How big of a problem are tariffs for China's economy?

Initial thoughts on market sell-off and opportunities ahead

The recent global sell-off triggered by Trump's tariff policy, which went worse than many analysts' expectation has made me reminiscent of the circuit breaker of Nasdaq back in the March 2020. Only this time, it feels even worse.

At this point, there are still a lot of floating pieces and I think it's too soon to call it a dip. But I want to share some initial thoughts (along with charts) with you in today's newsletter. This is a somewhat meandering of my organic reasoning so far, and I welcome you to think out aloud with me and debate.

Time to fold the hand

I remember sitting on the trading floor in March 2020 when the Nasdaq circuit breaker was triggered. That crash was terrifying—you could hear the murmurs of fear in the air. But this recent sell-off feels even worse. And when you look at the data, it is worse—potentially more severe than the COVID crash and even comparable to the global financial crisis.

Market sentiment is in extreme fear. After back-to-back sell-offs on Thursday and Friday, the percentage of S&P 500 stocks trading above their 20-day average has dropped below levels seen during the financial crisis (though this could change after Monday’s open). This suggests broad-based selling pressure. Looking at the 200-day average, the current situation is also among the worst in decades, exceeded only during the financial crisis and the pandemic. If this isn’t just a short-term correction but part of a broader economic downcycle—which I believe it is, considering the looming U.S. recession and global decouple narrative still haven’t been fully priced in—then we may still have room from the bottom.

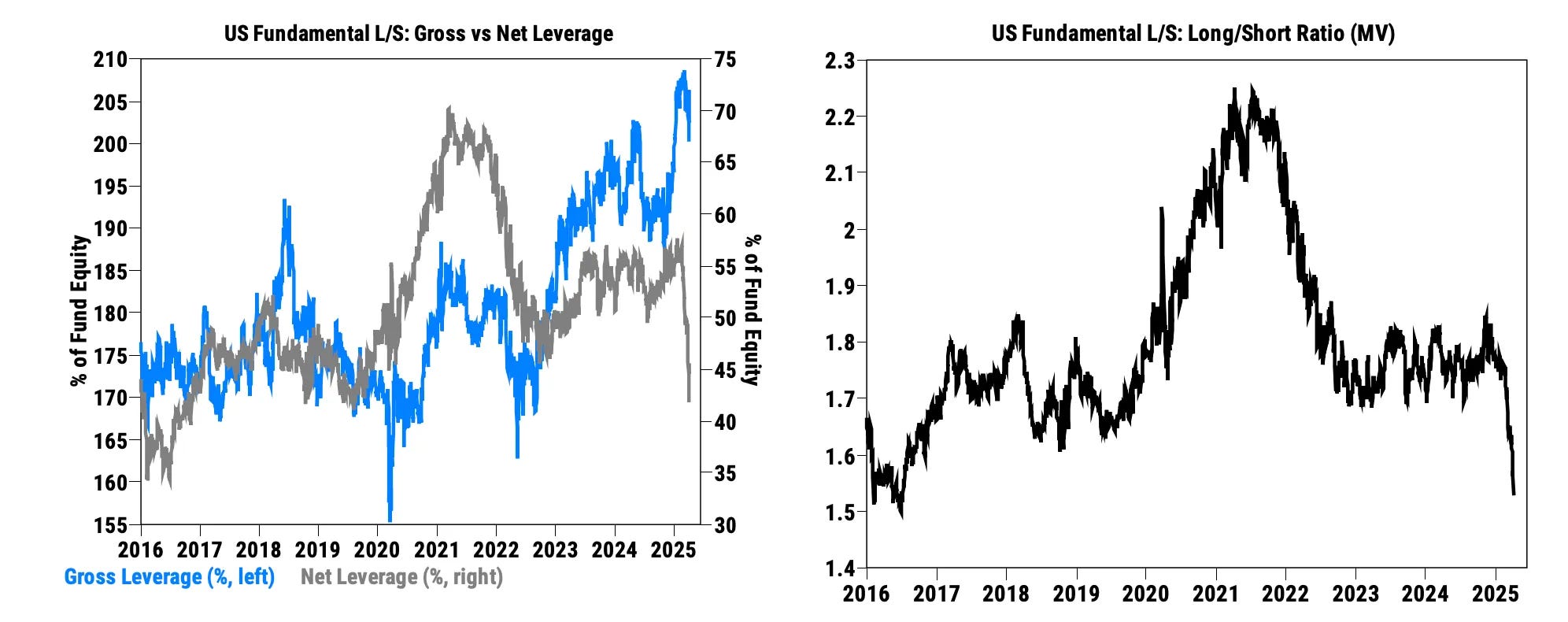

On the fund flow side, net leverage and long/short ratios among long/short funds have dropped to near 10-year lows. Clearly, we’re in full risk-off mode.

In China, we’ve witnessed historical declines too. ChiNext (-12.5%), CSI 500 (-9.55%), CSI 1000 (-11.39%), and CSI 2000 (-12.83%) all posted record single-day drops as the global sell-off spilled over.

What’s striking is how “orderly” this sell-off has been—at least so far. Unlike March 2020, where a lot of the fear came from panic sales and forced liquidation, this time the VIX closed around 45 on last Friday—elevated, but far from the >80 seen during the pandemic and the financial crisis. This suggests that fear is getting higher, but we haven’t yet seen full-blown panic; the sells are in order.

So why am I focusing so much on the U.S equities in a China-focused newsletter?

Because I don’t think this is just a short-term correction or another deepseek moment repricing of U.S. tech valuations. I believe we’re seeing something unprecedented in decades, comparable to financial crisis/COVID situations. In this context, “buying the dip” doesn’t offer an attractive risk-reward setup. Risks feel increasingly asymmetric.

While I told my readers I had taken profits on Chinese names—given that tech valuations looked fair—I personally held on to some U.S. and European positions as of last Friday, partly out of wishful thinking. In hindsight, that wasn’t the most rational move. There could still be policy reversals or tariff negotiations, but those are beyond my ability to forecast. (And again, the asymmetrical risks aren’t just worth it)

Take the profits if you have them. And even if you’re not in the green, folding your hand may be the wiser choice. It’s too early to confidently call a bottom—and even if we are close, I don’t expect a sharp V-shaped rebound or major FOMO opportunities in the short term.

Because I think we may not just witness the end of a bull run—but the end of the globalization era. (Well, it’s impossible for the world to fully disconnect and return to pre-WWII conditions; but you get the idea—the landscape will be drastically different.)

Buckle up.

Where are China's opportunities?

Back to Baiguan’s core focus: Chinese equities.