China macro: is the strong Jan & Feb data organic?

Real estate, salary growth, early 2026 economic signals

“Charts of the Week” is Baiguan’s series that features key data points to help you quickly grasp the general state of affairs in China in just a few minutes. We handpick the highlights of the data charts from a variety of sources, analyzing and delivering insights trusted by 100+ top institutional and corporate clients worldwide at BigOne Lab. Don’t forget to subscribe before you continue reading!

China’s Jan & Feb prints were improving across the board

Inflation: In January–February 2026, China’s CPI rose 0.8% year-on-year, and Core CPI hit 1.3% — the strongest reading since January 2023. PPI also showed encouraging signs at the factory gate, with industrial producer prices rising for five consecutive months on a month-on-month basis.

Spring Festival spending held up well, with services standing out. We covered this in detail in a previous post.

The key question: Is this organic or policy-driven?

This is where the honest read gets more nuanced. Much of the consumption uplift to date has been policy-assisted — trade-in subsidies, vouchers, and a record-long nine-day holiday that pulled spending forward.

The 2026 Government Work Report set a GDP target of “4.5% - 5%”—realistic but unexciting. The report prioritizes technology and new productive forces. The report prioritizes technology and new productive forces. Among its measures, China plans to issue RMB 250 billion in ultra-long-term special government bonds to support trade-in subsidies for consumer goods and to establish RMB 100 billion in fiscal-financial coordinated funds to boost domestic demand. To put that in perspective, these measures amount to less than 0.2% of GDP — hardly a massive fiscal stimulus. There is also no large-scale direct transfer to households on the table.

The elephant in the room: Is the strong Jan & Feb spending organic, and will it continue?

To put this into perspective, in today’s Charts of the Week, we return to two key pillars of domestic consumption: the wealth effect (real estate) and income expectations (salary).

Our January–February proprietary data on both fronts points in a positive direction.

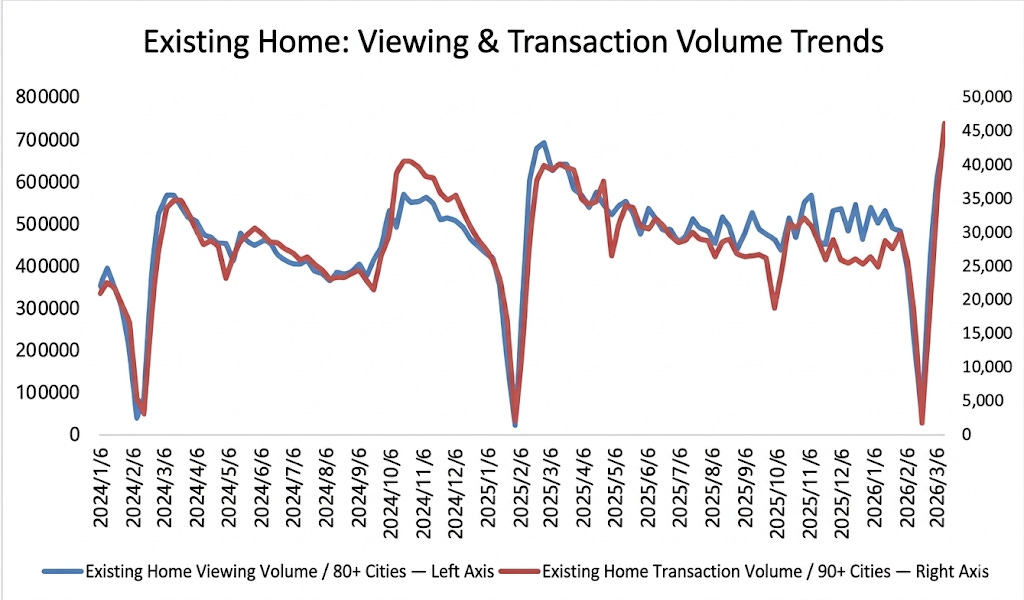

Real estate: Our tracking of China’s online real estate platforms shows the second-hand housing market stabilizing under policy support, with transaction volumes in 90+ cities up 15% YoY. Viewing activity also picked up, with week-on-week viewings across 80+ sample cities rising 15%, reflecting strong buyer interest and a recovering market.

