Today, we're sharing an enlightening article that delves into the profound challenges of China's pharmaceutical sector—challenges that run deeper than those faced by other US-targeted industries like semiconductors, yet often overlooked by investors and policymakers. The article prompts us to consider:

What stage of development is China's pharmaceutical industry currently in?

Why have top policymakers overlooked the severe export deficit issue in China's pharmaceutical industry?

How should policymakers reform the system to reconcile the mutual restrictions between public welfare and market ability, address slow and cumbersome internal government decision-making, and move away from a one-size-fits-all policy and approval process?

IMPORTANT Community Announcement

We are planning to launch a paying member-only online community for you to exchange ideas. We have yet to decide on details, but very likely it will be a Discord community. We welcome other suggestions from you.

Starting from July 15, we will increase our subscription price from $100/year to $188/year, $15/month to $20/month. Prices will NOT increase for paying subscribers who sign up by July 15th, so please subscribe before then to lock in the old price.

Paying members of Baiguan enjoy free access to China Translated, the personal newsletter of Robert Wu, which is currently worth $100/year. Please DM us if you wish for this access.

Below is Baiguan's translation of the original article (some paragraphs are abbreviated or redacted) from the public WeChat account Yi Luo "伊洛" known for its in-depth analysis and comprehensive coverage of the pharmaceutical sector, including new drug discoveries, industry policies, market dynamics, and technological advancements.

On June 6, the primary pharmaceutical producers and consumers—namely the US, Europe, Japan, and India—announced the formation of the "Biopharma Alliance" in the United States. This move comes in the wake of overt suppression policies targeting leading Chinese pharmaceutical firms, coupled with substantial and long-standing invisible trade barriers. Consequently, an "iron curtain" appears to be forming across the biopharmaceutical landscape of Eurasia.

Behind this metaphorical iron curtain sit the capitals of almost all major biopharma nations—Seoul, Tokyo, Berlin, Paris, and New Delhi. These renowned cities, along with their surrounding populations, are firmly within the American sphere of influence. This dominance not only brings them under Washington's control through the attraction of the world's largest pharmaceutical market but also integrates them into America's strategic economic policies.

The biopharmaceutical sector in China faces geopolitical pressures worse than semiconductors

The United States employs almost every tool short of hot war to weaken various Chinese industries. Sanctions lists, tariffs, targeted corporate attacks, and regional cooperation bans have become commonplace. Examples include comprehensive sanctions on Huawei, industry-wide sanctions in the semiconductor field, and discriminatory tariffs in sectors like new energy vehicles and photovoltaics.

Industries across these sectors face considerable pressure and challenges, meriting attention and countermeasures. However, their situation is still more favorable compared to the biopharmaceutical sector. Photovoltaics and new energy vehicles have unparalleled competitiveness globally and are supported by the world's largest domestic market. The United States' "small yard, high fence" strategy, akin to a self-damaging punch, struggles to attract followers, leaving the ultimate outcome uncertain.

The semiconductor industry, despite facing severe risks, benefits from high national priority, robust capital support, a self-sufficient defense sector, and substantial demand, all of which provide avenues to mitigate difficulties. Last year's release of Huawei's Mate 60 symbolized a milestone in achieving phased self-reliance.

China's biopharmaceutical industry operates in the shadows, yet huge trade deficits reveal its fragile supply chain

The pharmaceutical industry, characterized by stringent regulations in the US and Europe and extensive government and insurance funding, confronts significant non-tariff barriers in market entry, reimbursement, and institutional adoption.

The industry is segmented into numerous therapeutic areas with long investment cycles and substantial capital requirements. The economies of scale are essential for absorbing clinical, promotional, and lobbying costs. Consequently, smaller firms often get acquired by established giants, who dominate clinical trials, market access, and government relations, maintaining a stable, almost unassailable position.

These inherent characteristics and invisible barriers mean that even as "Made in China" products surge globally, China's market share in pharmaceuticals does not match its manufacturing and R&D capabilities.

