The boost from the stimulus policy launched in May may have been digested by the market for now. The total transaction value and average transaction price of existing homes in 140 Chinese cities cooled down in July, after existing homes (especially those in desirable locations and school districts) in first-tier and new first-tier cities (mostly metropolises and municipal capitals) experienced a round of destocking in May and June following the stimulus.

Continue reading behind the paywall to get updates on:

Real estate: existing home transactions across 140 cities in China

Youth unemployment

China's hiring trends

E-commerce platform performance in Q2 2024 (Douyin, Tmall, JD, Kuaishou)

Sectors with potential investment opportunities & risks given current consumer sentiments:

Sports brands (e.g., Nike, Lululemon, Anta)

Skincare brands (e.g., L'Oréal, Proya)

Long-term trends such as the pet and designer toy sectors

To get a sense of what is offered, you are welcome to check out this older post in the same series: Charts of the Week. You can also get free access by sharing us.