China’s AI Bubble Checkup, CXMT’s IPO, and Beijing’s Market Calculus

This is a follow-up to our earlier Baiguan Pro note tracking the A-share AI boom.

A Note From Baiguan

On April 1, we officially launched Baiguan Pro, our professional-tier subscription designed for investors seeking deeper, more specific coverage of Chinese equities. Baiguan Pro delivers the Baiguan team’s monthly outlook on overall Chinese equity assets, our quarterly focus on themes and sectors, richer company-level analysis, and follow-ups on the ideas and companies previously presented in the newsletter.

As a reminder, existing paid subscribers can claim a complimentary upgrade to Baiguan Pro (offer runs through July 31, 2026) by simply replying to this email.

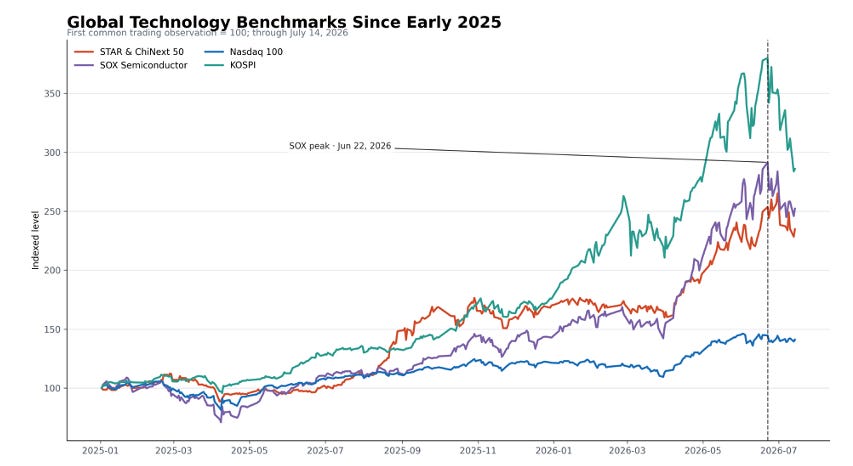

When we last took stock of the bubble cycle in early June, Chinese technology shares were still racing higher. What followed was a violent round trip: one final surge, then a sharp reversal across the sector. The global technology trade was increasingly moving in the same direction, but China’s market still carried its own distinctly Chinese characteristics.

Note: All four indices are rebased to 100 at their first common trading observation in 2025. The vertical line marks the SOX peak on June 22, 2026. Data run through July 14, 2026.

The move told us two things. First, in the final stage of the upswing, the rally had started to move well beyond companies with visible earnings. Second, when the selloff began, some parts of the AI trade proved more resilient than others.

Semiconductor equipment, materials and broader semiconductor self-reliance themes, excluding memory, became the last leg of the rally. The rally moved beyond optical modules and memory, where profits were already visible, into areas where Chinese investors were pricing in outcomes much further in the future.

