A Note From Baiguan

On April 1, we officially launched Baiguan Pro, our professional-tier subscription designed for investors seeking deeper, more specific coverage of Chinese equities. Baiguan Pro delivers the Baiguan team’s monthly outlook on overall Chinese equity assets, our quarterly focus on themes and sectors, richer company-level analysis, and follow-ups on the ideas and companies previously presented in the newsletter.

If you missed our launch piece, you can read it:

As a thank-you to our existing paid subscribers, we are offering a complimentary upgrade to Baiguan Pro (offer ends on June 30, 2026). If you’d like to take us up on that, simply reply to this email — we’ll get you sorted.

In Today’s Data Update

We are updating four sectors that we recently wrote about in the Baiguan newsletter, with BigOne Lab’s proprietary data as of March 2026:

Sportswear & Footwear: We previously highlighted how the rise of the “athleisure” trend and robust discretionary spending on sports and health in China are driving organic growth.

Luxury Goods — We previously noted that luxury goods are seeing a gradual comeback in China as sentiment improves among middle-class and affluent consumers. In particular, Laopu Gold and the broader gold jewelry sector deserve close attention.

Pop Mart — We previously detailed why we believe the IP sector is one of the best business segments in China and discussed Pop Mart’s valuation.

At BigOne Lab, we curate data highlights, analyze them, and deliver insights trusted by 100+ top institutional and corporate clients worldwide.

🔒 The following content is available to Baiguan Pro subscribers.

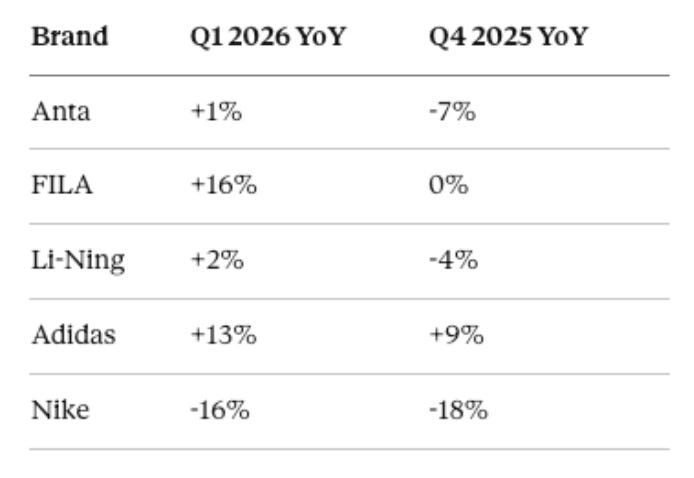

1. Sportswear & Footwear | March 2026

Bottom line: March growth moderated from the elevated January–February base, but Q1 as a whole delivered meaningful sequential acceleration versus Q4 — particularly for integrated brands and running shoes.

January–February’s strong performance was shaped by a confluence of one-offs: delayed winter demand from a warm December, the Chinese New Year week pull-forward, and Winter Olympics-related brand exposure. As those tailwinds faded, March growth naturally cooled. But stepping back to Q1 as a whole, the sequential improvement over Q4 is real across the board:

FILA’s acceleration to +16% is the standout. Nike remains the outlier — Q1’s -16% shows no meaningful improvement over Q4’s -18%, consistent with continued weakness at the distributor and retail level.

Performance Apparel: Divergence Opening Up

March brought a visible slowdown for Amer Sports: +20% YoY, down from +29% in January–February, with Q1 at +27% versus Q4’s +37%. Descente (+29% in March, broadly in line with Q4’s +31%) and Lululemon (+22%, versus Q4’s +26%) are both holding pace well.

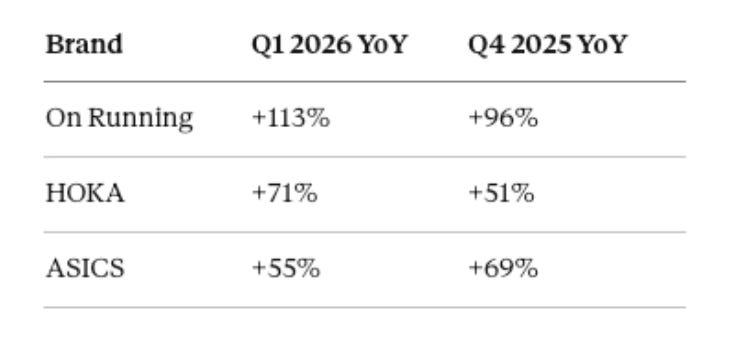

Running Shoes: The Standout Growth Story

Running shoes remain the cleanest high-conviction trend in our sportswear data. Despite a modest March moderation, Q1 figures are striking:

On Running and HOKA both accelerated in Q1 — this is not a base-effect story, it reflects genuine share gains in a Chinese running shoe market that continues to trade up.