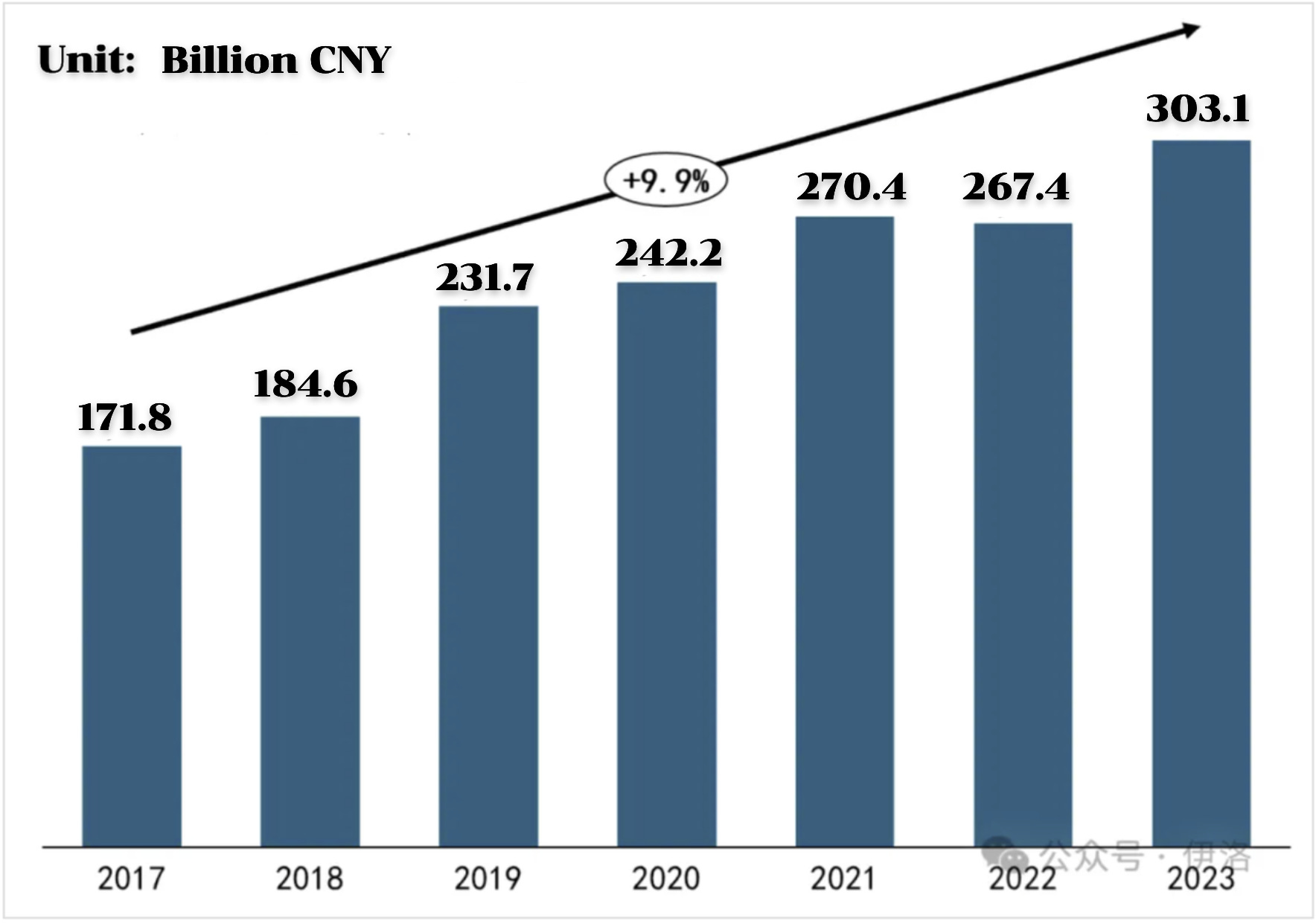

According to 2023 customs data, excluding resources like oil, gas, and metals, pharmaceuticals represent the largest trade deficit in industrial products, with a total amount exceeding 200 billion CNY (≈27.89 billion USD). Exports have contracted sharply, while imports continue to grow rapidly.

