The "Athleisure" Trending in China: Sports & Health Is Set to Become China's Structural Growth Sector in 2026

Chinese consumers going after "old money" sports look

If you’ve been to Beijing’s Guomao CBD or Shanghai’s Xintiandi recently, you might have noticed something: those urban professionals who used to carry Hermes or LV bags are now wearing On running shoes, Lululemon leggings, and holding sugar-free drinks.

This is an important shift in the fashion statement.

The year 2026 has so far seen a strong rebound in China’s sports and health consumption.

According to Bigone Lab‘s online sales data (across Tmall, JD, Douyin, etc.), the sports and health industry maintained +22% growth in January-February, accelerating from +18% in December and +12% in Q4.

What makes this remarkable is that this growth is entirely organic—no government subsidies, unlike appliances or electronics. Outdoor apparel and footwear have been particularly strong, with outdoor footwear growing 65% and outdoor apparel 47%. Sportswear, in general, showed significant acceleration at +31%, compared to just +5% in Q4.

But it’s not just about sports. A broader “healthy lifestyle” wave is sweeping through Chinese middle-class consumers.

For instance, as I covered previously, the low-sugar trend has become an up-and-coming lifestyle statement that’s trending among urban Chinese.

China’s Growing Appetite for Low-Sugar Living: From Happy Fat-Boy Water to Health-Conscious Choices

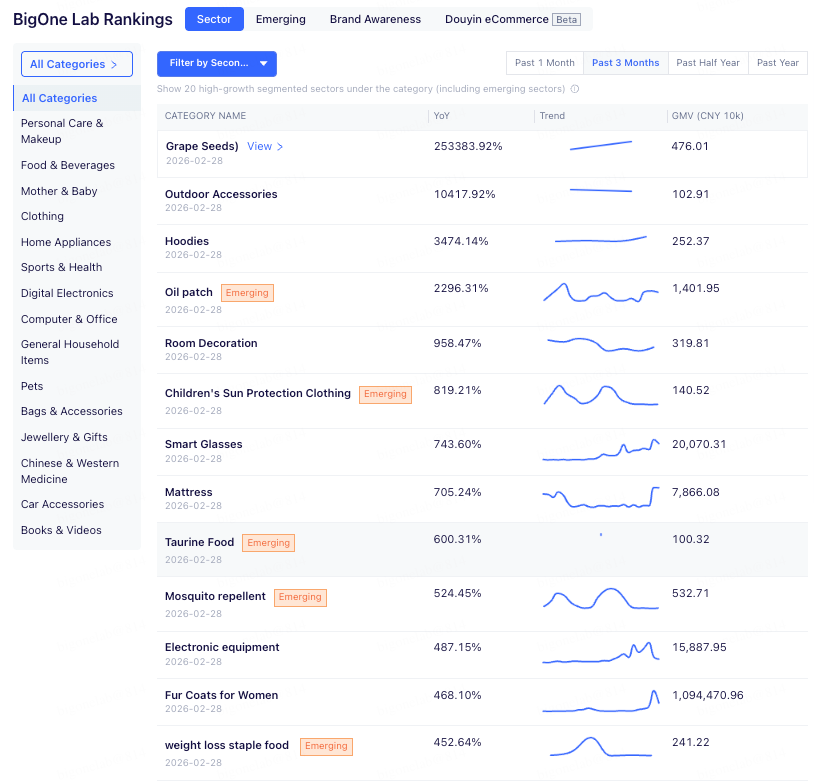

Apart from no-sugar or low-sugar beverages, over the past three months we’ve seen several interesting, niche yet emerging categories rapidly growing across e-commerce platforms, such as grape seed extracts, taurine food, and weight-loss staples—novelty items marketed to boost metabolism or support overall health.

Chinese consumers are becoming increasingly conscious about what they put into their bodies. Sugar-free beverages, metabolic supplements, and functional foods are no longer niche categories, but lifestyle choices.

“Athleisure”: the new trending lifestyle

But there’s an even more significant trend beneath the surface: “athleisure” is on the rise.

As we’ve covered since 2023, the “quiet luxury“ and “old-money“ aesthetic has been trending in China. From 2025 onward, this trend has evolved further: China’s “old-money” consumers are increasingly embracing sports, and their attitude toward luxury is shifting—from using brands as status symbols to focusing on how clothing feels on their bodies.

A simple “no-logo” or understated design no longer satisfies the “old-money” consumer. This aesthetic has gradually evolved into a broader lifestyle system, encompassing diet, leisure activities, vacations, and, most importantly, sports and overall health routines.

In urban Chinese cities, it has become common for professionals to wear sportswear four or more days a week. Sportswear is no longer purely functional—it is increasingly what urban professionals choose for social and even work occasions.

As sports leisure (”athleisure”) becomes trendy, more middle-class consumers are upgrading their choices in this category. The sports you practice now say a lot about your personality, taste, and social circles.

In fact, consumers are increasingly adding their own “aesthetic” preferences to professional running shoes and sportswear brands. On Chinese social media, you often see brands like On and Kolon linked with “old money” and athleisure styling—even in non-professional sports scenarios, urban elites are flocking to wear these brands for leisure and commuting.

Interestingly, the keyword “athleisure”—written in English—has been growing particularly fast on Chinese social media, especially Xiaohongshu (Red Note). This is no coincidence: China’s high-income urban elites, often internationally educated and English-proficient, are the leading group driving this lifestyle.

The big picture: spending by middle-class and affluent consumers is recovering

One telling piece of evidence that China’s affluent consumer base is spending again is the recovery of luxury sales since H2 last year. This recovery trend continued into January and February this year after the Chinese New Year.

According to our offline payment data, most luxury brands posted positive year-on-year growth in January-February, with sequential improvement from Q4.

But Ralph Lauren emerged as the biggest winner, with +88% growth (vs Q4 +47%), significantly outperforming other luxury houses—for instance: Hermès (+13%), Louis Vuitton (+2%), Gucci (-4%), YSL (-5%), Dior (+5%), and Prada Group (+3%).

This is no coincidence. For one, Ralph Lauren not only offers stronger sporty aesthetics and functional designs, but also uses more skin-friendly fabrics like cotton, making it a brand people genuinely choose to wear for actual exercise.

Brand Performance & Investment Implications

So what’s the takeaway for investors?

First, I believe there is a structural tailwind for sports and health in general, given the recovery of middle-class and affluent spending combined with the “athleisure” fashion trend.

This comes against the backdrop of major sporting events—the Winter Olympics and upcoming World Cup have sustained momentum in sports spending, especially Anta. As the official uniform provider for Chinese athletic teams, Anta has enjoyed significant brand exposure.

Domestic brands are already seeing accelerated growth. According to our online and offline tracking, Anta’s

full-channel sales improved significantly: +9% YoY in January-February 2026, a sharp turnaround from -7% in

Q4 and -10% in December 2025.

But I believe “athleisure” brands such as On, Lululemon, and Arc’teryx could enjoy even stronger growth.

The confluence of two factors creates a powerful tailwind. First, value-based premium is emerging—consumers are not just buying functional sportswear, they’re buying identity. Premium brands are likely to outperform. Second, usage scenarios are extending beyond “exercising” to “commuting,” “dating,” “working”—this means consumers buy more, buy more frequently.

The data support this.