A Note From Baiguan

On April 1, we officially launched Baiguan Pro, our professional-tier subscription designed for investors seeking deeper, more specific coverage of Chinese equities. Baiguan Pro delivers the Baiguan team’s monthly outlook on overall Chinese equity assets, our quarterly focus on themes and sectors, richer company-level analysis, and follow-ups on the ideas and companies previously presented in the newsletter.

If you missed our launch piece, you can read it:

As a reminder, existing paid subscribers can claim a complimentary upgrade to Baiguan Pro (offer ends on June 30, 2026) by simply replying to this email.

In Today’s Data Update

We are updating four sectors that we recently wrote about in the Baiguan newsletter, or mentioned as ideas to watch in Baiguan pro content, with BigOne Lab’s proprietary data as of April 2026:

Sportswear & footwear: Q1 saw a broad-based recovery across athleisure, running, and outdoor, and we will break down the winners and losers. Notably, Lululemon was probed for potential toxic chemicals in its fabric and made Chinese social media headlines, and we will share whether this is an early sign of a sales impact.

Gold jewelry: March marked a sharp reversal for Laopu after a blockbuster Q1, with gold price volatility weighing on price-sensitive buyers. With promotional activity ramping into May, the key question is whether April’s data shows stabilization, further softness, or something else investors should be paying attention to.

Luxury goods: Q1 hinted at a gradual stabilization in Chinese luxury demand, but brand-level dispersion has been the dominant theme. We will share insights about which segments are sustaining momentum into April, and which megabrands are losing ground.

Pop Mart: March already showed cooling in IP heat as the Sanrio collaboration came in below expectations. We will provide updates on April’s new product launches and on secondary market price trends.

At BigOne Lab, we curate data highlights, analyze them, and deliver insights trusted by 100+ top institutional and corporate clients worldwide.

🔒 The following content is available to Baiguan Pro subscribers.

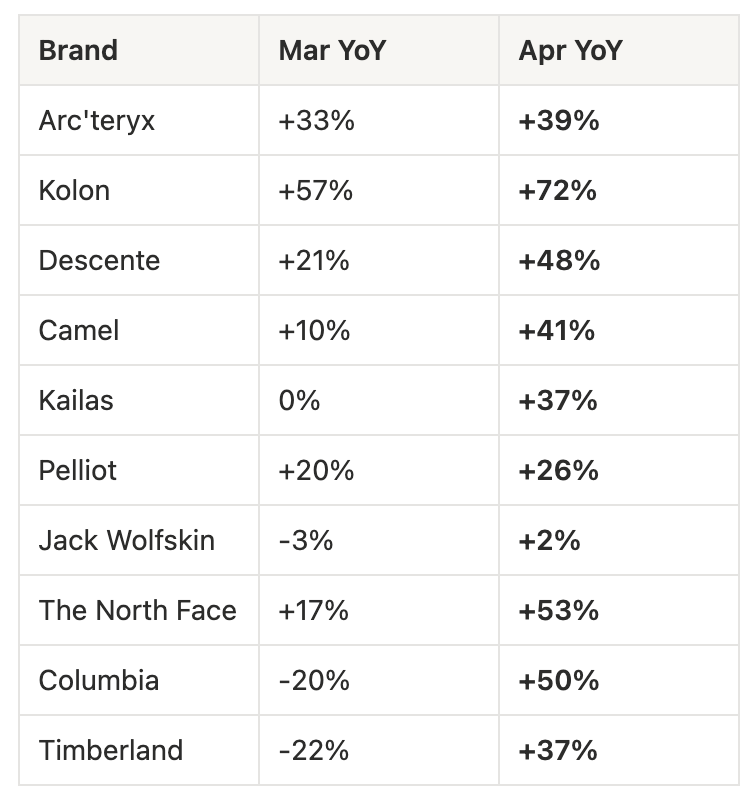

1. Sportswear & footwear

Bottom line: April marks a clear sector-wide reacceleration, with outdoor emerging as the headline growth story alongside continued strength in athleisure and a broad-based recovery across running and integrated brands.