China's substantial overall trade surplus conceals a critical issue in the pharmaceutical sector, where the trade deficit leads to significant financial outflows. This might not be a major concern under normal circumstances, but if overseas supply chains were suddenly disrupted for any reason, the situation would become dire. Considering the lengthy R&D cycles and the stringent, prolonged domestic approval processes, does China have a contingency plan to quickly address a shortfall of over 360 billion CNY (≈54 billion USD)in imports? Can patients afford to wait?

Hidden barriers and sanctions abroad threaten high-quality firms

The pharmaceutical industry is already in a vulnerable catch-up phase, and current geopolitical tensions exacerbate this scrutiny. Recent events suggest an acceleration of this process.

In the few areas where China has a competitive edge, decisive action is imperative. For instance, in the efficiency-driven R&D CRO and production outsourcing CDMO sectors, domestic engineers' advantages have provided stability and high efficiency. Companies like WuXi AppTec (2359. HK) have thrived, especially during the pandemic, gaining market share and competitive edge.

However, unfounded accusations have emerged. Since late last year, US legislators have proposed restrictions on Chinese CRO/CDMO firms like WuXi AppTec, citing "genetic" biosecurity concerns.

Jiangsu-based GenScript (1548. HK), a leader in cell therapy and CDMO, developed a BCMA CAR-T therapy for multiple myeloma in collaboration with Johnson & Johnson, achieving over $1 billion in sales. Despite being one of the most successful global cell therapy firms, it was named for investigation in late May, causing a 17.7% stock drop. Sadly, this leading therapy is yet to be available in China, let alone rely on the domestic market to counter potential sanctions.

In May, tariffs were imposed on certain medical devices. Despite past contributions to the US pandemic response, companies like A-share listed Caina Technology (301122. SZ) received import warnings in April, halting imports.

An alarming oversight: unrecognized perils looming in the industry

As the largest pharmaceutical market, the US's direct suppression of leading companies in various fields imposes significant operational pressures on China's biopharma industry, potentially driving out top companies and talent.

Hidden barriers also pose serious challenges. In 2023 alone, 865 batches of Chinese medical products were rejected by the US FDA due to compliance issues, including 187 pharmaceutical batches and 678 medical device batches, representing 12.6% of all US FDA rejections. This has resulted in severe economic losses for Chinese pharmaceutical exporters.

Currently, there seem to be no visible countermeasures to support domestic companies against these challenges, though some private support may exist.

During the pandemic, the fragmented global supply chain and unprecedented focus on healthcare, combined with the Federal Reserve's massive liquidity injections, briefly boosted domestic pharmaceutical R&D. However, pharmaceuticals are a long-cycle industry, and short-term indicators like new drug output don't fully capture the negative impact of contractionary policies.