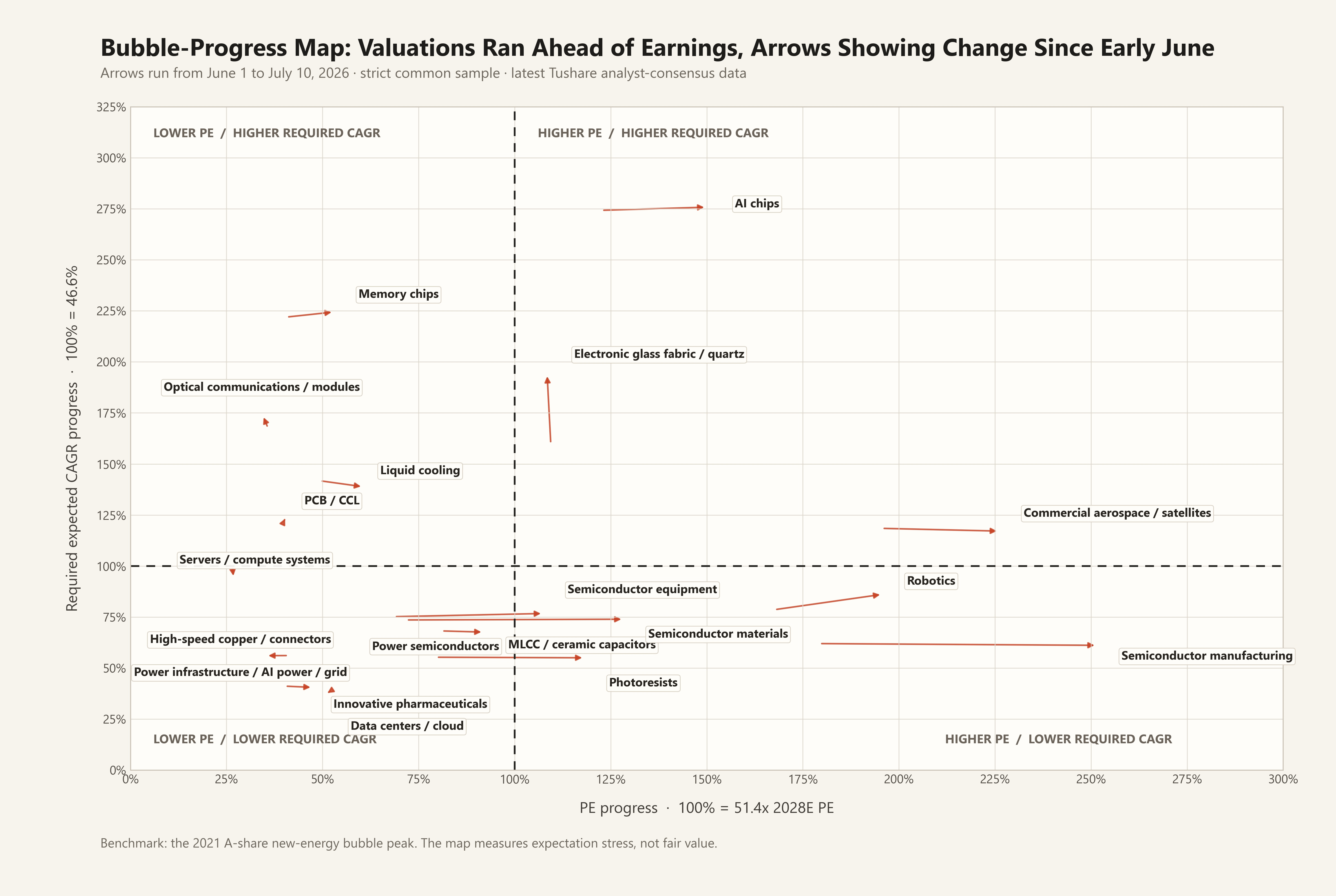

We can use the same bubble-progress framework again to see what changed over the past month.

Arrows run from June 1 to July 10, 2026 and use a strict common sample. The clearest valuation expansion occurred in semiconductor equipment, materials and manufacturing, even though their required earnings-growth assumptions changed little.

The framework is deliberately simple. We use the peak of the 2021 A-share new-energy bubble as a stress benchmark. At that peak, a representative basket of new-energy leaders implied a 46.6% expected earnings CAGR from 2021 to 2023 and still traded at 51.4 times expected 2023 earnings. We set each of those readings to 100%.

The themes we track, most of them centered on AI and technology, are plotted against the same two yardsticks. The horizontal axis is current 2028E PE divided by 51.4 times; the vertical axis is the expected profit CAGR required from 2025A to 2028E divided by 46.6%. Moving right means valuations are more stretched. Moving up means more earnings growth must still arrive. Each arrow shows how a theme moved between June 1 and July 10, 2026. The map measures how much expectation stress Chinese investors are pricing in relative to a previous A-share extreme.

The upper-left quadrant: profit leaders

Optical modules and memory remain in the upper-left quadrant. The themes in this quadrant carry expected profit growth above the peak of the previous bubble, but their forward PE multiples would be relatively moderate if that growth is delivered. They include some of China’s most profitable technology companies and some of the clearest beneficiaries of the AI infrastructure buildout. They were also the focus of our previous article. Memory, in particular, has become the market’s immediate focus and one of the core engines of the broader AI boom.

The 2026 H1 financial reports have yet to be published, so most analysts have not marked up their 2028 forecasts. Two domestic memory companies, however, have already released H1 earnings forecasts. If their first-half profit run rates are annualized, their 2026 net profits alone, even assuming no further growth, would already exceed analysts’ previous consensus forecasts for 2028 net profit.

The harder question has not changed: is memory still a cyclical industry, or is AI demand turning it into something closer to a growth business over a much longer time horizon?

That is now one of the central debates in global markets, and Chinese investors do not have a definitive answer. Memory scarcity has produced extraordinary margins, but it has also invited resistance from customers, including Apple and the major cloud service providers.

Those arguments are already familiar. Two less familiar perspectives are shaping the debate inside China.

The first comes from politics. Some Chinese investors believe the U.S. will not accept Korean memory suppliers capturing the largest share of the profit pool across the AI value chain indefinitely. It is a political-economy lens: markets do not operate in isolation from politics, and political power can reshape how value is divided across a strategic supply chain. That assumption no longer feels far-fetched. In the Trump era, the U.S. administration has shown a willingness to defend domestic interests through direct and highly visible intervention.

Though the recent KOSPI drawdown more likely reflects deleveraging, that is also a pattern Chinese investors know well: even when the fundamental story is intact, deleveraging can turn a crowded trade into a forced unwind, as it did during the 2015 A-share selloff.

The second perspective concerns the expected listing of ChangXin Memory Technologies, or CXMT.

The A-share market has never had a true heavyweight memory producer. That makes the prospect of a CXMT listing both exciting and unsettling. The excitement is straightforward: Chinese investors would finally gain access to a company that matters to the industry’s core economics, rather than having to express the memory cycle through peripheral proxies. Many of those proxies are module makers whose profits owe as much to inventory appreciation as to durable competitive advantage. Techwinsemi is a typical example. It is also one of the constituents in our memory-theme tracker. By July 14, it had fallen 24.1% from its own June 29 high, far more than the 11.5% drawdown in the STAR & ChiNext 50.