According to our online sales table across major e-commerce platforms:

Outdoor: The standout — acceleration across the board

Outdoor remains the cleanest high-conviction trend in our sportswear data, with virtually every brand we track posting sequential acceleration in April. By category, outdoor apparel and outdoor footwear posted +57% and +47% YoY, respectively (vs. +28% / +41% in March).

Arc’teryx continued its strong run at +39% (vs. +33% in March and +20% in Q1), Kolon delivered +72% (vs. +57%), and Descente accelerated to +48% (vs. +21%). Among more value-tier outdoor players, Camel posted +41% (vs. +10%), Kailas +37% (vs. 0%), and Pelliot +26% (vs. +20%).

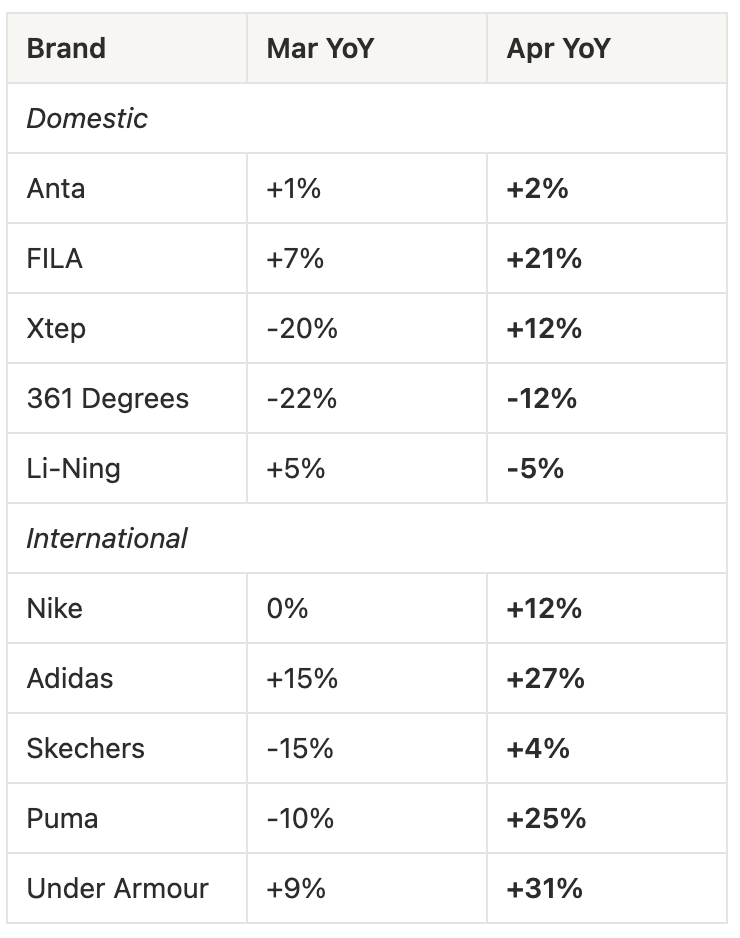

Integrated brands: improvement almost everywhere, with Li-Ning the exception

Among domestic integrated brands, most names improved: Anta +2% (vs. +1% in March), FILA +21% (vs. +7%). Li-Ning was the outlier, slipping to -5% (vs. +5% in March). Across the group, the improvement is driven primarily by volume; ASPs remain in single-digit YoY decline.

International integrated brands saw broad-based acceleration similarly. Nike returned to double-digit growth at +12% (vs. flat in March), helped by a strong reception of the new Pegasus and improved casual footwear.

Athleisure: Lululemon still Strong

Lululemon delivered +39% YoY in April — the late-April social media controversy about the toxic chemicals in the fabric has not yet visibly impacted the data, though we will watch May closely.