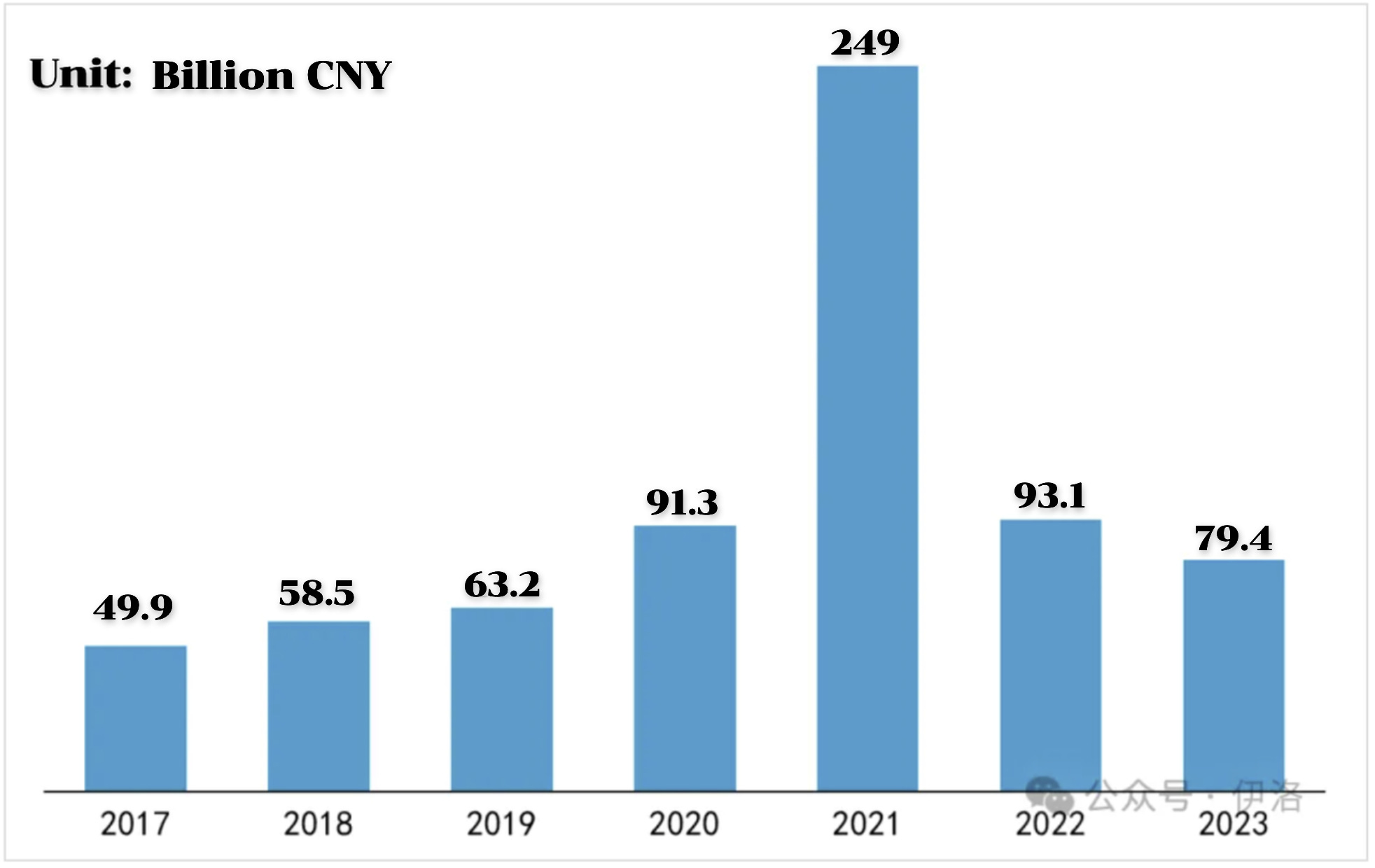

The macroeconomic climate has cooled since late 2021, intensifying competition and reducing pandemic-related demand, leading to rapid export contractions. In 2021, vaccine and COVID-19 drug manufacturing boosted pharmaceutical exports to $38.5 billion. This fell to $14 billion in 2022 and further to $11.3 billion in 2023.

Conversely, imports continue to grow significantly, making pharmaceuticals one of the few sectors with a widening trade deficit each year, reflecting potential biases in domestic industrial policies.

Current pharmaceutical policies, from evaluation to market entry, fail to account for the pressures of great power competition and the industry's fragile foundation. Overemphasis on "livelihood" benefits without considering the sustainable development of pharmaceutical R&D and manufacturing companies, rigid review timelines, non-differentiated volume-based procurement policies(*) encouraging the lowest prices, and pushing for globally lowest-cost innovative drugs suppress the future R&D space and dampen investment incentives.

[*Baiguan Note: China's volume-based medicine procurement program is a government-led initiative that centralizes the buying of drugs to negotiate lower prices through bulk purchases, making essential medications more affordable for the public as part of broader healthcare reforms.]

Facing such internal and external challenges, the biopharmaceutical industry is in a precarious position. It is crucial for domestic policy to adopt a wartime economic mindset to navigate these turbulent waters.

