China reality check after the DeepSeek rally - Charts of the Week

China's economy stabilizing and finding a bottom, for now

"Charts of the Week" is Baiguan's series that features key data points to help you quickly grasp the general state of affairs in China in just a few minutes. We handpick the highlights of the data charts from a variety of sources, analyzing and delivering insights trusted by 100+ top institutional and corporate clients worldwide at BigOne Lab. Don't forget to subscribe before you continue reading!

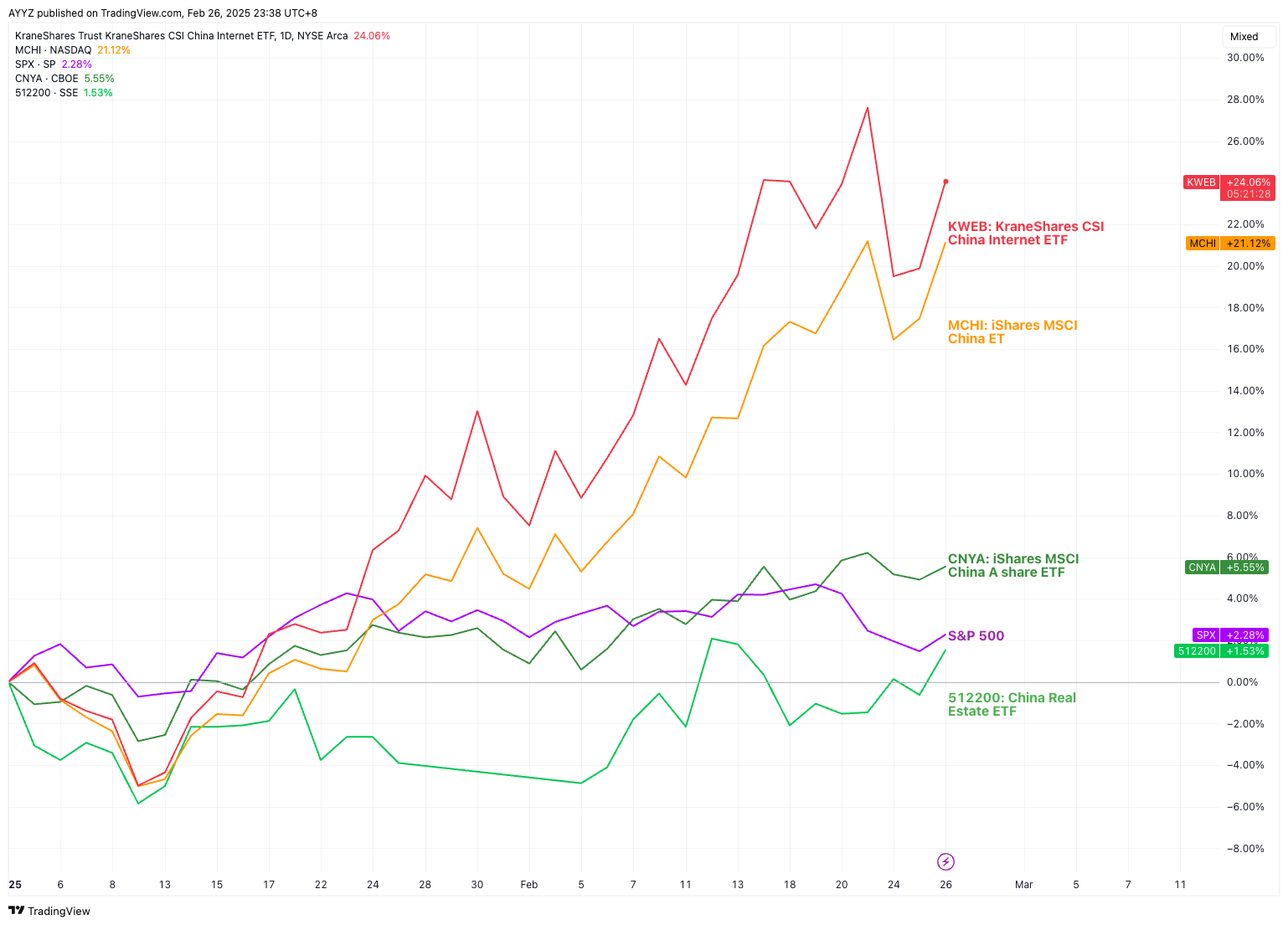

Since DeepSeek launched its ChatGPT-rivaling model and made global headlines in late January, Hang Seng has roared back with a 21% year-to-date gain. Much of this rally has been driven by tech giants, with the KraneShares ETF (KWEB), which tracks China’s internet sector and tech giants like Alibaba and Tencent, surging 24% YTD at the time of writing.

DeepSeek’s success, alongside other tech giants like Alibaba and ByteDance releasing their own large language models (LLMs), has reignited global interest in China’s tech sector. The country is now being seen as a competent competitor—and potentially a global leader—in the AI race.

However, the current rally is being fueled in part by “hot money.” While there’s no denying that investors are rushing in, driven by fear of missing out (FOMO) on China’s resurgence, the market remains highly volatile. Institutional money has yet to fully commit, and small sentiment shifts could trigger big profit-taking—as seen in the correction this past Monday, for instance.

Moreover, not all Chinese equities are enjoying the rally. For instance, CNYA, which tracks Chinese onshore A-shares (with less exposure to big tech), has returned a modest 5.5% YTD, compared to KWEB’s 23.9% surge. Meanwhile, the troubled real estate stocks have barely restored, underscoring the uneven nature of Chinese equities' rebound.