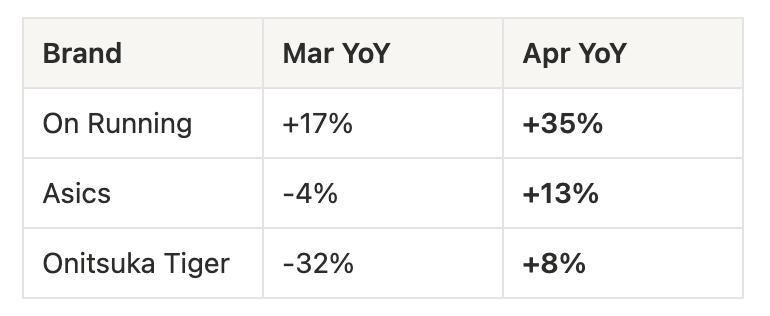

Running shoes: growth returns

Running brands rebounded in April after a softer March. On Running continued to outperform at +35% (vs. +17%).

2. Laopu Gold & gold jewelry

Bottom line: Laopu Gold’s April weakness continued at a pace similar to March, amid broader weakness in gold jewelry as the gold price rally reverses the trend seen in previous months.

Based on our offline payment data, Laopu Gold’s mainland China store sales (excluding SKP locations, on a region-adjusted basis) fell 23% YoY in April, broadly in line with March’s decline. The traffic story is what stands out: customer count was down 21% YoY, and order volume was down 32% YoY, pointing to clearly weaker buyer interest rather than a pure ticket-size issue. The May store-promotion ramp will be the key swing factor to watch.

Our social listening and daily transaction data suggest that gold price volatility has had a meaningful dampening effect on price-sensitive consumers, and that Laopu’s April promotional activity was insufficient to reignite their interest.

From our channel checks, May is expected to bring a broader promotional ramp across regions, with Shanghai and Guangdong rolling out ‘RMB 100 off per RMB 1,000 spent’ campaigns. We will be watching closely for the sequential lift this delivers.

Broader jewelry remains under pressure: Chow Tai Seng is the standout

With Laopu dragging on the category, total offline sales across the four gold jewelry brands we track grew +4% YoY in April (vs. +17% in March). Chow Tai Seng was the clear outperformer at +27% (vs. +24% in March) — the only brand to accelerate.

The high-end branded jewelry sub-segment remains under pressure on an underlying-demand basis. After a strong March (when a low prior-year base flattered comps), Bulgari turned negative to -10% in April (vs. +25% in March) as that base effect rolled off. Tiffany’s weakness extended to -15% (vs. -12% in March).