Source: CXMT IPO prospectus; Futu OpenAPI financial statements for Micron and SK hynix; cross-checked against Wind Financial Data Service. All figures refer to a single reported quarter closest to March 31, 2026. CXMT: Q1 2026 net profit attributable to owners; SK hynix: Q1 2026 net profit attributable to parent shareholders; Micron: fiscal Q2 2026 GAAP net income attributable to parent shareholders for the quarter ended February 26. Values are shown in USD; CXMT is converted from RMB at RMB 6.77 per USD. Reporting periods and accounting standards differ, so the comparison should be read as an indication of scale rather than a precise like-for-like ranking.

The anxiety is about liquidity. A listing of this size could absorb a meaningful amount of capital. It also touches an old scar: PetroChina’s 2007 debut, which arrived near the peak of that market cycle and became a lasting symbol of what can happen when an industry giant lists at the wrong moment. Chinese investors tend to be wary when a national champion comes to market amid already elevated expectations.

A second anxiety is valuation. CXMT’s official IPO pricing implies an equity value of roughly RMB 579 billion, but Chinese investors widely expect a much higher valuation once the stock begins trading, because A-share IPOs are typically issued at a discount to the price investors hope the secondary market will pay. RMB 3 trillion has become a shorthand for the bull case. If CXMT’s annual profit is roughly RMB 100 billion, that bull case would imply close to 30 times earnings. SK Hynix, by contrast, still trades at a single-digit forward earnings multiple despite being one of the global leaders in memory. That creates an implicit ceiling: Chinese investors want to price CXMT as a scarce national champion, while global memory comparables still impose valuation discipline.

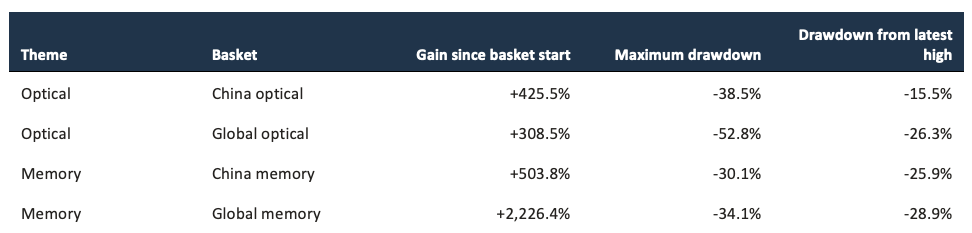

Let us look more closely at the upper-left quadrant. A deeper dive shows that optical modules and memory have behaved quite differently in the Chinese market. China’s memory trade still takes much of its direction from overseas markets, while optical modules have developed greater independence.

China’s A-share optical companies are globally significant in their own right. Zhongji Innolight, Eoptolink and TFC Communication sit at the centre of the global AI interconnect buildout. Their share-price behavior has consequently developed a degree of independence from overseas optical peers, and they proved more resilient when the broader technology trade reversed.

The difference becomes clearer when the Chinese baskets are compared directly with their global peers. China’s optical module basket looks more independent: it gained more than the global basket and gave back substantially less from both its worst drawdown and its latest high. Memory tells a different story. The global producer basket delivered much stronger upside, while Chinese memory did not show superior resilience on drawdown.

Dynamic equal-weight baskets are rebased to 100 at their first available value. SanDisk enters from February 13, 2025; Kioxia enters from January 6, 2025. Data run through July 14, 2026.

The broader validation points in the same direction. Daily correlation between the Chinese and global optical baskets was only 0.16. For memory, correlation rose to 0.43. Optical modules are not fully detached from global markets, but their domestic price formation has been meaningfully more independent.

That relative resilience of the first-quadrant players, supported by earnings prospects, helps explain why many Chinese investors still expect optical modules, and to a lesser extent memory, to lead any credible rebound. Both corrected sharply, but neither has lost its claim to earnings leadership. Our bubble-progress monitor will keep tracking these companies as a priority.

Profit support is not the same as bottleneck power

Not all upper-left themes deserve the same priority, however. Most of them are parts of the AI supply chain and have genuine earnings support. PCB and liquid cooling are obvious examples. They sit in the upper-left quadrant: earnings expectations are demanding, but forward valuations remain relatively moderate if those profits are delivered.

But profit growth alone does not necessarily create bottleneck power: the ability to sit at the point in a supply chain where profits and value tend to concentrate. GPU, the first major bottleneck in the AI buildout, drove Nvidia’s extraordinary re-rating. Scarcity then shifted toward memory. In both cases, a handful of companies controlled the essential technology and capacity, while new supply took time to arrive.

PCB and liquid cooling do not have the same structure. Capacity was not fundamentally scarce before the boom, expansion is easier, and credible suppliers are numerous. Chinese companies already hold meaningful market share, and their ability to add capacity quickly is hardly in doubt. The same demand surge can therefore produce strong earnings without producing durable scarcity rents. That can restrain the room for further valuation expansion.