China's embattled pharmaceutical sector must urgently reinforce and optimize industry policies

Relying heavily on the US market while being in a catch-up phase, Chinese pharmaceutical companies face enormous pressure, especially when the domestic market fails to provide robust support. The only viable solution is to expand the domestic market, creating a virtuous cycle of investment, R&D, and commercialization, thereby enhancing industrial competitiveness.

Securing the pharmaceutical supply chain should be a national security priority—an immediate comprehensive review is needed

Ensuring supply chain security is crucial, significantly encouraging both domestic and foreign pharmaceutical companies to relocate production to China. As Western nations accelerate de-globalization, China's dependency on over 300 billion CNY (≈42 billion USD) worth of annual pharmaceutical imports becomes increasingly fragile.

The National Medical Products Administration (NMPA) must adopt a more pragmatic approach. Historically, its rigorous requirements for transitioning imports to local production, such as comprehensive technical documentation from raw material suppliers, have discouraged many foreign suppliers. The extensive investment, uncertain prospects, long timelines, and high technical demands have deterred both domestic and international companies from relocating production to China, thereby reinforcing dependence on overseas supply chains.

In response to industry demands, April 2024 saw the release of Measures to Optimize the Registration Process for Transitioning Imported Drugs to Domestic Production. While these marks progress, it remains insufficient.

For instance, the insistence on identical processes overlooks practical challenges. For older products, adapting to domestic production lines can be costly and impractical, requiring significant investments to achieve compliance. This focus on textual compliance over practical considerations of safety, stability, and quality control imposes substantial uncertainty on corporate investments.

The NMPA should receive higher-level support, including increased central budget allocations, to expand the review team and provide reviewers with greater flexibility. Responsibility should be shifted more towards the companies, with a focus on scientific and professional evaluations, enhancing post-approval accountability rather than rigid pre-approval procedures that currently cause significant delays.

For companies transitioning imported products to local production, central fiscal support should be considered. This not only enhances supply chain security but also boosts domestic pharmaceutical manufacturing capacity, presenting a win-win scenario. Given the substantial investments and efforts required, there should be significant positive incentives.

Substantial reforms to volume-based procurement policies are crucial to preserve domestic firms' cash flow and enable industry upgrades

Since the inception of the volume-based procurement (VBP) policy in late 2018, nine batches have been conducted, covering over 1,600 products. While VBP has significantly reduced the prices of original drugs, creating "patent cliffs" with lower prices and volumes, it also carries risks if overdone.

From a macro perspective, why haven't import drug costs decreased significantly? This may be because many imported products are still sold at high prices in retail markets, while extremely low prices for domestic products (some as low as a few cents per unit) undermine confidence in their quality. VBP's low-price competition could lead to industry concentration decline and future quality risks.

The foundation of VBP lies in adherence to quality and standards of domestic products. It is hard to imagine foreign enterprises in niche markets, like Da Vinci surgical robots, responding to price cuts as aggressively as they did in the coronary stent segment.

In the high-value medical device sector, domestic companies face substantial hurdles in competing with foreign brands due to brand loyalty and procedural familiarity. These companies require prolonged efforts and substantial financial backing to support R&D. Post-VBP, the multi-billion yuan coronary stent market shrunk dramatically to approximately 1 billion CNY(≈140 million USD). For global giants like Boston Scientific and Medtronic, with diverse product lines and limited reliance on the Chinese market, such changes are manageable. However, for domestic firms with narrower product lines and still in their growth phase, this poses existential threats, which could indirectly affect other sectors and increase the burden on the national healthcare budget.

In areas with high domestic substitution, is it necessary to prioritize low prices exclusively? Revenues generated by domestic companies are reinvested into R&D, production, hiring, and taxes, contributing to the domestic economic cycle. Gradual price reductions, along with increasing household incomes to proportionally reduce the impact of high-value medical consumables on residents, might be a more sustainable approach.