So, the natural question is: What will it take to sustain the rally for China’s equities, and could the DeepSeek craze finally lift broader Chinese assets?

We’re currently in what can be described as a “vacuum” period for China’s economy and markets. Policy announcements have been mostly muted ahead of the Two Sessions (which kick off next week), and macroeconomic data has been sparse as consumption and hiring activities slowed during the Spring Festival. This lull has left investors with limited signals to gauge the economy’s direction.

At the same time, the market is digesting the potential risks of renewed Trump-era tariffs. However, China’s strong export performance and its overseas expansion of manufacturing capacity have provided reasons for optimism. Many believe China is better positioned to adapt to external shocks than it was in 2018. So far, this vacuum window has been free of bad news, and the loudest voice seems to be the optimism surrounding China’s tech comeback. Tech disruptors cannot single-handedly drive the volume of job creation and consumption growth that China’s economy needs in the years to come. Ultimately, the success of China's planned shift to a domestic-consumption-driven model will hinge on real estate asset prices and household income expectations.

So, what's China's economy really been doing? Let’s do a reality check.

In today’s newsletter, I’ve handpicked a few key data points to update you on the latest developments in China’s macro environment—covering real estate, the job market, and consumption. These insights will help you gauge the current state of China’s economy amid the super bullish sentiment, enabling you to make informed decisions if you’re invested in broader Chinese equities.

In the coming weeks, we’ll also dive into specific industries and companies that we find compelling from an investment perspective. Stay tuned!

