Is delivery war drawing to an end?

A data-driven look looking at top tea and coffee chains

On April 1, we officially launched Baiguan Pro, our professional-tier subscription designed for investors seeking deeper, more specific coverage of Chinese equities. Baiguan Pro delivers the Baiguan team’s monthly outlook on overall Chinese equity assets, our quarterly focus on themes and sectors, richer company-level analysis, and follow-ups on the ideas and companies previously presented in the newsletter.

If you missed our launch piece, you can read it:

As a reminder, existing paid subscribers can claim a complimentary upgrade to Baiguan Pro as of now by simply replying to this email.

Is the delivery war drawing to an end?

From 2025 to the present, China’s on-demand delivery market has been shaped by an intense subsidy battle—primarily between Meituan and Alibaba’s Taobao Flash Purchase (淘宝闪购). By using proprietary data on top 5 tea and coffee brands from BigOne Lab, Baiguan’s data analytics arm, this analysis examines how the dynamics of the “third-party delivery” (3PD) market are shifting, and why the war appears to be drawing to a close.

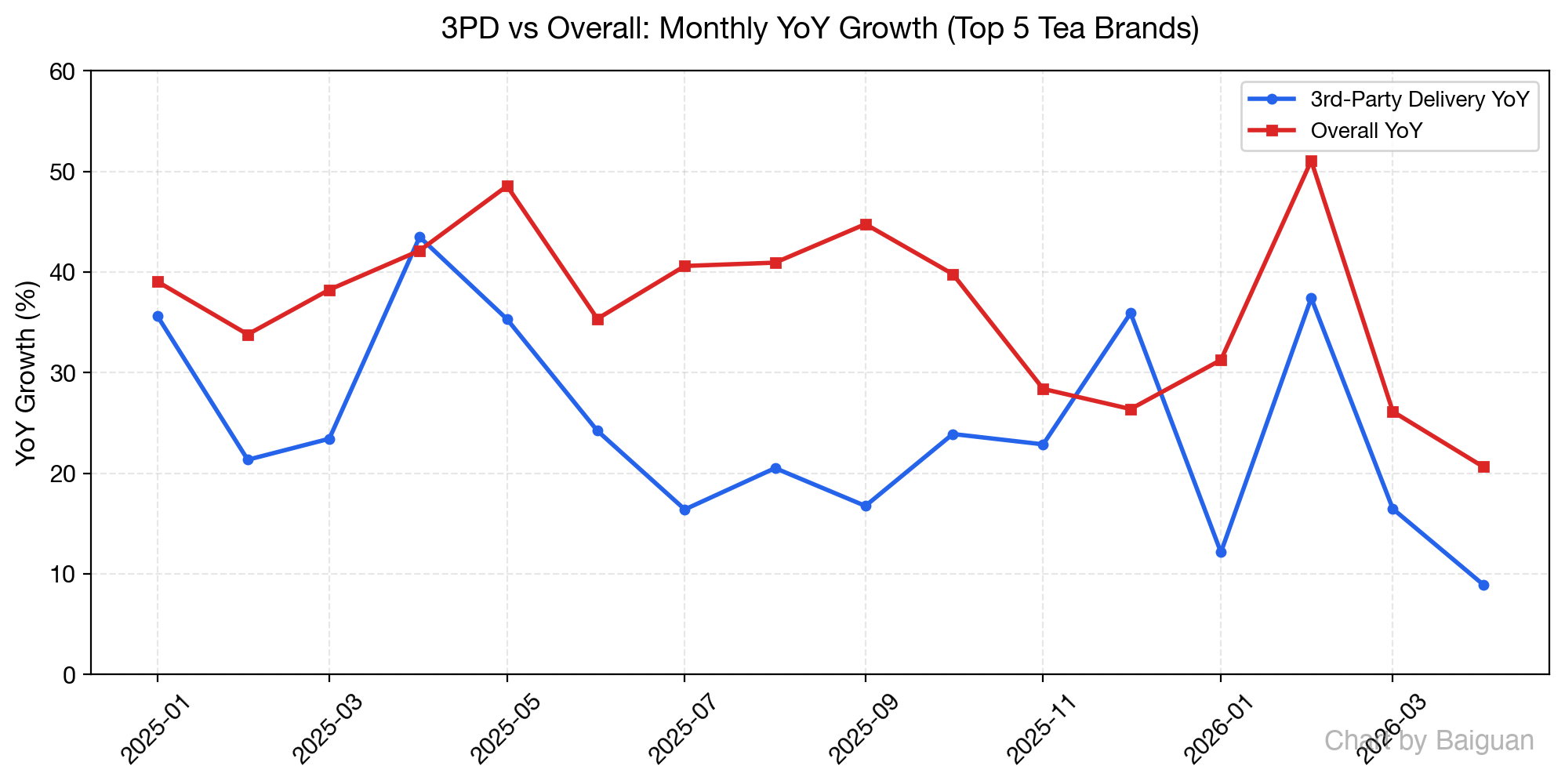

1. 3PD Growth Still Outpaces Overall—But the Gap Is Narrowing

The five brands we have chosen for this analysis are Luckin Coffee, Mixue, Guming, Starbucks, and Chagee.

From January 2025 to April 2026, the five brands’ 3PD channel YoY growth consistently outperformed their overall brand growth, proving that subsidized delivery has been a key growth engine.

However, the gap peaked during the peak subsidy months of June through September 2025 and has since been steadily narrowing. By early 2026, the gap between 3PD and overall growth rates had narrowed significantly, suggesting that the subsidy-driven boost was fading.