Policy Recommendations:

In areas where domestic products hold a dominant market share, exceeding 50% (implying major profits are retained domestically, benefiting shareholders, employees, and suppliers), and in sectors where the total medication expenditure is relatively low (under 140 million USD annually, meaning the overall societal burden is manageable), it would be beneficial to temporarily halt centralized procurement in these fields. This can provide domestic pharmaceutical companies with much-needed respite and additional capital to invest in R&D.

Furthermore, in therapeutic areas where daily medication costs are already below 5 CNY (indicating a lighter financial burden on patients), delaying centralized procurement could allow the industry to transition more smoothly. Such measures would immediately enhance valuations in the capital market, improving the investment outlook for the domestic pharmaceutical industry.

National medical insurance catalog negotiations should embrace the art of 'making a fervent quest for talent' to leverage more social investment

As Bi Jingquan stated: "The pricing mechanism for innovative drugs is crucial to the survival of China's biopharma industry. New drug R&D is highly challenging, lengthy, costly, and fraught with a high failure rate. It is a high-risk investment in high-difficulty innovation. Such high-risk investments should be allowed high returns. Only then can we attract scientists to engage in fundamental innovation and investors to support the biopharma sector. High pricing is the best incentive."

Without rapid domestic R&D progress in areas like PD-1 cancer treatments and rare diseases, it is hard to imagine global pharma giants setting lower prices for their monopolistic therapies in China.

Policy Recommendations:

Currently, the industry is experiencing low investment and financing activity. For high-quality products, we should make a fervent quest for talent, granting them higher nominal pricing. High nominal pricing allows the healthcare management to negotiate with companies to re-price once a certain total expenditure is reached. This ensures limited total spending but significantly boosts capital market expectations, industry morale, and long-term investment in innovation.

Some provinces experiencing net population outflow face greater pressure on healthcare funds, lacking national coordination. This sensitivity to pricing and delays in listing products post-negotiation are key issues. Central government should consider establishing a livelihood support fund to aid innovative drug and device payments in central and western provinces. The revenue from domestic enterprises can then be reinvested in early-stage R&D, clinical trials and training, factory construction, salaries, taxes, dividends, and venture reinvestment, all contributing to the domestic economic cycle and promoting innovation.

My take

The article I read filled me with a sense of urgency. China's pharmaceutical industry is in a period of dual crises—external suppression led by the United States and an over-reliance on foreign industrial chains, coupled with internal dilemmas. Healthcare, inherently a public service and a critical livelihood issue, is naturally characterized by inclusiveness rather than commercialism. Yet, market competition and ample capital are essential to foster higher quality products and services, driving long-term technological advancement.

The author urgently calls attention to the fact that China's healthcare industry is at a crossroads, with policy being the critical issue. On one side, policies could encourage industry incentives, talent, innovation, and healthy development. On the other, tight policies could lead to talent loss, technological stagnation, continued reliance on imports, and being constrained by high-priced foreign innovations. Policy has always been a crucial driving force for China's industrial and economic development. Sectors like new energy vehicles, photovoltaics, and telecommunications have gained global competitiveness through policy support. However, the dilemma in the pharmaceutical industry lies in the mutual restriction between public welfare and marketability.

Therefore, first, more flexible policy formulation and sophisticated policy executors are needed. The article points out that many issues arise from one-size-fits-all policies or lengthy and rigid approval processes, requiring more fundamental or systemic improvements, not limited to the pharmaceutical industry. Second, there needs to be a focus on incentives for local governments, especially given local government debt issues and tight fiscal revenues. The central government needs to step in.

Additionally, despite breakthroughs in China's pharmaceutical industry, these benefits are not evenly distributed among all citizens. The inequitable distribution of medical resources underscores the necessity for a tiered medical system designed to meet the needs of China's diverse and widespread population. This disparity was brought into sharp relief for me during the recent Spring Festival, as I experienced firsthand the contrasting standards of urban and rural healthcare when an elderly family member contracted COVID-19.

I had no idea there was such a large trade gap between China and the US for pharmaceuticals. It's funny because when the COVID crisis started there was urgency in the US to de-risk pharmaceutical supply chains from China. Are there any other big high-level industries where the China-US trade gap is this large?