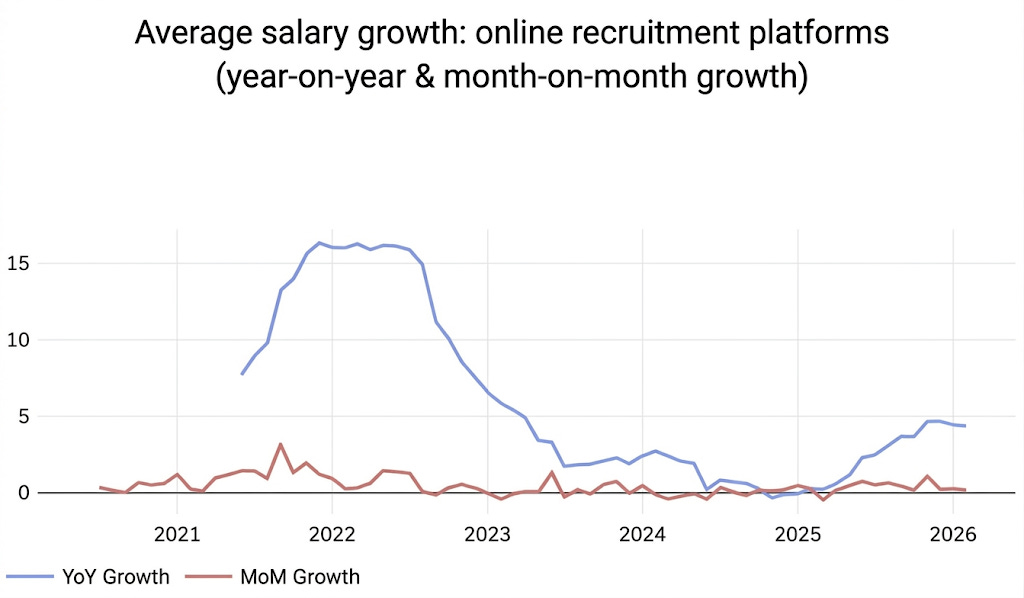

Salary: Average salaries growth across online recruitment platforms are gradually recovering, rising from near-zero in 2024 to around 4–5% in early 2026. This steady wage growth supports household purchasing power, suggesting consumption could continue at a measured pace.

Importantly, the worst of the real estate bubble’s impact on the workforce appears to be behind us, as we covered earlier:

Additionally, in select discretionary categories, we are already seeing what looks like organic spending growth that isn’t purely subsidy-driven. That is the signal worth watching. For example, we wrote about the Sports & Health sector yesterday and will follow up with more examples in future posts.

One additional tailwind: China sits in a different risk bucket than the rest of Asia

The escalation of the Iran conflict has rattled Asian markets, but not all of Asia is equally exposed. China actually sits in a more defensive position, holding large strategic and commercial oil reserves that help cushion short-term disruptions. It has also spent years diversifying its supply toward Russia and Central Asia.

In contrast, Japan relies on the Middle East for roughly 90% of its crude oil imports. South Korea sources about 70% of its crude from the region and routes over 95% of that through the Strait of Hormuz.

Market reactions reflect this. Compared to other Asian markets, China has seen a comparatively modest decline since the conflict began.

A-shares also carry a structural cushion that most markets lack: the “national team” actively intervenes when needed, reducing correlation to external shocks in ways that are hard to replicate elsewhere in the region.

Therefore, I am more constructive on Chinese markets, especially the on-shore market at this particular time.

We will continue tracking real estate and job market data — crucial macro datapoints for our paid subscribers in future posts.

Despite all the positives - the stock mkt is still terrible.