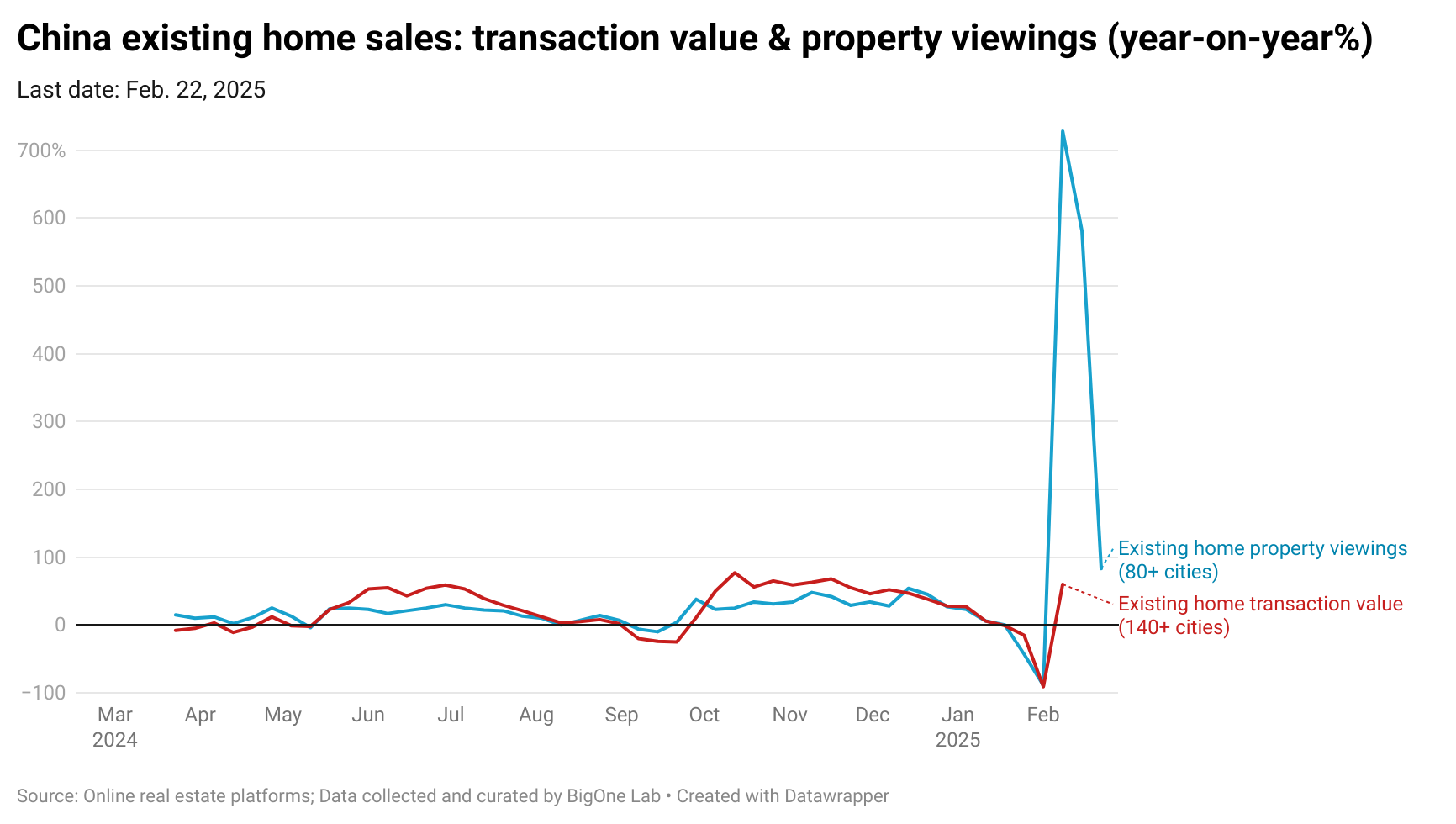

Real estate showing significant rebound of property viewings post Spring festival

Post Spring Festival, property viewing activities have surged triple digits year-on-year, signaling renewed interest in the real estate market. This uptick surpasses even the peak seen after the September 2024 stimulus package.

Core regions, especially first-tier and new first-tier cities such as Beijing, Shanghai, Guangzhou, Hangzhou, and Suzhou, are experiencing the strongest rebound in property viewing activities. This trend aligns with recent reports of China's state-owned developers purchasing land at premiums again, particularly in economically robust metropolitans such as Shanghai and Hangzhou.

However, transaction prices still show little sign of recovery. As recommended in my previous "Charts of the Week" post, it’s crucial to monitor policy developments during the "Two Sessions." If the real estate market continues to stabilize, additional stimulus packages may be less likely. However, any new policy announcements could serve as a game-changer and provide a positive surprise.

Continue to read updates on job markets and consumption. To get a sense of what is offered, you are welcome to check out this older post in the same series: Charts of the Week. You can also get free access by sharing us.