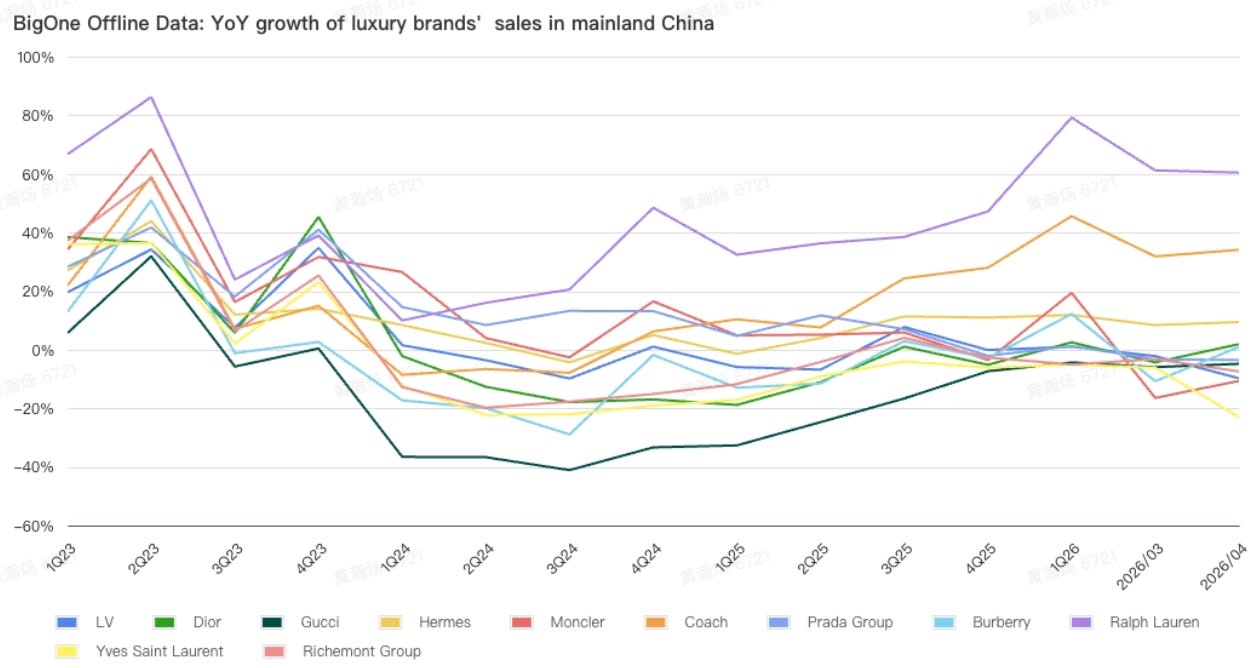

3. Luxury brands

Bottom line: Based on our offline payment data, the overall luxury market grew at a similar pace in April to March, but within-brand dispersion remained sharp. American/accessible luxury continues to be the standout, the high-end held its pace, and a subset of European brands deteriorated further.

Accessible & American luxury: sustained outperformance

Coach delivered another strong month at +34% YoY (vs. +32% in March), and Ralph Lauren maintained its torrid pace at +60% (vs. +61%). Both brands have now sustained high-growth trajectories for several consecutive months, and the consistency of the read across our data suggests these are durable share gains rather than promotional pulls.

Resilient high end: Hermès delivered +9% YoY in April (vs. +8% in March) — the most consistent performer in our luxury data, holding firmly in high-single-digit growth.

Still under pressure and worsening: Louis Vuitton deteriorated to -10% YoY in April (vs. -2% in March) — a notable sequential step down. YSL fell sharply to -23% (vs. -6%), and Richemont Group also slipped further to -7% (vs. -3%).

4. Pop Mart

Bottom line: BigOne Lab estimates April offline sales grew +37% YoY — a meaningful step down from March’s +58% — as a lukewarm new-product slate ran into a tough prior-year base (April 2025 featured Twinkle Twinkle Gen-2 and LABUBU Gen-3). Q2 base pressure persists for the rest of the quarter.

The headline April IP launches — the LABUBU x FIFA collaboration and ‘Flying LABUBU’ series, both plush pendants — underperformed March’s Sanrio collaboration. The mid-month *Twinkle Twinkle ‘Moon Gelato’ ****series *****release saw no notable launch-day spike in our daily sales data.

Secondary market: IP heat cooling

LABUBU Gens 1–4 are at a 30% discount to retail; Twinkle Twinkle Gens 1, 2, and 4 are at a 20% discount. Looking at Twinkle Twinkle’s series: ‘Sweet Dream Forecast’ and ‘Crush on You‘ trade roughly flat to retail. The new ‘Moon Gelato‘ commands a 12% premium — well below the 60% premium ‘Crush on You‘ commanded at its own launch.

Pucky’s ‘Knock Knock‘ series, Hirono’s ‘Road Journal’, and CRYBABY’s ‘Vacation Mode On‘ are the most resilient, trading within 10% of their retail prices.

Plush pendants: a margin offset

April saw 8 figurine blind boxes (+1 YoY), 3 plush blind boxes (+1 YoY), and a record-high 13 plush pendants. With plush pendant ASPs running 50–100% above standard plush products, the mix shift is a likely margin tailwind — an offset worth weighing against the softer revenue print.

Disclaimer: All content in Baiguan Pro is for informational purposes only and reflects directional views based on publicly available information and Baiguan’s proprietary data. Nothing here constitutes investment advice or a recommendation to buy or sell any security. Please conduct your own investment research before making any investment decisions.